On the morning of May 23, SJC gold bars were selling at VND 162 million per tael, approximately VND 18.2 million above the international gold price converted at Vietcombank's exchange rate.Thanh Niên That 12.7% gap is not a temporary market fluctuation. It is the product of a regulatory framework that has been in place for over a decade, and understanding where it comes from is a natural starting point for anyone comparing long-term savings channels.

This article places four popular channels — SJC gold, the VN-Index, 12-month Big4 bank deposits, and fixed-rate savings products — side by side using five years of data. No single channel can answer all three questions at once: capital safety, returns above inflation, and reasonable liquidity. The goal is to give you a clear picture of each channel's characteristics before you decide.

Why the VND 18.2 Million Gap Is Still There

Since 2012, Decree 24/2012/ND-CP gave the state a monopoly over gold bar production and the authority to allocate import quotas for raw gold. In plain terms: only SJC could make gold bars, and the amount of raw gold allowed into the country was set by regulatory decision rather than market supply and demand. When demand rose faster than supply could respond, domestic prices naturally moved well above global levels.

Decree 232/2025/ND-CP, issued on August 26, 2025 and effective from October 10, 2025, officially ended that monopoly.Vietnam Government Portal Banks with charter capital of at least VND 50,000 billion and enterprises with at least VND 1,000 billion are now eligible to produce gold bars. However, the supply effect has not yet materialized: licensing, importing raw material, and setting up production lines all take time. The VND 18.2 million premium today is the residual echo of the old regime during a transition period.

What does this mean for someone buying gold today? You are paying 12.7% above the international benchmark. If the new supply under Decree 232/2025 enters the market over the next 12 to 24 months, that gap could narrow meaningfully, creating downward pressure for anyone holding gold at current prices.

SJC Gold: Top Nominal Return, Bumpy Ride

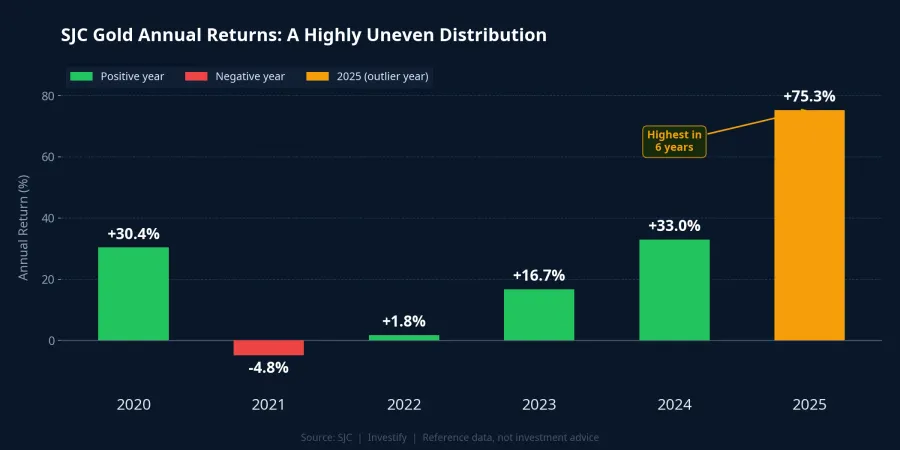

Looking at five-year data from end-May 2021 through May 23, 2026, SJC gold delivered a nominal CAGR of approximately 25.3% per year. That figure stands out in a comparison table, but how it was generated matters just as much as the number itself.

The year 2025 alone contributed a gain of 75.3%, the highest single-year return in the past six years. By contrast, 2021 posted a loss of 4.8% and 2022 gained just 1.8%. A straightforward way to think about it: strip out the 2024–2025 surge, and SJC's CAGR looks much more ordinary. Buyers who entered at end-2024 are sitting on substantial gains. Those who bought at the April 2025 peak are roughly flat.

This is a structural feature of gold as an asset: returns are highly uneven, concentrated in periods of global risk aversion or financial stress. For long-term wealth builders, gold works well as a defensive layer. It is not a vehicle for steady year-by-year growth.

