On the morning of May 22 (US time), Kevin Warsh was sworn in as Chair of the Federal Reserve at the White House.Yahoo Finance No Fed Chair has held their ceremony there since former Fed Chair Alan Greenspan in 1987, under then-President Ronald Reagan. Every Chair since has chosen the Fed's own building on Constitution Avenue, a deliberate signal of distance between the central bank and the executive branch. Warsh's return to the 1987 ritual is no footnote: it immediately raises questions about Fed independence at the very moment President Donald Trump is expecting lower interest rates while economic data is telling a different story.

The inflation picture Warsh inherits

The Senate confirmed Warsh on May 13 by a 54-45 vote, the narrowest margin in the modern history of the Fed.CNBC Fed Governor Jerome Powell remained on the Board of Governors after stepping down as Chair. Observers read this as a structural buffer protecting the central bank's independence from political pressure. But whoever occupies which seat, economic data does not consult politics.

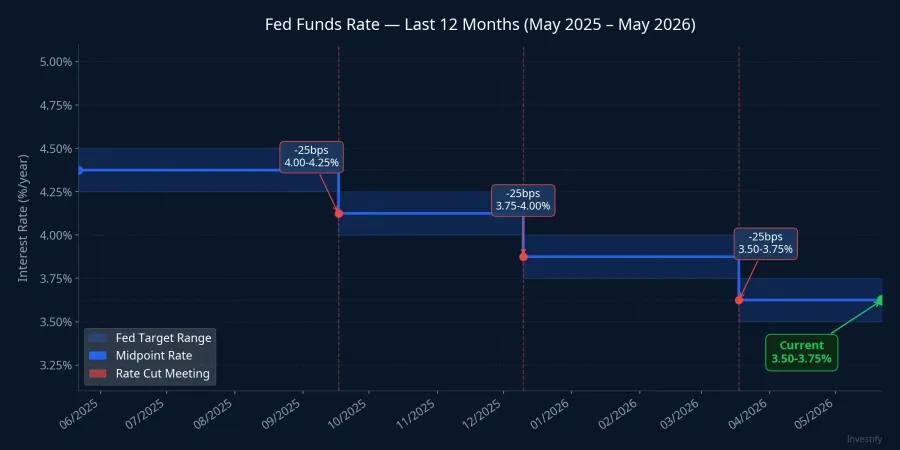

US CPI for April rose 3.8% year-over-year, the highest since May 2023, driven primarily by a 17.9% surge in energy prices tied to the ongoing Iran conflict.CNBC Brent crude climbed to a peak of $112.00 per barrel on May 18 before retreating to $102.98 on May 22. The April FOMC meeting minutes, released on the evening of May 20, showed that a majority of members considered a rate hike a scenario worth contemplating if inflation remains persistent.CNBC The Fed funds rate currently sits in the 3.50–3.75% range following three consecutive cuts since September 2025.

This is the inheritance Warsh receives from day one: Trump appointed him with an explicit expectation of lower rates, but inflation data and market sentiment are pushing in the opposite direction.

Three scenarios, three different outcomes

The big picture points to three plausible paths ahead, each with distinct triggers.

Rate hike scenario. Trigger: Iran tensions extend through Q3, Brent revisits $110/barrel, and CPI for May–June surpasses 4.5% with pressure spreading beyond energy. Paul Tudor Jones, Founder and Chief Investment Officer of Tudor Investment Corporation, said on CNBC on May 7 that there is "no chance" Warsh can cut rates in this environment, and that the Fed may even need to consider a hike.CNBC If this scenario plays out, the USD stays strong, the USD/VND rate — currently at VND 26,371 — faces additional upward pressure, and international capital flows tend to pull back from emerging markets.

Hold steady, wait for data. Trigger: US–Iran negotiations show progress over the summer, Brent falls and sustains below $90/barrel for two consecutive months, and Q3 CPI cools toward 3%. This scenario aligns with Warsh's policy record from 2006–2011 when he served as a Fed Governor: cautious about balance sheet expansion, prioritizing inflation-fighting credibility over short-term stimulus. For Vietnam, this means a range-bound USD, a stable exchange rate, and partial recovery of foreign capital flows that would not yet be strong enough to power a sustained rally.

