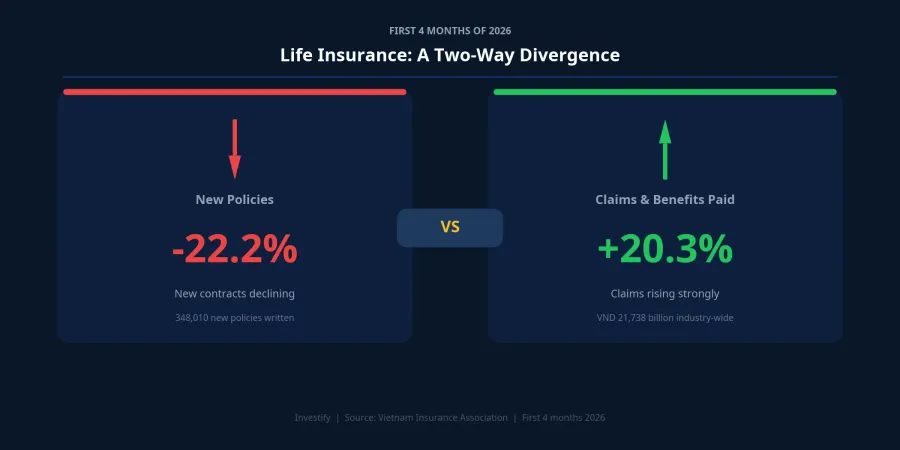

On the morning of May 20, the Vietnam Insurance Association released industry data for the first four months of the year. Two numbers tell the story: new policy sales down 22.2%, benefit payments up 20.3%. One side contracting, the other expanding, in the same market, over the same period. This is not a short-term fluctuation. This is how a business cycle settles its accounts.

The life insurance industry wrote 348,010 new policies in the first four months of 2026, down 22.2% from the same period in 2025.Tin nhanh Chứng khoán New premium revenue is estimated at VND 6,653 billion, down 11.5%. Total market premium revenue for the four months reached VND 43,398 billion, down 4.3%. This is the third consecutive year the industry has recorded a decline, following three years of regulatory overhaul in the aftermath of the bancassurance scandal.

The 2021 Peak: Banks as Growth Engines

To understand why 2026 looks the way it does, we need to look back. In 2021, new premiums channeled through banks grew nearly 58% compared to 2020, accounting for 41.4% of total new premiums across the industry.Tin nhanh Chứng khoán The model was efficient: banks had a ready-made base of savings customers; insurers had investment-linked products that looked, to many customers, like a higher-yielding savings account. Exclusive distribution agreements between major insurers and banks — Manulife with SCB, Prudential with MSB, Dai-ichi with Sacombank, AIA with VPBank — carved the market into separate territories.

In the first half of 2022, Manulife surged to the top spot for new premiums with VND 4,685 billion, overtaking both Prudential at VND 4,490 billion and Bao Viet Life at VND 2,678 billion.VietnamBiz The top five insurers collectively recorded VND 17,372 billion in new premiums in just six months. For full-year 2022, the bancassurance channel still posted 45% YoY growth. From the outside, no one called it a peak.

The 2022–2023 Scandal: The Trust Collapse

Beginning in late 2022 and throughout 2023, a wave of complaints broke out. Savings customers at SCB alleged that bank staff had pressured them into signing investment-linked insurance contracts under the impression they were a higher-yielding savings product. Manulife, as SCB's distribution partner, became a focal point alongside SCB after the bank was placed under special supervision in late 2022. These grievances emerged at multiple banks and across multiple insurers, not limited to any single partnership.

Vietnam's Ministry of Finance opened a complaints hotline and required insurers to review their policyholder records. Some customers received contract cancellations and premium refunds. But the loss of trust in the bancassurance channel as a whole — not just in Manulife or SCB — fell to a level that cannot be quickly recovered. That invisible loss is larger than any refund amount.

