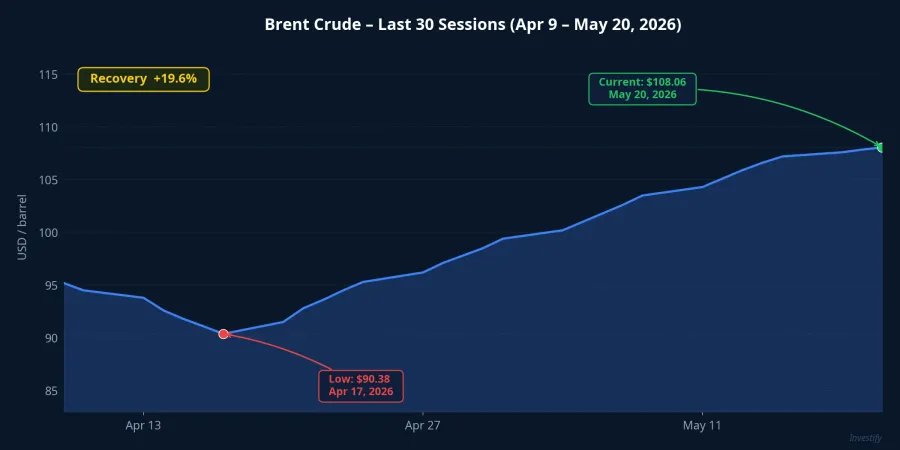

By the close of May 20, Vietnam's Fuel Price Stabilization Fund (BOG) held just VND 199.92 billion — essentially nothing relative to the domestic market's weekly consumption. At the same time, Brent crude had rebounded nearly 20% from its April 17 low of USD 90.38/barrel, closing May 20 at USD 108.06/barrel. Pressure has accumulated precisely when the buffer is thinnest, and Thursday's price adjustment cycle will be the first real test of the government's capacity to intervene this round.

How the BOG Mechanism Works and What Resources Remain

Under Decree 80/2023/ND-CP, Vietnam's retail fuel prices are reviewed and adjusted on a 7-day cycle every Thursday. The Joint Ministry of Industry and Trade alongside the Ministry of Finance can draw on the BOG fund to soften the impact of global price spikes. When the fund runs dry, retail prices track world crude without any cushion.

In late March, the government issued Resolution 69/NQ-CP (March 27, 2026), authorizing a VND 8,000 billion advance from excess central budget revenue of 2025 to replenish the BOG fund.CafeF Circular 19, effective April 3, 2026, spells out the allocation mechanics: a maximum advance of VND 5,000 per litre for diesel and VND 4,000 per litre for petrol per 7-day cycle, disbursed through escrow accounts held by major distributors.

A critical structural point: the VND 8,000 billion is a loan from the budget, not a grant, and must be repaid within 12 months. Every draw on the advance in Scenario 1 pulls from that ceiling, and the repayment clock starts with the first activation.

At the May 14 adjustment cycle, the Joint Ministry again did not draw on the BOG fund and let prices track the calculation period. As a result, E5 RON92 fell to VND 23,134/litre (down VND 656), RON95 to VND 24,078/litre (down VND 276), and diesel to VND 27,226/litre (down VND 268). The fund was neither refilled nor drawn upon; the balance simply sat near zero.

Brent Up Nearly 20%: Pressure Building Into May 21

The oil market picture has shifted materially since mid-April. From the USD 90.38/barrel trough on April 17, Brent has climbed steadily, trading in the USD 105–112/barrel range throughout the second half of May. A sharp intraday sell-off on May 6 briefly touched USD 101.27/barrel, but buying absorbed the dip quickly and USD 108/barrel is now holding.

The current USD 108/barrel level is meaningfully above the average embedded in the May 14 calculation (around USD 105/barrel). Per market estimates, the May 21 adjustment cycle could push RON95 and diesel up by VND 1,000–1,500/litre in the absence of fund intervention.Techz That magnitude of increase is sufficient to pass through meaningfully into operating costs for fuel-intensive businesses.