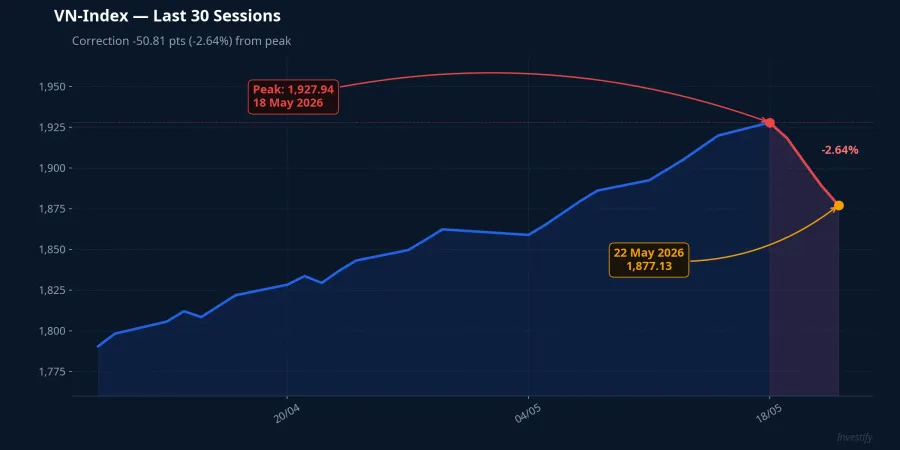

Rate cut scenario, in line with Trump's expectations. This is the scenario requiring two simultaneous conditions: a clear US economic slowdown (payroll growth below 100,000 for two consecutive months, manufacturing PMI below 47) combined with a de-escalation of Iran tensions and a rapid drop in oil prices. For Vietnam, this is the most favorable outcome: a weaker USD, stronger capital inflows, and room for the VN-Index to recover from its current level near 1,877.

What the White House ceremony says about independence

It is no accident that the swearing-in venue drew market attention. In 1987, Reagan hosted Greenspan's ceremony to signal political support for the successor to Paul Volcker. Since then, every Fed Chair has held their swearing-in at the Fed's own building to assert distance from the executive branch. Warsh's return to the White House puts his political relationship with Trump on public display from day one.

His actions over the coming weeks will be the real test. During his tenure as a Fed Governor from 2006 to 2011, Warsh repeatedly opposed former Fed Chair Ben Bernanke's quantitative easing programs and wrote policy papers emphasizing balance sheet discipline. If he maintains that stance, he will find it difficult to cut rates with CPI at 3.8%, regardless of what Trump wants. If he shifts to accommodate political expectations, markets will reprice the Fed's credibility. In that scenario, the USD could weaken not because rates are falling but because institutional credibility is eroding. That is a far more complex dynamic than a standard easing cycle.

Three signals to watch

Foreign investors net-sold more than VND 3,200 billion on May 22, concentrated in bank stocks.Nguoi Dua Tin The VN-Index has shed 50.81 points (-2.63%) since its May 18 peak of 1,927.94. Both moves coincided with the week of heavy Brent volatility and the release of the FOMC minutes. International capital is repricing Fed policy risk ahead of fresh data.

Three concrete signals can help identify which scenario is materializing:

US–Iran negotiations and Brent's reaction. This is the single most decisive variable. Brent sustaining below $95/barrel for two consecutive months would ease CPI pressure and raise the probability of the hold scenario. Conversely, if Brent revisits $110, the rate hike scenario becomes the dominant path.

US CPI for May, due in mid-June. Core CPI (excluding energy and food) matters more than the headline figure: it shows whether price pressures have spread beyond energy. Core CPI for May holding below 3% keeps the hold scenario viable. Core CPI above 3.5% would be a signal that the Fed needs a stronger response.

Warsh's first Congressional testimony. The language he uses on Fed independence and inflation expectations will set the frame for market reaction. References to "balance sheet discipline" in the vocabulary familiar from his 2006–2011 tenure would signal he is not prepared to cut under pressure. Softer language would invite questions about credibility.

Overall assessment

The big picture currently leans toward the hold scenario through Q3 2026. CPI at 3.8% and the April FOMC minutes leaving the door open to a rate hike leave no room for Warsh to cut immediately, regardless of Trump's wishes. The rate hike scenario needs additional adverse data from Iran and from May–June CPI before it becomes the dominant path. The rate cut scenario requires two favorable conditions simultaneously, and neither is presently clear.

The larger risk to monitor is a USD weakening driven by eroding Fed credibility rather than by rate cuts. This is significantly harder to price in advance than a standard easing cycle, because it occurs when nominal rates are still elevated but markets lose confidence in policy consistency. In such a cycle, capital flows can shift abruptly in ways that historical models do not reliably predict.

The decisive signals will come from Warsh's words before Congress and from the May CPI print, not from today's swearing-in ceremony.