On May 20, 2026, SpaceX filed its S-1 registration statement with the U.S. Securities and Exchange Commission (SEC), kicking off its planned Nasdaq listing under the ticker SPCX with trading expected to begin June 12.CNBC This is the first time SpaceX's internal financials have ever been disclosed publicly, and the numbers describe a company that looks quite different from the "rocket company" image most people carry.

The top-line figures appear contradictory: 2025 revenue reached $18.67 billion, yet SpaceX posted a net loss of $4.94 billion for the year.The VC Corner In Q1 2026 alone, $4.69 billion in revenue accompanied a $4.28 billion loss. Meanwhile, Starlink by itself generated over $1.2 billion in profit over the same period.implicator.ai The natural question is: where is the money going?

Starlink: The Real Profit Engine

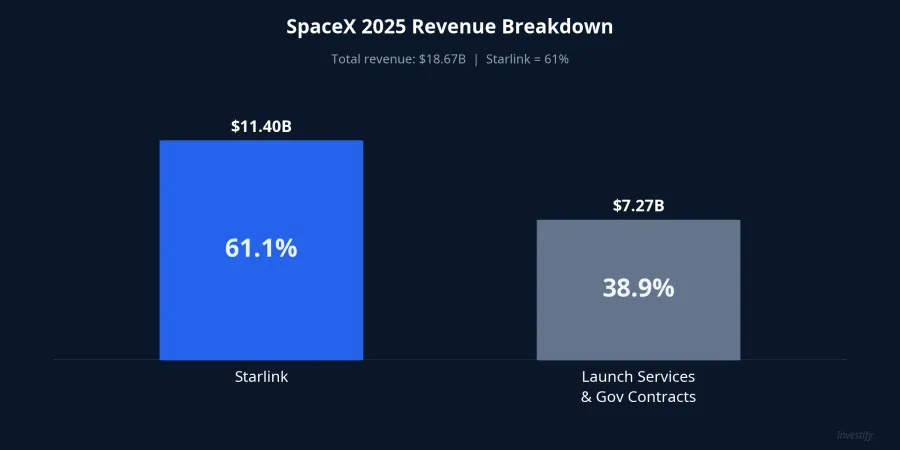

Breaking down the revenue structure brings the picture into focus. Of SpaceX's $18.67 billion in 2025 revenue, Starlink contributed $11.4 billion, representing approximately 61% of the total.implicator.ai The remaining $7.27 billion came from launch services and U.S. government contracts, including ISS cargo missions and defense work.

What stands out in the Starlink data is an adjusted EBITDA margin of 63%, generating $7.17 billion in operating cash flow from that segment alone. Subscriber count has crossed 10.3 million, more than doubling from 5 million a year earlier. This is the classic scale inflection point for infrastructure businesses: the cost of launching and deploying satellites has already been spread across prior periods, and each new subscriber adds revenue with minimal incremental cost.

Put plainly: the SpaceX in the S-1 is not a rocket company. It is a global satellite internet company that is using the cash flows from that business to fund a large-scale AI infrastructure race.

AI Division: Where Capital Flows

After SpaceX acquired xAI in February 2026, the Colossus computing cluster in Tennessee and Mississippi was folded into the consolidated balance sheet. The AI division has since become the largest consumer of capital across the entire company.

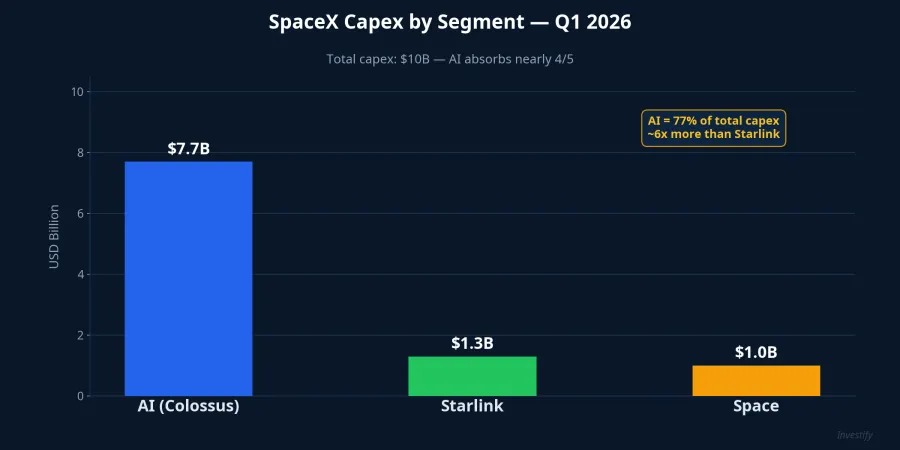

In 2025, the AI segment posted an operating loss of $6.4 billion and consumed $12.7 billion in capital expenditure.The VC Corner Q1 2026 saw the pace accelerate further: AI infrastructure capex for the quarter alone was $7.7 billion, compared with $1.3 billion for Starlink and $1.0 billion for the space segment. Roughly 77 cents of every dollar SpaceX deployed in capex during the quarter went to AI.

Colossus 1 now operates over 220,000 NVIDIA GPUs, including H100, H200, and GB200 units, with combined computing capacity exceeding 1 gigawatt.IBTimes That scale puts SpaceX in the same tier as the world's largest AI data center operators.

