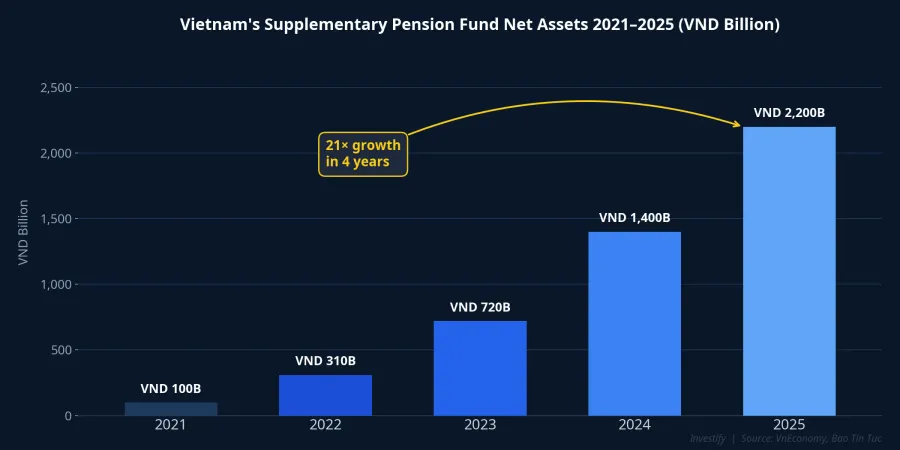

When people hear "tax benefit," they generally expect a meaningful number. But after years of piloting, Vietnam's voluntary supplementary pension fund system counts just under 28,600 participants and VND 2,200 billion in net assets — a 21-fold increase since 2021.VnEconomy Against total household bank deposits in the system, that is still a tiny fraction. The natural question: why does a product with explicit tax incentives attract so few people?

The answer isn't that the product is poorly designed. It comes down to one specific number: VND 1 million per month.

What Is a Supplementary Pension Fund, and How Does It Differ from an Open-End Fund?

Think of it this way: a voluntary supplementary pension fund is a long-term savings account for retirement, sitting alongside the mandatory social insurance system. Employees and employers contribute regularly. A fund management company invests the money to generate returns over time. At retirement age, participants receive monthly payouts or a lump sum.

Two core differences from a regular open-end fund certificate. First, contributions are deductible from personal income tax (PIT), up to a maximum of VND 1 million per person per month.LuatVietnam Open-end fund certificates carry no such benefit. Second, the money cannot be freely withdrawn. You must wait until retirement age, or fall into a narrow set of special circumstances defined by law.

Simply put: you trade liquidity for a tax benefit. This is exactly the logic behind every pension system in the world, and Vietnam's model follows the same architecture at a smaller scale. The practical question is whether the tax benefit is large enough to compensate for losing access to your money.

Decree 85: A Broader Portfolio, but Not a Fix for the Core Bottleneck

Decree 85/2026/NĐ-CP took effect on May 10, 2026, replacing Decree 88/2016.ThuvienPhapluat The most significant change: supplementary pension funds may now invest in listed securities,NhanDan subject to risk limits and requirements to maintain a high allocation in safe channels like government bonds and bank deposits. Previously, portfolios were more restricted, which suited capital preservation but capped long-term return expectations.

The new decree also requires full disclosure before employees sign up, standardizes agreements between employees and employers, and raises oversight standards for fund management companies. Four licensed operators currently run seven active funds: Dragon Capital Vietnam (DCVFM), SSIAM, MB Capital, and Vietcombank Fund Management (VCBF).VnEconomy

These are all worthwhile improvements. A diversified portfolio means higher long-term return potential. Greater transparency lowers the risk of participating. Yet both changes are supply-side fixes. The reason employees don't join in larger numbers is a demand-side problem, and Decree 85 barely touches it.

The Real Bottleneck: What Does VND 1M per Month Actually Buy You?

