Before discussing the VND 30,500 billion coming due in Q2's final two months, it's worth establishing the foundation those maturities are landing on. As of end-April, the cumulative value of corporate bonds in payment arrears stood at VND 31,500 billion, equivalent to 2.3% of the total market outstanding.Tin nhanh CK April alone saw four bond series miss principal or interest payments, totaling nearly VND 2,900 billion. This is the backdrop against which Q2's maturity wave arrives — not a clean slate.

What does this mean for bondholders? The real risk isn't the aggregate number. It's the fact that within the same maturity wave, two different issuers can produce two completely opposite outcomes. Most bondholders aren't prepared for that divergence.

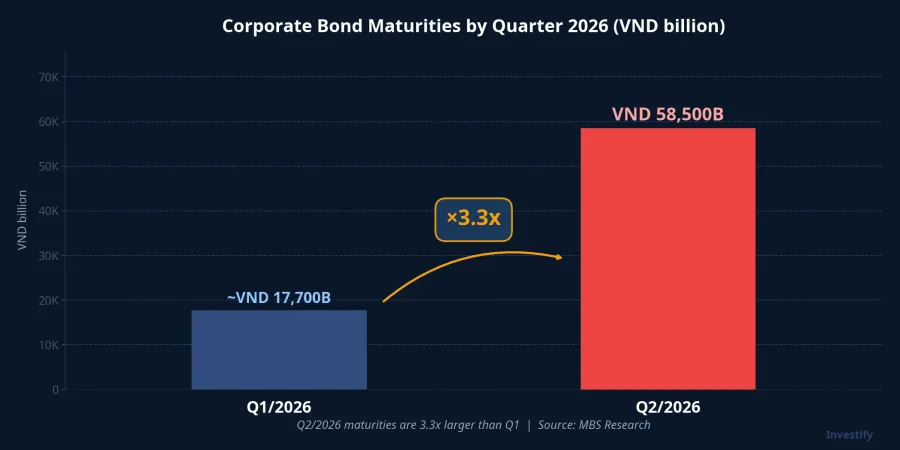

Q2 Maturities Are 3.3x Larger Than Q1: A Legacy of the 2021–2023 Issuance Boom

Per MBS Research's report published May 24, total corporate bond maturities in Q2/2026 amount to approximately VND 58,500 billion — up 140% year-on-year and 3.3 times Q1's volume.VnEconomy This is the largest quarterly maturity so far this year.

The reason isn't difficult to trace. During 2021–2023, Vietnam's corporate bond market ran hot, with many real estate developers issuing large tranches at 3-to-5-year tenors. Those notes are now coming due simultaneously. Q2's maturity pressure isn't a sudden event. It's the predictable endpoint of a debt cycle set in motion years ago.

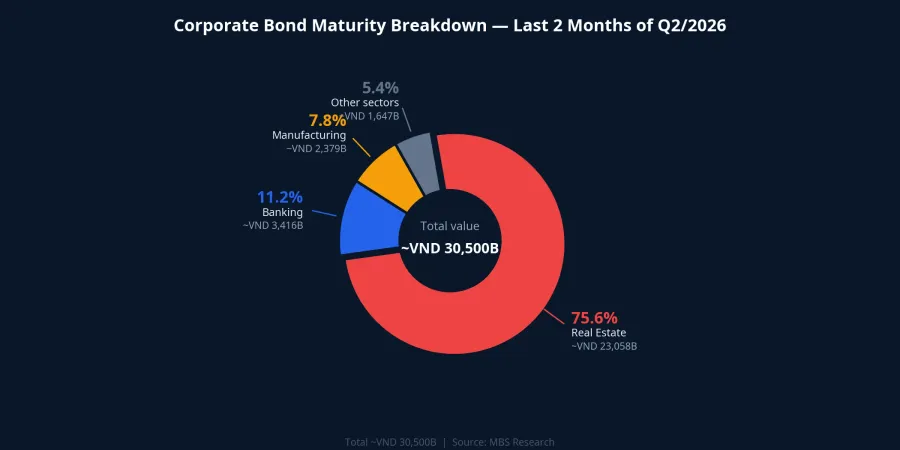

Real Estate Holds 75.6% of the Remaining Two Months

Looking at Q2's final two months alone — May and June — roughly VND 30,500 billion in corporate bonds come due. Of that, 75.6%, or approximately VND 23,000 billion, belongs to real estate issuers.VnEconomy

Real estate isn't just the largest share. It's also the sector with the most complicated track record in prior stress episodes. Many bonds issued during 2021–2023 are tied to projects that remain incomplete, pre-sale, or entangled in legal processes. When the maturity date arrives, repayment capacity depends directly on actual project revenue, not on management's stated intentions.

