Starting May 26, Duc Giang Chemical Group enters a stricter phase of market oversight. HOSE has moved DGC shares from the "controlled" category to "trading restricted" status under Decision No. 445/QD-SGDHCM, citing the company's failure to submit its audited 2025 financial report within the 45-day deadline required by the exchange.CafeF

On the surface, this looks like a compliance paperwork issue. Submit the missing audit report and the restriction lifts. But why would a sector-leading chemical conglomerate let this happen in the first place? The answer has nothing to do with the accounting department. It traces back to a criminal investigation launched in March 2026, which has simultaneously compressed profit margins, forced a mid-year auditor change, and indirectly triggered today's trading restriction. These two problems look separate. They are not.

What the Trading Restriction Actually Changes

HOSE initially announced that DGC would only be tradeable in the afternoon session. After the company filed a clarification, the exchange revised its ruling: DGC can trade throughout the day, but only through periodic lot-matching, not continuous order matching.CafeF

The distinction matters to anyone holding shares. Under continuous matching, buy and sell orders are paired the moment prices align, at any point during the session. Under periodic matching, orders accumulate and are only matched at fixed time intervals, at a single clearing price per batch. The practical consequences for retail investors: thinner liquidity, slower price discovery, and a wider bid-ask spread. Exiting a position quickly during a volatile session becomes considerably harder.

For first-time investors encountering this situation, the key distinction is that trading restricted is not suspension or delisting. Shares remain tradeable. The exit path is clear: once the company submits the completed audit report, HOSE removes the restriction.

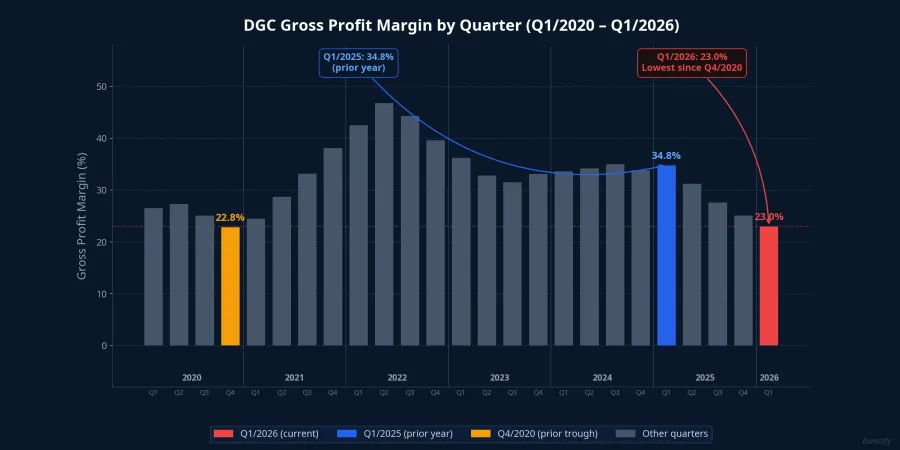

Q1 Earnings: Lowest Gross Margin Since 2020

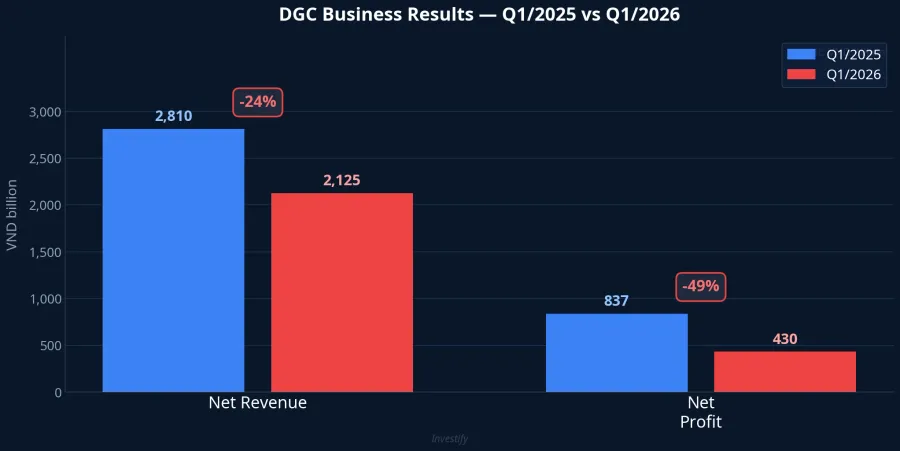

The financial results deserve close attention. In Q1/2026, DGC reported net revenue of VND 2,125 billion, down 24% year-on-year, while net profit dropped to VND 430 billion, a 49% decline.CafeF Gross profit margin contracted from 34.8% in Q1/2025 to 23.0% — the lowest reading since Q4/2020.Nguoi Quan Sat

The question worth asking: why did profit fall nearly in half when revenue only fell by a quarter? Sulfur prices tripling year-on-year is part of the answer. Electricity, coking coal, and ammonia all rose as well. But the heaviest blow came from the company's primary raw material, apatite ore.