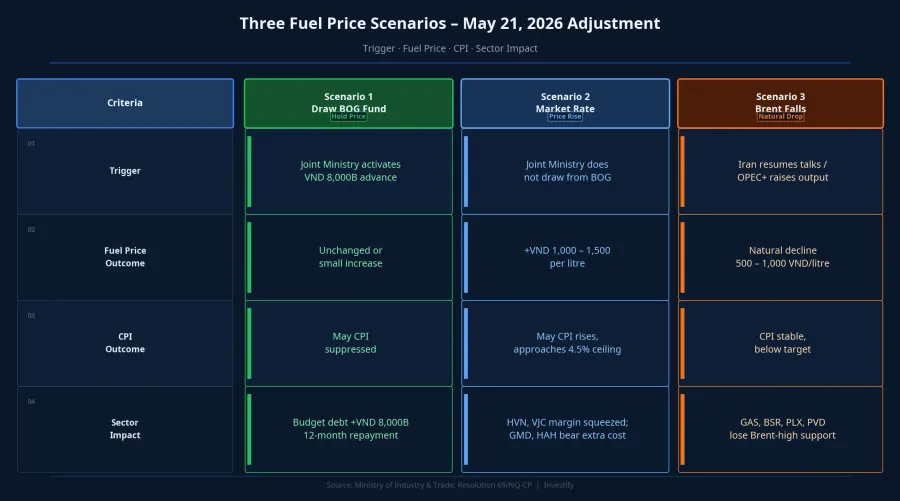

Three Scenarios and Their Differentiating Triggers

Three distinct policy paths are now open ahead of the May 21 adjustment. Each has a different trigger and a different set of market consequences.

Scenario 1: Activate the VND 8,000B advance, draw the fund to hold prices. If the Joint Ministry announces a BOG draw alongside advance allocations to major distributors (Petrolimex, PVOIL, and private wholesalers), retail prices for May 21 could stay flat or tick up by only a few hundred dong. May CPI in the transport category would be capped. The burden does not disappear, however. It shifts from pump prices to the central budget, on a 12-month repayment schedule. If Brent stays above USD 105/barrel for several months, the room to intervene via the fund will shrink with each successive draw.

Scenario 2: Let prices adjust to market. If the Joint Ministry declines to draw the fund and does not activate the advance, retail prices at the May 21 cycle could rise by VND 1,000–1,500/litre. On the macro side, CPI for April 2026 had already reached 5.46% year-on-year (the four-month average came in at 3.99%).Thị trường Tài chính Tiền tệ A 5–7% fuel price increase feeding through to the transport CPI component would push the May reading close to the year-end ceiling. This scenario relieves the budget but transfers pressure directly to margins at fuel-intensive firms.

Scenario 3: Brent retreats, pressure resolves organically. The trigger here lies outside Vietnam's control: renewed Iran nuclear talks, an OPEC+ output increase at the June meeting, or a USD index rally that depresses nominal crude prices. If Brent returns to the USD 95–100/barrel range and holds for one calculation period, the following adjustment cycle could naturally deliver a VND 500–1,000/litre decrease without any fund involvement. This is the most benign outcome, but it depends entirely on geopolitics and OPEC+ decisions.

Which Sectors Bear the Pressure, Which Benefit

Viewed from an investor's perspective, each sector cohort is sensitive to a different branch of this framework.

Aviation (HVN, VJC) carries the highest sensitivity to Scenario 2. Fuel represents a large share of airline operating cost structures, and fuel surcharge adjustment cycles typically lag actual price moves. HVN closed May 20 at VND 21,200; VJC closed at VND 170,600. The signal to watch is any official fuel surcharge announcement from the Civil Aviation Authority of Vietnam.

Maritime freight and logistics (GMD, HAH) are sensitive to both Scenario 2 and the lag in BAF (Bunker Adjustment Factor) revision, which tracks international bunker prices with a shorter delay than domestic aviation surcharges. GMD closed at VND 77,900 and HAH at VND 55,700 on May 20. The signal to monitor is the June BAF schedule from major shipping lines.

Seafood exporters (VHC) face indirect exposure through export logistics costs rather than direct fuel dependency. VHC closed at VND 58,200 on May 20. The relevant signal is Q2 gross margin data from companies exporting to the US and EU.

Oil and gas equities (GAS, BSR, PLX, PVD) benefit indirectly while Brent holds high in Scenarios 1 and 2. Risk materializes in Scenario 3: if Brent slides to the USD 95–100/barrel range, the high-crude support underpinning current valuations would weaken.

Signals to Read on Thursday Afternoon

Per the regulatory calendar, the Joint Ministry will publish updated prices before 3:00 PM on May 21. The two most consequential lines in that announcement are: (1) whether the BOG fund is being drawn for this cycle, and (2) whether regular fund replenishment contributions are being reinstated.

A draw on the BOG fund accompanied by advance allocation to distributors means the government has chosen Scenario 1: protect pump prices now, accept higher budget exposure. No draw with a market-rate increase signals Scenario 2, and the aviation and logistics sectors face immediate margin pressure in Q2. A price decrease, if it materializes, would indicate that Brent's move during the calculation period already triggered a partial Scenario 3.

One point to keep in mind regardless of how May 21 resolves: the VND 8,000 billion advance is a finite, repayable facility. If Brent anchors above USD 105/barrel for several months running, the choice set gradually narrows to accepting higher CPI or waiting for the market to self-correct. This is not a question that one adjustment cycle resolves.