New Issuance Looks Healthy: But Read the Fine Print

Over the first four months of the year, companies issued VND 93,300 billion in new corporate bonds, up 26.3% year-on-year.Tin nhanh CK Real estate alone accounted for VND 54,400 billion of that — up 278% from the same period last year and representing 58.3% of the total market.VnEconomy On the surface, the market appears active and functional. But this is precisely where the report's headline doesn't tell the full story.

According to MBS Research, most of the new issuance falls short of covering maturing debt, and a significant portion of the fresh capital is being used to restructure existing financial obligations rather than fund new projects.Tin nhanh CK In other words: rising issuance volumes don't equal rising net new capital. Part of that money is circling to service old debt. When the issuance window tightens, the underlying stress becomes visible immediately.

An early signal appeared in May, when several banks hesitated to issue new bonds because of high interest costs.Tin nhanh CK Banks carry the market's highest credit ratings. If even they face cost barriers, the pressure on real estate issuers is considerably larger.

Three Scenarios for the Maturity Wave

The outcome of this episode depends almost entirely on one question: can issuers refinance? From there, the next two months can unfold along one of three paths.

Scenario 1: Smooth absorption. High-quality issuers successfully refinance or repay from project cash flows that have started generating real revenue. For this to materialize, new issuance by real estate companies needs to maintain its current pace, and the 10-year government bond yield — currently at 4.24% per year — must not spike sharply upward.VnEconomy This is the most benign scenario, but it requires multiple favorable conditions to hold simultaneously.

Scenario 2: Differentiation by issuer quality. This is the most probable outcome given current market structure. Issuers that completed restructuring earlier and generate real project revenue will refinance or repay on schedule. Those still working through legacy debt obligations will be forced to seek extensions again or slip into arrears. The systemic effect is that total delinquencies edge above VND 31,500 billion. But in isolated tranches, not a contagious system-wide shock. For bondholders, this scenario demands knowing precisely which category their issuer falls into.

Scenario 3: The refinancing window narrows. Early signals are visible: banks pulling back from new bond issuance in May due to elevated costs. This scenario becomes real if government bond yields continue rising while real estate credit is tightened simultaneously, closing both refinancing channels at once. It's important to be clear: this is a conditional scenario, not a forecast. It only materializes if both triggers occur together.

Two Signals to Watch Through End of Quarter

The most direct leading indicator of which scenario is unfolding is the pace of new real estate bond issuance in May and June. Strong issuance sustaining Q1's momentum points toward Scenario 1 or the constructive half of Scenario 2. Issuance stalling while the 10-year government yield climbs above the 4.24% level tilts probability toward Scenario 3.

The second signal is monthly new delinquencies. April saw four series totaling nearly VND 2,900 billion. If May and June show a sharp uptick, it means Scenario 2 is sliding toward Scenario 3 faster than expected.

Legal Rights for Current Bondholders

Regardless of which scenario plays out, bondholders in real estate notes have specific legal protections under Decree 08/2023 that many holders haven't fully understood.

The most important is the right to refuse an extension. Under Decree 08/2023, issuers may propose extending bond tenors by up to two years, but this requires bondholder consent.Government Portal If a bondholder doesn't agree to the extension, the issuer must still fulfill its full obligations to that holder under the original terms. The right to refuse is real and legally enforceable, not a formality.

Decree 08 also allows issuers to propose settling principal and interest with alternative assets — real estate or equity shares — but again only with bondholder consent.Legal Library Before accepting an asset substitution, holders have the right to demand an independent valuation and can choose to hold out for cash payment if they disagree.

Three concrete steps for bondholders before Q2 closes: determine whether the issuer has completed its prior restructuring and is generating verified project revenue — based on the most recent prospectus and financial statements; read any restructuring proposal carefully before the voting deadline; and participate in votes on schedule while retaining all official notices.

The Divergence Is What Determines Outcomes

The real risk of Q2's maturity wave isn't the VND 58,500 billion headline. It's the differentiation that will occur within that number: issuers that can refinance versus those that can't. Scenario 2 — divergence by issuer quality — remains the most probable path given current market structure. The worse scenario only materializes if rising government yields and tighter real estate credit arrive simultaneously and quickly.

Two indicators will signal which way the market is moving: real estate new issuance in May and June, and the monthly tally of newly delinquent series against April's four. Those two metrics are what determine whether principal comes back on time — and for which holders.