The S-1 also provides a partial answer to how returns are expected to flow back: Anthropic signed a contract to pay SpaceX $1.25 billion per month for access to Colossus capacity, running from May 2026 through May 2029, for a total contract value of approximately $15 billion.IBTimes This revenue had not fully materialized in 2025 figures, but it explains why SpaceX can sustain this burn rate: Colossus is not serving xAI's Grok exclusively: it is a compute infrastructure landlord, with Anthropic as a paying tenant.

One causal point worth making explicit: the $4.94 billion consolidated net loss in 2025 is not a sign that Starlink is underperforming or that the launch business is struggling. Both segments are operating soundly. The loss is attributable almost entirely to Starship R&D costs and, more significantly, AI infrastructure capex. This is a deliberate strategic choice.

Dual-Class Share Structure: Musk Controls 85.1%

The governance structure is the least-discussed section of the S-1, but arguably the most important for investors. SpaceX will issue two classes of stock: Class A shares carry one vote per share, while Class B carries ten votes per share.MSN Elon Musk, CEO and founder of SpaceX, holds the majority of Class B shares, giving him 85.1% of total voting power.

The practical implications for anyone buying SPCX on Nasdaq are straightforward: every major strategic decision rests with one individual. Capital allocation among Starlink, Starship, and Colossus; AI business direction; structural changes to the company. All of these decisions sit exclusively with Musk. Class A shareholders have economic rights proportional to their ownership stake, but no meaningful governance leverage to influence those decisions. The structure is similar to Meta or Alphabet at the time of their IPOs, though the 85.1% concentration is substantially higher than either of those cases.

94x P/S: Reading the Valuation Correctly

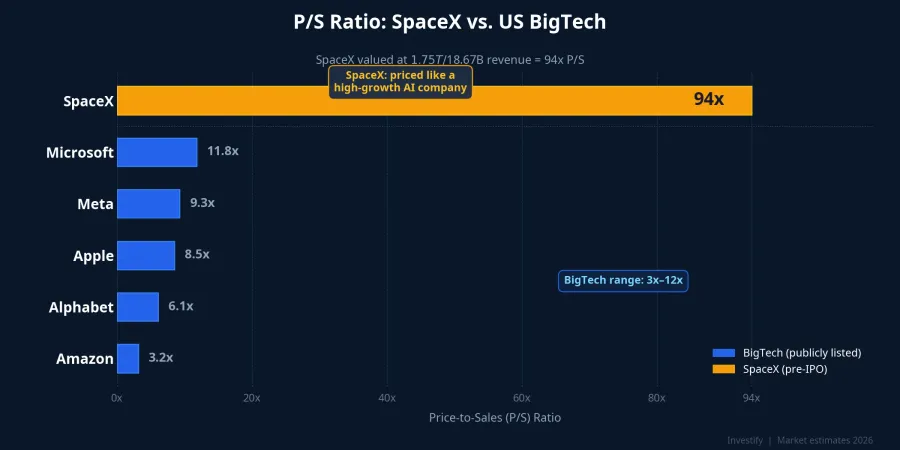

At a target valuation of approximately $1.75 trillion against $18.67 billion in 2025 revenue, SpaceX's implied price-to-sales ratio sits at roughly 94x.SatNews For context, the U.S. BigTech group — Apple, Microsoft, Alphabet, Meta, Amazon — typically trades in the 3x to 12x range.

A more useful framing is to decompose the valuation into three parts. The Starlink segment, with its 63% EBITDA margin and steady cash flows, could reasonably carry a mid-double-digit revenue multiple by internet infrastructure standards, implying several hundred billion dollars on its own. The launch and government contracts business is stable but lower-margin, warranting a more conservative multiple. The remainder of the $1.75 trillion sits with the AI division: currently loss-making, valued on long-range expectations. Buying SPCX at this price means paying primarily for the probability that the AI division becomes a cloud computing platform on par with AWS or Azure within five to ten years.

For Vietnamese Investors

According to international financial news coverage, SpaceX is targeting a roadshow starting June 4 with official pricing on June 11 and trading beginning June 12.HeyGoTrade Vietnamese retail investors can access SPCX through international brokerage accounts that support U.S. market trading, subject to standard T+2 settlement on U.S. market hours.

Dividends and capital gains from foreign securities are subject to personal income tax obligations in Vietnam and must comply with regulations governing repatriation of profits. These are practical details that should be confirmed with your custodian and a tax advisor before placing any orders.

Read the S-1 Before You Buy

The S-1 has put enough data in the public domain for investors to form their own views. The bull case rests on three pillars: Starlink holds its 63% margin as Amazon Kuiper and new satellite competitors enter the market, Colossus evolves into a profitable cloud computing platform over five to ten years, and the $15 billion Anthropic contract is the opening chapter of a longer infrastructure-leasing revenue stream. The bear case depends on the opposite: Starlink margins erode under competitive pressure, the AI division continues burning capital without a clear path to profitability, and the 85.1% voting structure leaves minority shareholders with no mechanism to influence the outcome.

The deciding variables to monitor: Starlink subscriber growth in Q2 2026, additional compute-leasing contracts signed after Anthropic, and the final IPO pricing relative to the $1.75 trillion target. These three data points will answer most of what needs to be known about the probability of each scenario.