The Other Three Channels by the Numbers

The VN-Index closed at 1,877.13 on May 23, 2026.Vietstock Its five-year CAGR is approximately 7.2% per year, below gold and also below compounded fixed-rate returns for most of the period. However, its three-year CAGR is 20.4% per year, meaning most of the gain was compressed into the 2023–2026 window following a sharp 32.8% correction in 2022. The 7.2% figure also excludes cash dividends, which typically run 2–4% per year among large-cap stocks.

With the VN-Index, the biggest risk is not the average return but the year-to-year volatility. Investors who entered in 2022 and sold in early 2023 took heavy losses; those who held through the bottom and stayed for another three years see very different numbers. This channel suits investors who can tolerate volatility and have a horizon of at least three years.

Big4 12-month deposits are currently offered at 5.9% per year.CafeF This is the most stable return profile of the four channels: no negative years, no market monitoring required. The key caveat is that CPI came in at 4.65% in March 2026, leaving a real return of roughly 1.2 percentage points above inflation. Big4 deposits are a capital-preservation tool, not a wealth-building vehicle.

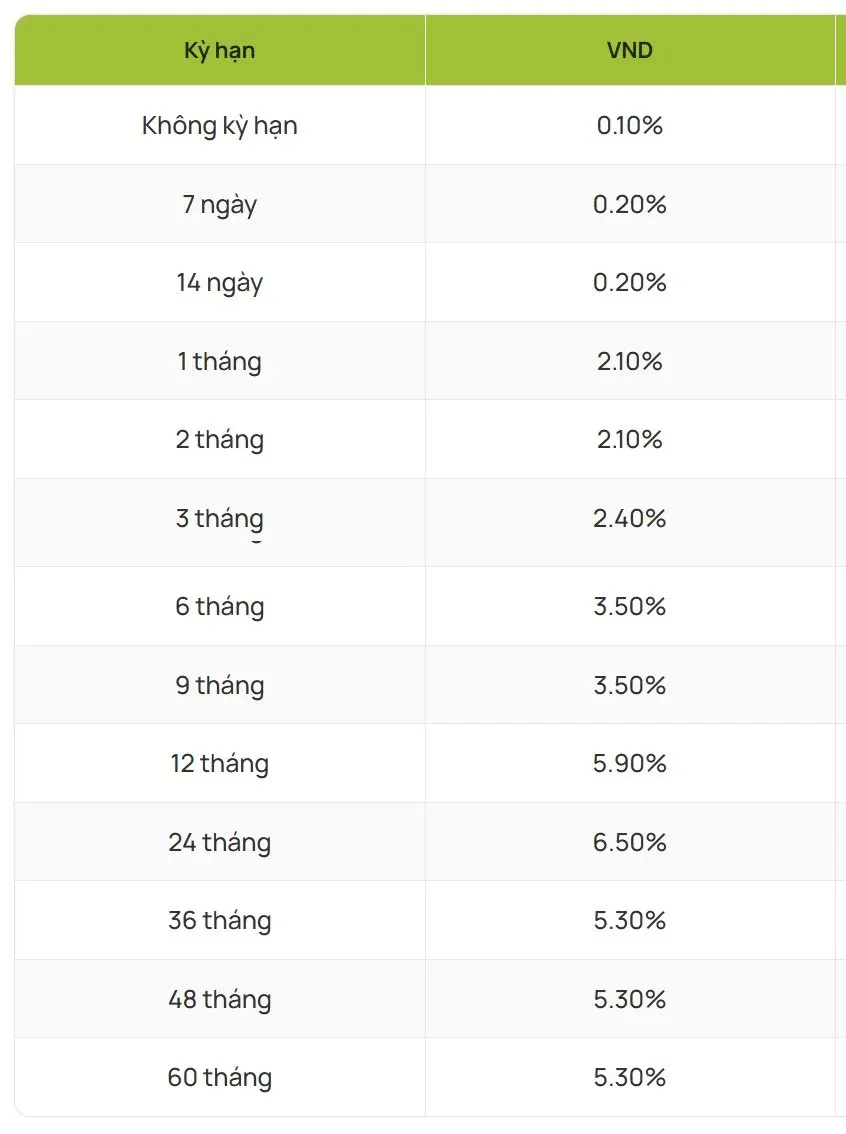

Fixed-rate savings products with tenors of 12–24 months are commonly available in the 7–9% per year range. A sample of current offerings: SHB Online at 7.8%, Hong Leong Bank at 7.6%, and Bac A Bank at 6.9%.Báo Mới Some distribution platforms offer 9–11% for longer tenors, with collateral structures and specific credit ratings attached. This channel outperforms Big4 deposits by roughly 1.5–3 percentage points, with higher issuer credit risk, but that risk is identifiable and bounded, unlike market risk.

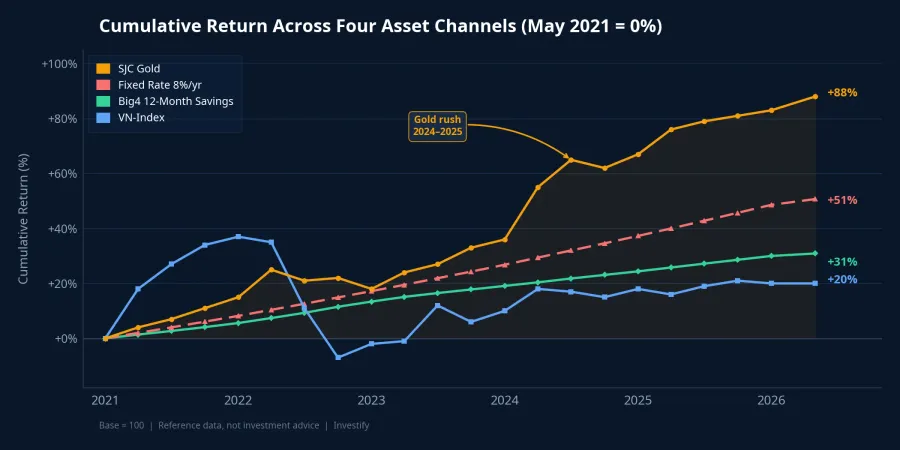

Four Channels Side by Side: The Five-Year Picture

SJC gold leads on five-year nominal CAGR at approximately 25.3% per year. The VN-Index ranks third on five-year CAGR (roughly 7.2%), but beats all four channels if measured from the 2023 trough. Big4 deposits deliver reliable cash flow but thin real returns. Fixed-rate products at 7–9% occupy a middle ground: they outperform deposits, are predictable, and carry issuer risk that can be evaluated upfront.