The Common Root: the March 2026 Investigation

To understand the margin collapse, you need to look at the competitive advantage DGC is currently losing. Prior to the investigation, the company self-sourced apatite ore from its own quarries — Quarry 25 and Quarry 19B in Lao Cai province — at a significantly lower cost than buying externally. This input cost advantage was DGC's core structural edge, sustaining gross margins in the 30–35% range for years.

In March 2026, the Ministry of Public Security launched criminal proceedings against Duc Giang Chemical and related entities over alleged violations involving environmental regulations, accounting practices, and resource extraction. Former Chairman of the Board of Duc Giang Chemical Group Dao Huu Huyen and several other executives were indicted and detained pending investigation.Tuoi Tre Both quarries were immediately suspended to facilitate the investigation, forcing the group to import ore from Pakistan and Egypt at substantially higher cost.

This is the thread connecting both problems. The investigation forced a mid-year auditor change. The incoming auditor — brought in with no prior familiarity with the accounts — required additional time to conduct the audit from the start. The 2025 financial report missed the statutory deadline by more than 45 days. HOSE placed DGC on the controlled list on May 13, then escalated to restricted trading status on May 26.

The real risk is not the slower order-matching mechanism. That clears when the audit report arrives. The larger risk is the duration of the quarry shutdown. Every quarter the company cannot source ore from its own mines, it operates at a structurally disadvantaged cost base relative to what its historical margins imply.

The Financial Buffer: Over VND 11,200 Billion in Cash

The picture has a counterweight. As of end-March 2026, DGC's total assets remained above VND 18,000 billion, with cash and bank deposits accounting for approximately 62% of that, equivalent to more than VND 11,200 billion.CafeF That figure is approximately 61% of the company's current market capitalisation. This is not the profile of a company facing a liquidity crisis or at risk of insolvency.

However, the operating cash flow figure deserves attention: the company reported a cash deficit of more than VND 1,000 billion in just the first three months of 2026, driven by the cost of importing replacement ore.Doanh Nghiep Hoi Nhap If the quarries remain closed for several more quarters, the cash pile will erode at that pace. Not an immediate threat given the current buffer, but a meaningful signal when read alongside the investigation timeline.

The Path to Lifting the Restriction: Three Signals to Watch

On the remediation side, the board approved UHY Audit and Advisory as the new auditor for the 2025 financial report on May 8 and signed the engagement letter on May 11.CafeF On the same date, Mr. Dao Huu Kha, Chairman of the Board of Duc Giang Chemical Group, was elected to replace his older brother, former Chairman Dao Huu Huyen.CafeF The company says it will publish the full audited report immediately upon UHY's issuance, expected in Q2/2026.

Under exchange rules, a stock exits restricted trading status once the listed company has fully remedied the original cause — here, submitting the audited annual report. The critical milestone is therefore when UHY completes the audit, not where the share price trades this week.

On the price side, DGC closed at VND 48,500 on May 24, down approximately 7.27% from late April. The May 11 session saw over 8.9 million shares change hands alongside a 6.90% single-day decline, as selling pressure concentrated in the days just before the stock entered the controlled category on May 13.

For investors currently holding DGC, three signals are worth monitoring in the coming weeks: when UHY issues the 2025 audit report, which determines when HOSE lifts the trading restriction; whether Quarry 25 and Quarry 19B resume operations, which determines whether gross margins can recover toward historical levels; and what Q2 earnings show, providing evidence of how much accumulated damage has occurred if quarries remain closed through the second quarter.

DGC is a sector leader navigating a significant legal inflection point. The VND 11,200 billion cash cushion rules out an acute financial crisis. But the core cost advantage that built the company's margin profile over years has temporarily disappeared, and the recovery timeline depends on two variables management does not control: the pace of the criminal investigation, and when the quarries are permitted to resume operations.