The 2023 Regulatory Reform: Closing the Shortest Route

The Insurance Business Law 2022 took effect on January 1, 2023.TLA Law Decree 46/2023/ND-CP and Circular 67/2023 then imposed three direct constraints on bank-based insurance distribution. First, physical separation of insurance advisory areas from banking transaction areas, along with staff training requirements and technology systems to record advisory sessions. Second, a ban on selling investment-linked insurance products during the 60-day window before and after the full disbursement of any loan, the window where mis-selling had been most prevalent. Third, a prohibition on conditioning loan products on insurance purchases and on setting insurance sales targets for credit staff.

On paper, this was a comprehensive technical tightening. In practice, it shut down the most direct channel insurers had relied on to reach new customers for six years. The agency channel — more expensive and slower to scale — had to absorb the bulk of the recovery burden without the capacity to compensate quickly.

Three Years On: The Market Has Not Found a Bottom

By the first four months of 2026, the market's structure had shifted meaningfully. Investment-linked insurance still held a 55.7% market share but fell 23.6% year on year; within that, the universal-link segment — the most widely sold product through banks during 2020–2022 — declined 27.7%. The top-five ranking for new premiums has reversed completely compared to the first half of 2022: Bao Viet Life now leads with VND 1,445 billion, followed by Dai-ichi Life at VND 703 billion, AIA at VND 662 billion, Manulife at VND 629 billion, and Techcom Life at VND 570 billion. Manulife has fallen from first place in the first half of 2022 to fourth.

What stands out in these figures is how far absolute volumes have contracted. In the first half of 2022, Manulife alone recorded VND 4,685 billion in new premiums in just six months. In the first four months of 2026, the entire top five combined reached roughly VND 4,000 billion. This contraction reflects a combination of factors: eroded trust, tighter regulations, and investment-linked products viewed differently by customers who watched policy fees erode account values in the early years of their contracts.

Claims Up 20.3%: Understanding the Source

Claims and benefits paid by insurers reached an estimated VND 21,738 billion in the first four months of 2026, up 20.3% from the same period in 2025.Báo mới Read in isolation, this number can be mistaken for a warning sign. The reality is different: this is the fulfillment of obligations under policies written during 2018–2022, now coming due, including death claims, critical illness payouts, policy maturities, and mid-term cancellations. With a large existing policy base still in force, claim outflows follow the natural pace of an inherited book, independent of new sales momentum.

There is, however, a more telling angle. The industry-wide claims ratio climbed from around 50% during 2023–2024 to 54.08% in 2025 and continued rising in Q1/2026. International benchmarks place 55% as the threshold at which profit margins come under meaningful pressure. Add to that the higher distribution costs of the agency channel relative to bancassurance, and the insurance underwriting business is operating in a thin-margin cycle.

BVH Q1/2026: Look Past the Headline

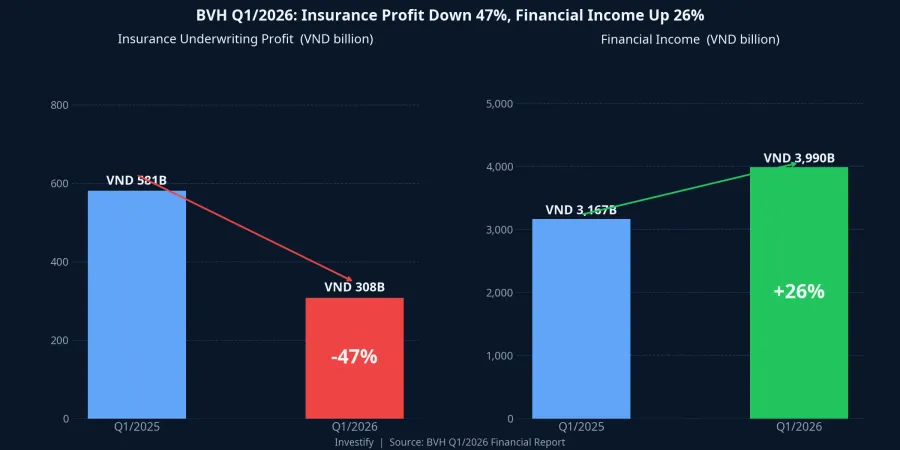

Bao Viet Group reported consolidated pre-tax profit of VND 1,006 billion for Q1/2026, up 18.7% year on year.Báo Đấu thầu A quick read suggests this is good news for the sector. But the profit breakdown tells a different story.