One observation worth sitting with: if you take the five-year window and remove gold's final 18 months (the 2024–2025 surge), its CAGR drops close to that of fixed-rate products. The advantage gold shows in cumulative terms is largely explained by an extraordinary period. That is not an argument against gold — the period happened, and its magnitude was real — but it is a reason not to extrapolate that CAGR forward mechanically.

The structural premium also matters here. SJC gold currently costs VND 18.2 million per tael more than the global benchmark. If that gap narrows as Decree 232/2025 supply enters the market, buyers at today's prices will absorb a structural loss even if the international gold price holds steady.

Two Signals Worth Watching Over the Next 6–12 Months

With the current return structure, there is no single best channel. A common allocation framework for individual investors with portfolios under VND 5 billion looks roughly like this: 20–30% in physical gold for defense and wealth transfer, 20–30% in deposits and emergency liquidity, 25–35% in fixed-rate products with 12–24 month tenors for predictable cash flow, and 15–25% in equities or fund certificates for active wealth building. This is a reference point, not a fixed prescription. The right weights depend on personal circumstances and how these two signals evolve.

The first signal to watch is the pace of licensing under Decree 232/2025. If eligible banks and enterprises receive approvals quickly and begin bringing new supply to market, the VND 18.2 million premium could compress significantly, shifting the attractiveness of gold relative to other channels. The second signal is the direction of deposit rates. If the Fed holds rates high for longer and the State Bank of Vietnam adjusts its policy rate, the 7–9% band for fixed-rate products could widen further. Each signal will shift the optimal weight across the four channels in a specific direction: not eliminating any of them, but changing their relative appeal.