For most Vietnamese savers, the assumption has long been settled: park money at a state-owned bank, earn 5–6% a year, stay safe. Over the past decade or more, that assumption held. Nominal rates topped CPI, real returns stayed positive, and depositors at the Big 4 banks never had to run the math on whether they were actually gaining purchasing power after inflation.

In May 2026, two data points released in close succession are forcing that assumption to be re-examined, at least for certain deposit terms.

April CPI vs. the Big 4 Rate Sheet

Vietnam's General Statistics Office recorded April 2026 CPI at 5.46% year-on-year, well above the 3.99% average for the first four months of the year.VTV Housing and construction materials rose 6.25%, while food and catering services climbed 4.71%. Together, these two categories — among the most essential spending for Vietnamese households — contributed nearly 3.1 percentage points to headline CPI.Thị trường Tài chính

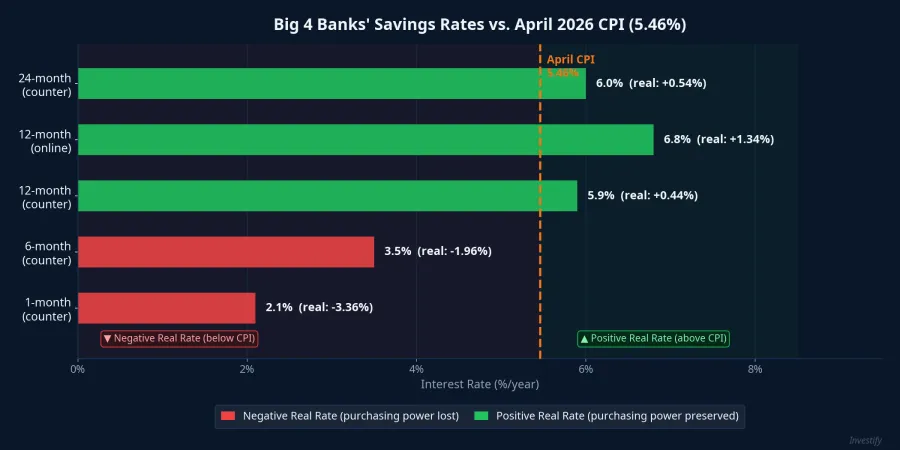

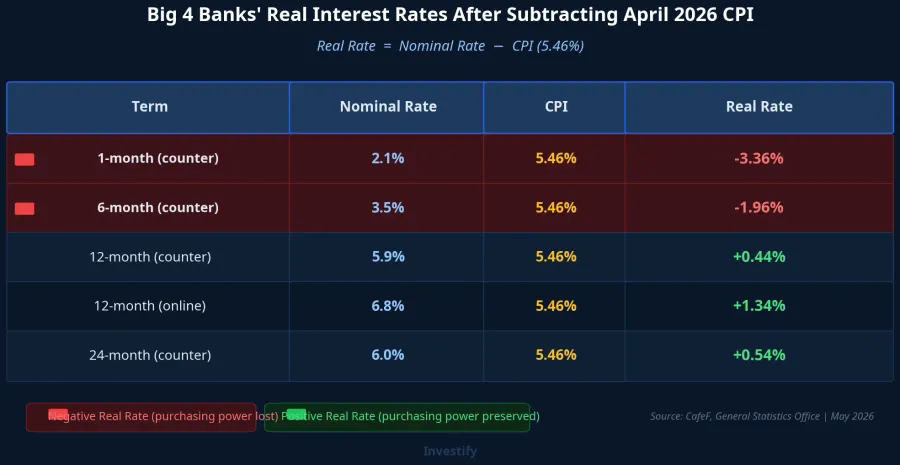

At the same time, the Big 4 banks (Vietcombank, BIDV, VietinBank, Agribank) were offering the following counter rates on new deposits: 1-month at 2.1% per year, 3-month at 2.4%, 6-month at 3.5%, 12-month counter at 5.9%, 12-month online at 6.8%, and 24-month-plus at 6.0%.CafeF

Put those two sets of numbers side by side and the real interest rate, simply nominal rate minus CPI, tells a clear story: the 6-month counter deposit earns a real rate of −1.96 percentage points (3.5% minus 5.46%). The 1-month term is even worse at −3.36 points. Only deposits of 12 months or longer stay in positive territory, with the 12-month counter yielding a slim +0.44 points and the 12-month online channel returning +1.34 points.

