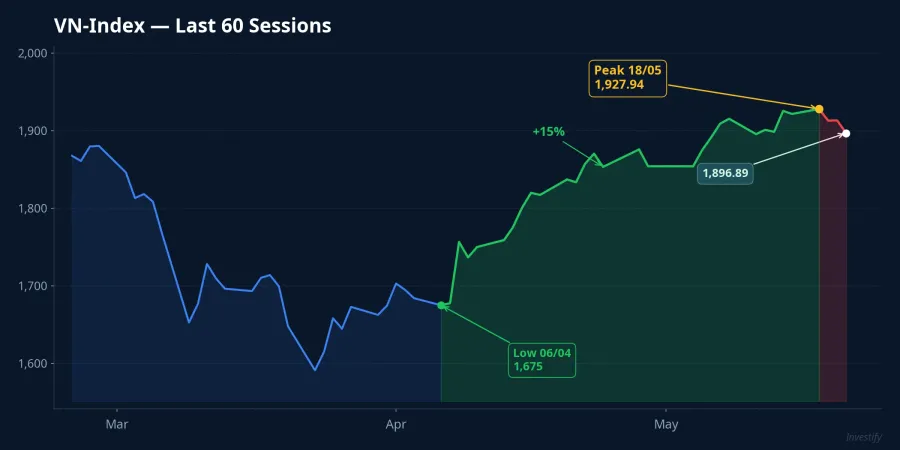

The VN-Index hit an all-time high of 1,927.94 points on May 18, then pulled back roughly 30 points to 1,896.89 over the following two sessions. At the same time, the clock on MSCI's annual market classification review is ticking — the announcement is expected at end of June 2026, roughly five weeks away. The question has moved past "will Vietnam be upgraded?" to something more specific: three distinct outcomes are all plausible, and each one requires a different portfolio response.

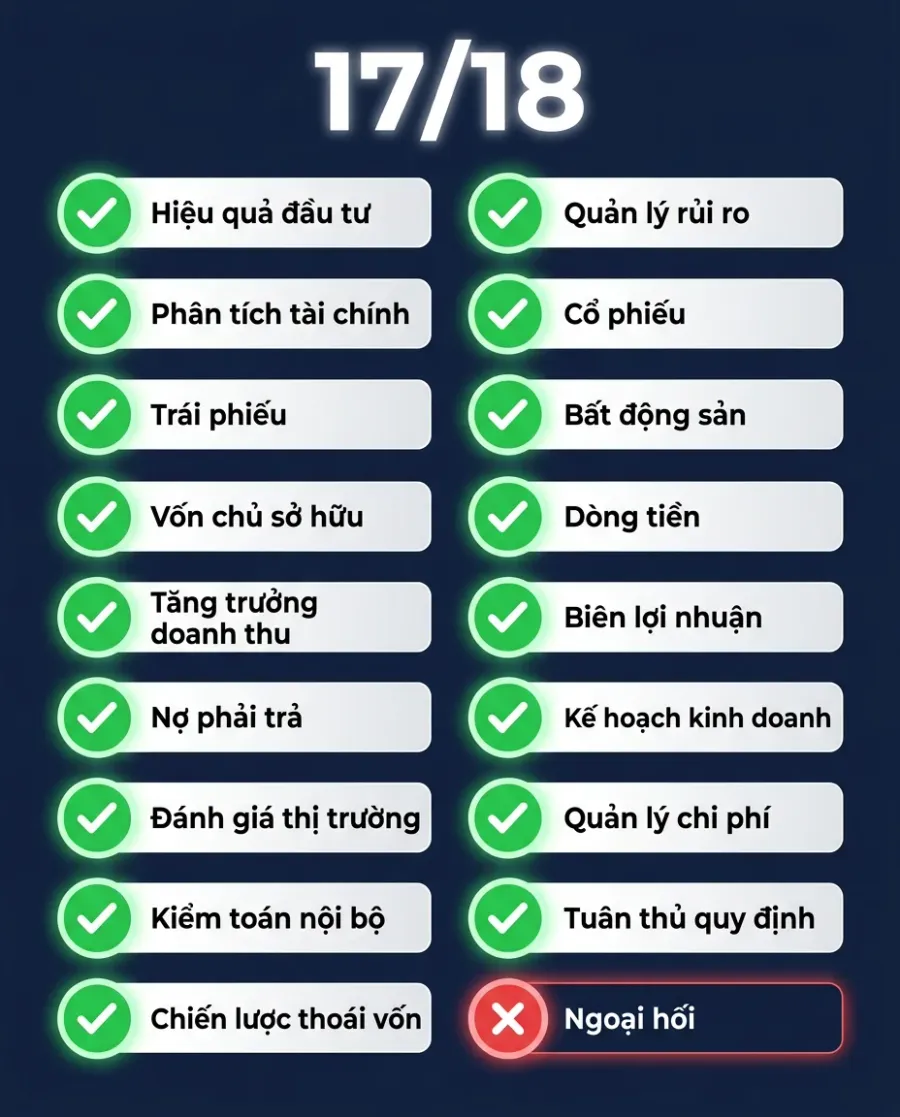

The big picture: SSI Research's May 2026 strategy report upgraded its assessment, noting that 17 of 18 MSCI market access criteria have moved close to a basic level of compliance.CafeF This is a meaningful step up from roughly 10 of 18 criteria recorded as fully met in prior review cycles. The remaining sticking point is the degree of foreign exchange market liberalization, specifically the mechanisms for currency conversion and capital repatriation available to foreign investors.

What makes June 2026 different from last year?

The June 2025 cycle did not add Vietnam to the watchlist. MSCI acknowledged progress on English-language disclosure requirements and the pre-funding mechanism, but the overall assessment was unchanged. Since then, three concrete developments have shifted the landscape.

