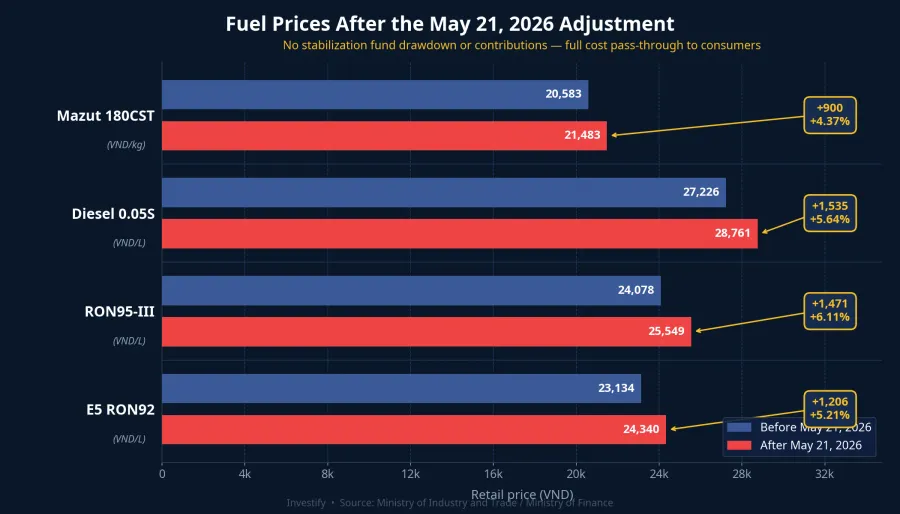

Effective from 3 PM on May 21, 2026, Vietnam's retail fuel prices moved to a new level with broad increases across all products: E5 RON92 rose to VND 24,340/liter (up VND 1,206), RON95-III to VND 25,549/liter (up VND 1,471), diesel 0.05S to VND 28,761/liter (up VND 1,535), and mazut 180CST to VND 21,483/kg (up VND 898).Tuoi TreNLD This was the tenth price adjustment of the year 2026.

What matters more than the size of the increase is the decision that came with it: for this cycle, the joint Ministry of Industry and Trade / Ministry of Finance committee neither contributed to nor drew down the petroleum price stabilization fund for any product.Tuoi Tre Previously, when the fund absorbed part of an increase, fuel-intensive businesses had a buffer window to adjust their cost structures. That buffer is now gone: 100% of the world-price increase passes straight through to domestic retail, with no cushion in between.

The Stabilization Fund Has Run Low

The reason the government could not intervene through the old mechanism is that the fund itself has fallen into deficit at several distributors. Per data through May 14, PV Oil alone was more than VND 1,611 billion in the red on its share of the fund; Petro Binh Minh was down more than VND 138 billion; Truong An Phat was short nearly VND 15 billion.24h The Ministry of Finance had not published a consolidated balance as of May 21, but the decision to pass the full cost shock to consumers speaks to how much room for maneuver remained.

The most important implication for equity investors: fuel-intensive businesses no longer have a time buffer to pass on rising input costs. The increase from this cycle feeds directly and immediately into Q2 cost structures and beyond, depending on how much of each company's revenue is locked in fixed contracts.

Operating Margin and Fuel Share: The Two Axes That Define Risk

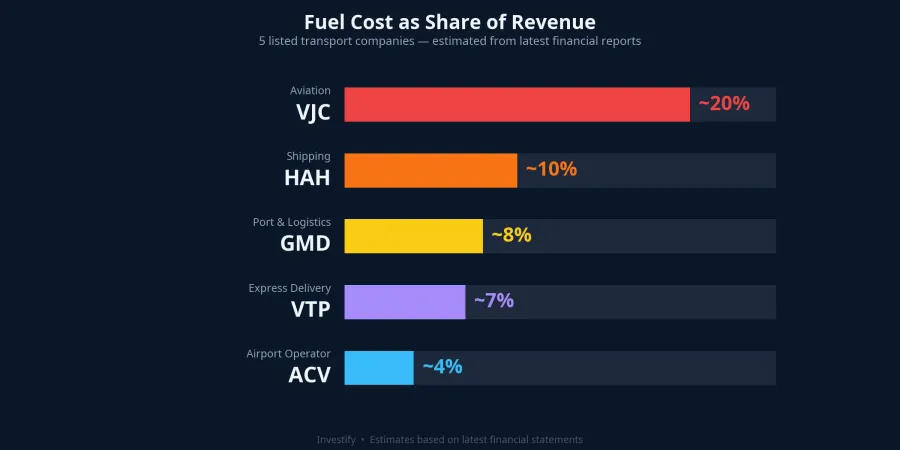

To gauge how much each transport stock is exposed, two metrics need to be read together: fuel cost as a share of revenues (indicating fuel dependency) and operating margin (indicating the cushion available to absorb cost shocks). Companies with high fuel dependency and thin margins face the largest margin compression risk when the stabilization fund is no longer providing relief.

Looking at estimates from the most recent financial statements, the listed transport sector diverges clearly. VJC sits at the unfavorable end of both axes: fuel costs account for approximately 20% of its cost base, roughly double that of the shipping companies and five times that of ACV, while operating margin over the past four quarters has been under 6%, the thinnest in the group. At the opposite end, ACV carries fuel exposure of only around 4% with an operating margin of approximately 60%, making it almost insensitive to fuel price moves in the near term.

VJC: Highest Fuel Share, Thinnest Margin

VJC closed May 21 at VND 173,500, up a modest 1.70% on the day, before the new prices were announced at 3 PM. Friday, May 22, is therefore the first session in which the market can reprice VJC against the new fuel cost environment.