Why the 6-Month Term Matters Most

Most individual savers in Vietnam gravitate toward 3- to 6-month deposits for a practical reason: short enough to access funds in an emergency, long enough to earn more than an on-demand account. The 6-month term was once considered the sweet spot between liquidity and yield.

The current picture reverses that logic entirely. The Big 4 6-month counter deposit now carries the most clearly negative real rate of any commonly used term. Consider a straightforward example: VND 100 million placed in a 6-month deposit at 3.5% per year returns roughly VND 1.75 million in interest. Over the same six months, with CPI at 5.46% annualised, the same basket of goods and services costs approximately VND 2.73 million more than before. The net effect is negative: the interest earned does not cover the inflation-driven price increase.

This does not mean bank savings have lost all their appeal. Deposits remain protected by deposit insurance up to VND 125 million per person per bank, carry no capital volatility risk, and remain the right vehicle for emergency funds that cannot be put at any risk. But "safe" in the sense of preserving purchasing power is no longer automatic across all maturities.

The SBV Issues Two Directives in One Week

Against this backdrop of shrinking real returns, the State Bank of Vietnam issued Official Dispatch 4190/NHNN-CSTT on May 21, 2026, instructing provincial SBV branches to inspect commercial banks that had raised deposit rates in violation of the current policy direction.VietnamNet The specific objective is to further reduce the general level of savings rates on terms of 6 months or longer for new transactions, alongside lowering posted rates and lending rates.

This followed Official Dispatch 3972/NHNN-CSTT on May 14, which required SBV provincial branches to work directly with each commercial bank branch in their region to enforce the rate-reduction policy.The Saigon Times The SBV's mechanism here is administrative supervision rather than adjusting rate caps or policy rates. The refinancing rate remains held at 4.5%, establishing a low funding cost floor for the banking system.Báo Chính phủ

The logic is straightforward: to bring lending rates down and support business access to credit, banks' funding costs must first come down. If some banks keep pushing deposit rates higher to compete for liquidity, the system-wide rate level cannot fall. Controlling input funding costs is the prerequisite for controlling output lending rates: a fundamental constraint in monetary policy transmission.

Who Is Still Posting High Rates, and How to Read Them

Compliance across the banking system is uneven. The Big 4 and larger joint-stock banks such as ACB have adjusted to around or below 6% per year on 12-month deposits. Smaller banks, however, are still holding higher: Bac A Bank maintained its 6-month rate at 6.85% and 12-month at 6.9% from May 6; Saigonbank posted 6.4% on 6-month and 6.7% on 12-month deposits from May 8, and raised its 13-month rate to 7.9%, the highest in the standard retail segment.

For the "special offer" rates that circulate widely online, it pays to read the fine print before using them as a reference. VietBank lists a 13-month rate of 10.7% per year with special conditions attached. PVcomBank offers 10% per year on 12–13 month deposits, but requires a minimum balance of VND 2,000 billion. These are products designed for institutional clients or very large depositors, not the rates available to ordinary individual savers. The practical lesson: when checking savings rates online, always confirm the minimum deposit amount and what conditions apply before treating the headline figure as achievable.

The CPI Trajectory and Signals Worth Watching

CPI jumped from a 3.99% average over the first four months of the year to 5.46% in April alone. That is a significant single-month acceleration, and if the trend holds, the implications for each deposit term become increasingly concrete.

Savers currently face two opposing forces: inflation running high while the SBV continues to press for lower rates on 6-month-plus deposits through administrative channels. Nominal rates have little room to rise in this environment, and inflation shows no immediate sign of retreating.

The term decision framework under current conditions is clearer than it has been in some time. The 1- to 3-month range (2.1–2.4% at the Big 4) serves as a liquidity buffer, not a real-return vehicle. The 6-month counter rate (3.5%) is the term with the sharpest negative real return, and faces the most direct downward pressure from the two SBV directives. The 12-month online channel (approximately 6.6–6.8% at the Big 4) is currently the only zone maintaining meaningfully positive real returns, with 6.8% yielding +1.34 points against April CPI.

Two signals are worth tracking in the weeks ahead. First, the May and June CPI readings: if they stay above 5% annually, the 12-month counter rate of 5.9% will begin approaching the zero real-return threshold. Second, whether the smaller banks still posting above-policy rates comply after the two SBV dispatches. The answer will show whether the overall rate level is converging across the banking system or whether a meaningful gap between bank groups persists.