First, FTSE Russell officially confirmed the roadmap for upgrading Vietnam from Frontier Market to Secondary Emerging Market status, with allocation into FTSE index benchmarks beginning September 21, 2026.VnEconomy This is a significant institutional signal: a major index provider has independently validated Vietnam's market infrastructure against an international standard.

Second, actual foreign ownership on HOSE rose from 41.4% to 46% in April 2026, driven primarily by large-cap companies listed with 100% foreign room.Vietstock The 46% figure represents a clear improvement on the foreign investor access criterion.

Third, the State Bank of Vietnam (SBV) has put out a draft amendment to its foreign exchange management regulations for public consultation, with provisions that would allow commercial banks to offer currency hedging instruments to foreign investors. A critical point: this is still at the consultation stage, not yet issued and not yet in force. The existence of the draft is a supportive signal, but it cannot substitute for regulations that are actually operational.

Scenario A: Added to the watchlist in late June

Distinguishing trigger: the late-June MSCI announcement includes language adding Vietnam to the review list for potential reclassification.

This is where readers often misread the capital flow mechanics. Being added to the watchlist does not automatically pull in passive capital. The watchlist is a signal, not an allocation instruction. MSCI typically keeps a market under review for 12 to 24 months before making a formal reclassification decision. Passive fund inflows only materialize once MSCI announces an effective date for index inclusion.

On estimated scale: SSI Research estimates passive inflows from FTSE-tracking funds following Vietnam's September 2026 upgrade at approximately USD 1.3 billion. With MSCI Emerging Market benchmarks tracking far larger assets than FTSE, market analyses estimate total inflows across the full MSCI EM upgrade process at USD 5 to 6 billion. Vietstock cites a higher figure of approximately USD 20 billion, but that figure is tied to the full MSCI EM inclusion scenario, not the watchlist phase.Vietstock

On which stocks receive the heaviest allocation: MSCI uses free-float adjusted market capitalization as the primary criterion, combined with liquidity and available foreign room. Using the current MSCI Vietnam Index as a reference, the leading names typically include large-caps such as VIC, VHM, HPG, FPT, VCB, MSN, and VNM. Notably, when transitioning from MSCI Vietnam (a frontier benchmark) to MSCI Emerging Market, each stock's weighting will dilute significantly relative to its current frontier weight.

Scenario B: Deferred to the June 2027 review

Distinguishing trigger: the June 2026 announcement acknowledges progress but does not add Vietnam to the watchlist, citing the unresolved foreign exchange criterion.

The SBV's foreign exchange management draft remains at the public consultation stage. The standard issuance process takes several months from consultation closure through formal submission, signing, and entry into force. If the document is still a draft when MSCI closes its assessment window in early June, the organization has grounds to hold Vietnam's classification unchanged for another year. This is not a negative verdict on market quality: it reflects MSCI's procedural discipline. Reforms must be operational, not merely proposed.

Price implications: VN-Index at current levels reflects some probability of watchlist inclusion. If Scenario B materializes, that embedded expectation will need to unwind.

Scenario C: Expectations already priced in too early

This is the least-discussed scenario but arguably the most likely outcome at current price levels.

The VN-Index gained nearly 15% from 1,677.54 points on April 7 to the high of 1,927.94 on May 18, coinciding with the window in which FTSE Russell confirmed its upgrade and SSI Research published its upgraded MSCI assessment.TNCK Part of that run reflects expectations of a June watchlist addition and the September FTSE upgrade, though the precise split between MSCI expectations, recovering global risk appetite, and domestic flows cannot be determined from available evidence.

Over May 19 and 21, the VN-Index fell roughly 30 points to 1,896.89 — the first sign of investors trimming positions near the peak. The "sell the news" dynamic operates even when the news is positive: once the market has fully priced in an expectation, the actual confirmation no longer provides fresh upside.

Mapping outcomes onto this framework:

If MSCI adds Vietnam to the watchlist but the announcement carries no decisive new language on the forex criterion, the market can still pull back through "sell the news" mechanics. If MSCI does not add Vietnam (Scenario B), a 5 to 8% correction from the 1,900 to 1,930 range is a typical outcome for "bad news after high expectations." If MSCI adds Vietnam with clearly positive guidance on the forex reform timeline, the index may break above the 1,927.94 peak.

Three signals to watch over the next five weeks

Smart money is tracking three specific signals to identify which scenario is taking shape.

Has the SBV's forex draft been submitted for approval? This is the strongest leading indicator MSCI can observe that reform is moving from consultation toward implementation. If the document advances from public consultation to formal submission before MSCI closes its assessment window in early June, there is a meaningful improvement in the weight of evidence for Scenario A.

Official communication on CCP (central counterparty) progress. SSI Research assessed the CCP implementation timeline as on track.CafeF Any signal of delay from the Ministry of Finance or the State Securities Commission would be a mark against Scenario A.

Foreign block flow in the final week of May and early June. Continued net buying by foreign investors suggests the market is pricing Scenario A as the higher-probability outcome. A shift to net selling in MSCI Vietnam-constituent names would suggest institutional hedging against Scenario B.

Risk/reward at the peak

The bullish case rests on the pace of the forex draft through the approval pipeline and confirmation that CCP is on schedule. The cautious case rests on the gap between a draft under consultation and a regulation that is actually in force. The deciding factor is the real-world progress on both milestones before MSCI closes its assessment.

What is already observable: after a nearly 15% gain from early April, the risk/reward balance at current peak levels is meaningfully less attractive than it was in April. Watchlist expectations and the FTSE upgrade have been partially priced in. The three signals above — forex draft progress, CCP timeline, and foreign block flow — will show which scenario is tracking toward confirmation before MSCI's official announcement at end of June.