Net revenue from insurance operations reached VND 9,819 billion, down a modest 2%; insurance underwriting gross profit fell to just VND 308 billion, down 47% year on year. The gain came entirely from financial activities: VND 2,290 billion in deposit interest income (up 36%), VND 1,401 billion in bond interest (up 16%), totaling VND 3,990 billion in financial revenue, up 26%. The life insurance business model permits this, since collected premiums are invested, and a large legacy portfolio accumulated during the peak years is earning well above what the underwriting business generates.

The formula holds only as long as interest rates remain elevated. Big 4 deposit rates have already retreated to the 5.5–6% range, and government bond yields are even lower. If the rate cycle continues downward in coming quarters, the financial pillar will be compressed precisely when insurance underwriting has not yet recovered.

BVH Stock: What the Market Is Pricing In

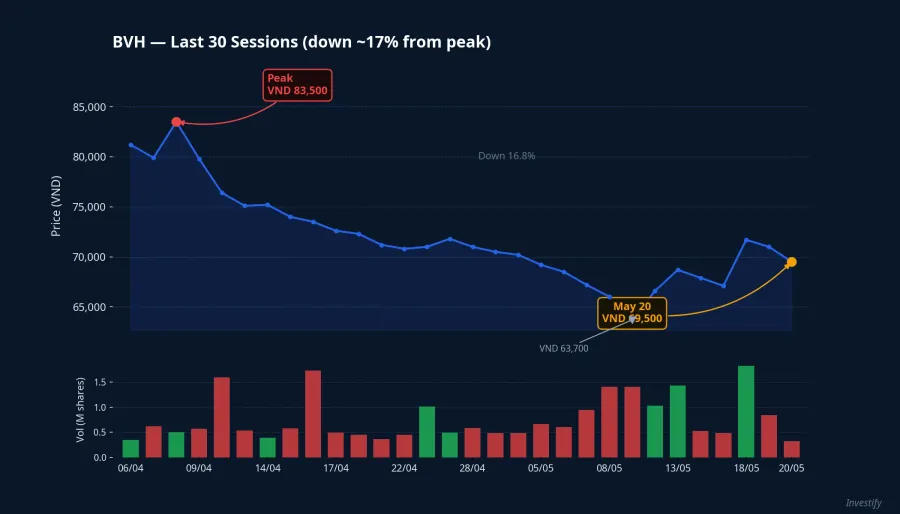

BVH shares fell from around VND 83,500 in early April to VND 69,500 on May 20, a decline of approximately 17% in six weeks. This drop does not stem from Q1 results, which remained positive in aggregate profit terms. The more compelling explanation is that the market is repricing structural risk: when underwriting profit is squeezed to VND 308 billion and financial income becomes the load-bearing pillar, valuation must reflect dependence on the interest rate environment.

BVH's P/B has come down, but a lower P/B does not automatically mean cheap when neither of the two foundational variables is stable. The recovery pace for new policy sales has shown no clear bottom after three years, and interest rates, while currently holding, could shift in the next cycle.

What This Means for Individual Investors

For those currently holding investment-linked insurance policies purchased through bank channels during 2020–2022, the 20.3% rise in benefit payments does not affect individual policy entitlements. Obligations under each policy are backed by the insurer's technical reserves, independent of new business volumes. The factors worth monitoring are the investment quality of the linked fund allocated to your policy and the insurer's solvency margin.

For investors considering BVH shares or the listed insurance sector more broadly, the analytical framework centers on two variables. The first is the pace of recovery in new policy sales: after three consecutive years of decline, there is no clear bottom in sight. The second is the interest rate environment: currently holding, but a rate reduction cycle could arrive. The signal of a sector turning point will come from the new business number — not from the consolidated profit headline.

This is not an industry that has hit its cycle bottom. This is an industry settling obligations from its peak years while it has not yet rebuilt a new customer base large enough to compensate.