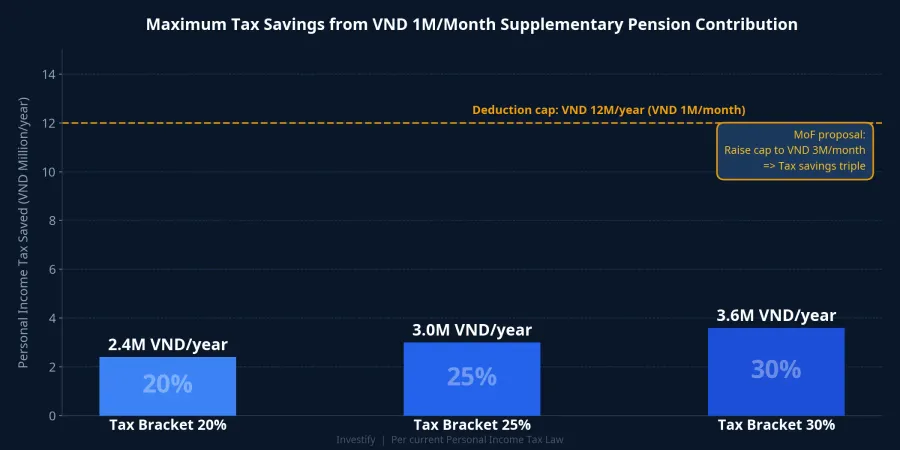

This is the most important part. Under current law, total contributions to supplementary pension funds — including both the employer's contribution on behalf of employees and the employee's own contribution — may be deducted from taxable PIT income, up to a combined cap of VND 1 million per month, aggregated across all funds.LuatVietnam

Do the math: VND 12 million per year is the maximum deduction. At the 20% PIT bracket (taxable income roughly VND 18–32 million per month), the maximum tax saving is VND 2.4 million per year. At the 25% bracket, approximately VND 3 million. At 30%, approximately VND 3.6 million. That is the total direct financial reward an employee receives for agreeing to lock their money in an account until retirement.

Compared with an open-end fund certificate — no tax benefit, but redeemable within three to five business days — a saving of VND 2–3.6 million per year is not enough to compensate for giving up liquidity entirely. This is especially true for workers in the 25–40 age range, a period when the need for flexible capital is high: buying a home, starting a family, changing careers, or launching a new venture.

The VND 1 million ceiling has barely changed in over 12 years, while nominal incomes for urban workers have increased significantly since the threshold was introduced into the PIT Law around 2013–2014. The effective value of the benefit relative to income has steadily eroded over time.

The Ministry of Finance has proposed raising the ceiling to VND 3 million per month, covering both supplementary pension funds and voluntary pension insurance products.DNSE This proposal has not yet been issued into law.

Two Structural Barriers: Distribution Channels and Withdrawal Conditions

Beyond the low tax ceiling, two other structural factors explain why the 28,600-person figure has remained modest.

Distribution currently flows primarily through employers. Companies sign contracts with fund management firms, then arrange participation for their staff. Freelancers, self-employed workers, and individual business owners — who make up a significant share of Vietnam's workforce — have virtually no direct access. Small and medium enterprises also tend to avoid the additional administrative burden.

Withdrawal conditions are strict. Outside of reaching retirement age, early withdrawal is permitted only in narrow circumstances: death, critical illness, labor capacity loss of 81% or more,BaoChinhPhu or foreign workers whose work permits have expired. This is a hard lock, fundamentally different from a term bank deposit where breaking the term only forfeits interest, or an open-end fund where redemption takes a few business days.

These two barriers are structural features of pension products, not design flaws that Decree 85 could easily fix. Loosening withdrawal conditions would undermine the tax incentive logic. Opening distribution beyond the employment relationship requires deeper product redesign, not just a regulatory update.

Where the Supplementary Pension Fund Fits in a Long-Term Portfolio

What does this mean for your savings plan? For salaried workers aged 25–40 building a long-term portfolio, the supplementary pension fund is best treated as a supplementary layer, not the primary one.

Placing it alongside other familiar channels: Big 4 bank deposits at 12-month terms currently offer roughly 5–5.5% per year with high liquidity; open-end fund certificates carry higher expected long-term returns but fluctuate with markets; investment-linked insurance has a similar tax benefit but front-loaded fees in the early years. The supplementary pension fund offers long-term return potential close to an open-end fund, plus a tax benefit, but trades off the lowest liquidity of any of these channels.

The optimal contribution level is to use exactly the tax deduction ceiling: VND 1 million per month, or VND 12 million per year. Anything above that loses the tax deduction but retains the lock-up. There is no rational case for choosing that path when you can instead add to a standard open-end fund with clearly superior liquidity.

If your current capital still needs to stay liquid for near-term goals — buying a home, family expenses, maintaining an emergency buffer — that portion belongs in high-liquidity channels first. The supplementary pension fund is a long-term strategic component, best suited for when you already have a solid liquid foundation.

Key Signals to Watch

The picture changes significantly if the Ministry of Finance issues the proposed ceiling increase to VND 3 million per month. At that point, annual tax savings at the 20% bracket would reach approximately VND 7.2 million. The liquidity-versus-tax-benefit trade-off calculation would need to be redone from scratch, and the optimal allocation would look different.

Under the current legal framework, the clearest conclusion is: contribute to the supplementary pension fund up to the VND 1 million per month tax ceiling to capture the available benefit; allocate savings beyond that to channels with liquidity that matches your financial plan at each life stage. The two signals worth monitoring in the coming months are the concrete progress of the Ministry of Finance's ceiling proposal, and whether any future expansion of access to freelance and self-employed workers is on the agenda.