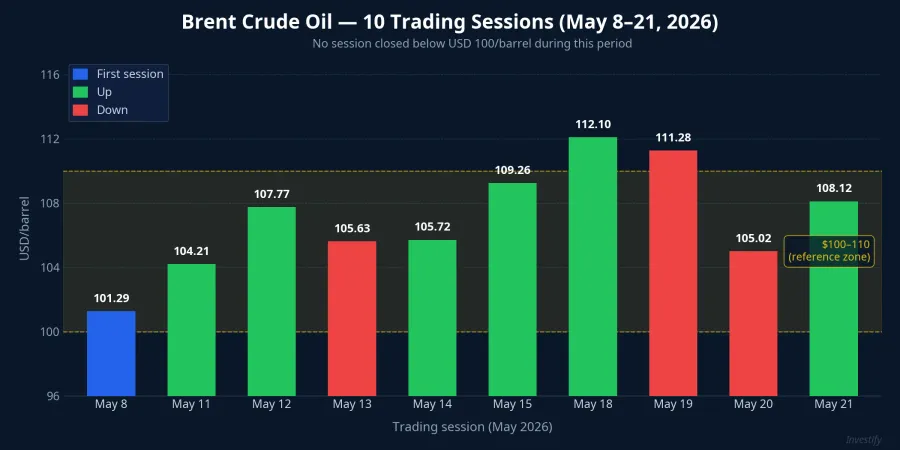

With fuel representing approximately 20% of cost structure, every percentage-point increase in fuel expense flows directly into margin with high intensity. Based on sensitivity estimates, a 10% rise in overall fuel costs could compress VJC's operating margin by roughly 2 percentage points. With diesel up 5.64% in a single adjustment cycle and international Jet A1 tracking closely against Brent (closing at USD 108.12 per barrel on May 21), the pressure is likely to seep through over multiple reporting quarters rather than clearing in one.

One additional point: VJC cannot adjust its fuel surcharge immediately. The approval process for aviation fuel surcharges requires regulatory review and advance notice. The gap between rising costs and an adjusted revenue line will compress margins in the near term, even if the market understands that pass-through will follow eventually.

VTP: Operating Margin Close to Breakeven

Viettel Post (VTP) is the second name to watch from a margin compression standpoint. An operating margin of just over 1% and estimated fuel exposure of around 7% of costs place VTP in a particularly exposed position: a 5.64% diesel increase in a single cycle could push margins toward breakeven if the company cannot adjust delivery fees quickly enough to match.

VTP closed May 21 at VND 68,900, down 2.27%, after two consecutive sessions of declines following sharp gains of 4.76% and 5.13% on May 18–19. The market appeared to have begun revising expectations even before the official price announcement. Friday's session will reveal how the market prices this cost risk in an environment where the stabilization fund no longer provides any cushion.

HAH and GMD: Better Buffered, but Fixed Contracts Create a Lag

HAH carries an operating margin of approximately 34% and fuel exposure of around 10%, giving it room to absorb pressure without immediate damage. The vulnerability lies in contract structure: most shipping contracts run on fixed-rate terms of 3–6 months, meaning the higher diesel cost eats into margin first, with freight rate adjustments possible only at the next renewal. HAH closed May 21 at VND 55,100 (-1.08%), extending a decline from the previous session.

GMD is in a similar position, with a margin of nearly 49% and fuel exposure of around 8%. Its margin buffer is thicker than HAH's, but GMD also fell for two consecutive sessions, closing May 21 at VND 74,500 (-1.59%). Sentiment in the port and logistics group is being pressured from two directions: declining market liquidity and concern that container throughput could slow if shippers tighten logistics spending.

ACV: Virtually Immune to Direct Impact

ACV sits at the opposite end of the spectrum. With an operating margin of approximately 60% and fuel representing only around 4% of its cost structure, the direct impact from the May 21 adjustment on ACV is negligible. The stock closed May 21 at VND 44,100.

ACV's risk is one layer removed: if airline margins deteriorate sufficiently for carriers to cut flight frequencies, the passenger volumes served at ACV's airports would be affected indirectly. That scenario requires sustained margin pressure across multiple quarters, not a single adjustment cycle. In Friday's session, that risk is too distant to price meaningfully.

Brent and the Supply-Side Signals

How long this pressure persists ultimately depends on Brent crude and the trajectory of US–Iran nuclear negotiations. From May 8 to May 21, Brent traded between USD 101.29 and USD 112.10 per barrel, with no session closing below USD 100. The USD 105–110 zone feeds into Vietnam's import-price calculations with a lag of roughly 10 days, meaning the next adjustment — expected on May 28 — will continue referencing this range absent a major geopolitical shift.

On the supply side, as of May 22, Iran's Supreme Leader ordered the country's stockpile of 60% enriched uranium to remain inside Iran, rejecting a US proposal to export or neutralize the material and slowing the pace of negotiations.CDM Press The move reduces the near-term probability of sanctions relief that would allow Iran to formally increase oil exports. The fact that no session closed below USD 100 over the past two weeks is the clearest signal yet of where the price floor sits.

Framework for Friday's Session

Looking at the numbers, May 22 is the first session in which the transport sector is priced without the stabilization fund acting as a cost shock absorber. VJC and VTP have the thinnest margins and high enough fuel dependency to produce a visible impact, making them the most relevant to watch for intraday moves. HAH and GMD sit in the middle: their real risk materializes more clearly through the next contract renewal cycle when freight rates can be renegotiated. ACV is essentially immune to the direct impact, with indirect risk only if airline pressure becomes prolonged enough to affect flight frequencies.

A genuine reversal signal requires a supply-side catalyst: Brent sustaining below USD 100 per barrel, or a concrete breakthrough in US–Iran negotiations leading to sanctions relief. The next scheduled adjustment on May 28 will be the first data point on whether the current price level holds or begins to ease.