FPT Corp closed at VND 74,500 on May 19, sitting at its lowest price in more than two years. On May 11, the stock touched VND 70,000, a level not seen since early 2024. Year-to-date from January 1, FPT has shed roughly 25%, equivalent to more than VND 40,000 billion in market capitalization evaporating from its peak.CafeF

Looking at those numbers, it is easy to conclude that something is wrong with the business. But the operating data tells a different story: in April 2026, FPT's overseas IT services division recorded new contract bookings of VND 6,143 billion, up 58.4% year-on-year.Elibook Two data streams pulling in opposite directions — that contradiction is the starting point for reading what is really happening at the VND 74,500 price level.

Business Results: No Cracks in the Numbers

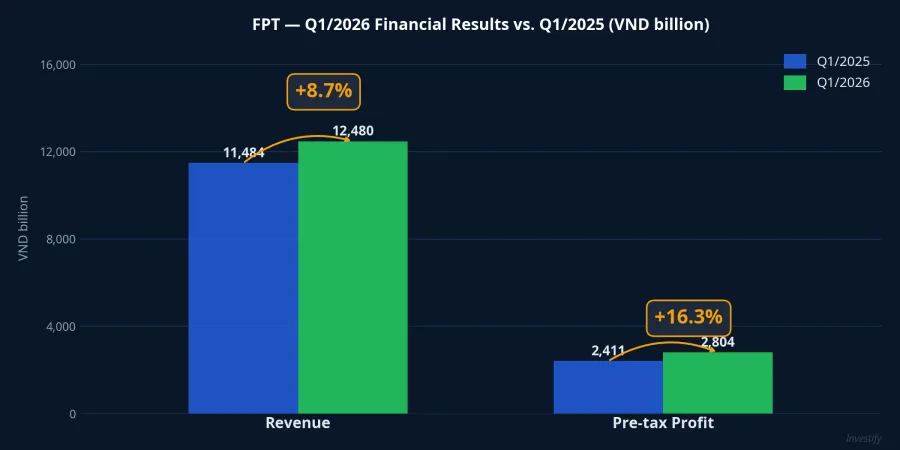

In Q1 2026, FPT posted consolidated revenue of VND 12,480 billion and pre-tax profit of VND 2,804 billion, up 8.7% and 16.3% respectively year-on-year.VnEconomy Net profit attributable to parent company shareholders came in at VND 2,487 billion, up 14.4%, with EPS rising 13.7% to VND 1,460.

What stands out is the quality of new wins: FPT secured 8 contracts each valued above USD 10 million in Q1, indicating that the company is moving toward higher-value engagements rather than simply adding volume on smaller outsourcing work. New contract signings in the overseas IT segment grew 22.2% year-on-year in the quarter.VnEconomy

For the first four months of the year combined, revenue reached approximately VND 24,000 billion and pre-tax profit approximately VND 3,800 billion.Nguoi Quan Sat The company's full-year 2026 plan calls for revenue of VND 58,580 billion and pre-tax profit of VND 11,629 billion, representing growth of 16% and 15% respectively. At the current run rate, FPT appears on track to meet its annual targets.

Valuation Has Compressed to a 5-Year Low

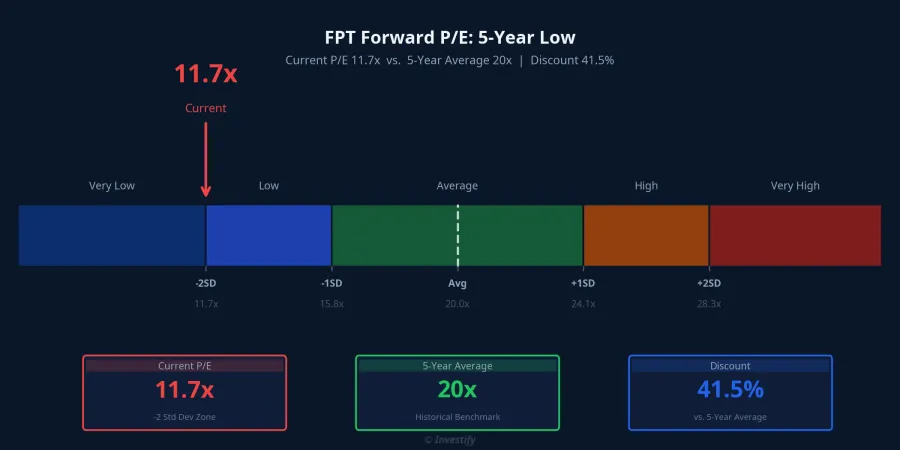

This is where the data becomes most interesting. FPT's 2026 forward P/E currently stands at 11.7x, placing it roughly 2 standard deviations below its 5-year average of 20x, per BSC's estimates. In other words, the same company with the same core business is being priced significantly cheaper than its own historical norm over the past five years.

Notably, BSC itself lowered its target P/E from 20x to 15x, resulting in a revised price target of VND 90,600, which is 28% below its previous estimate.Chungta This is not a pure bullish call. BSC maintains a positive view on cash flows and contract momentum while simultaneously acknowledging that the market has legitimate reasons to re-rate FPT's growth story, reflecting that acknowledgment by cutting the target multiple. The outcome: a stated upside of 24% versus the May 18 close, per BSC's recommendation.StockBiz

Why the Stock Fell: Two Forces Unrelated to Q1 Results

Looking at the operating numbers, FPT has not shown signs of fundamental deterioration. The price decline originates elsewhere — and the two main forces are both independent of the company's near-term financial performance.

Force one: sustained foreign net selling. Since the start of the year, foreign funds have been selling FPT shares on HOSE in meaningful volume. Foreign ownership has retreated noticeably after months at the cap. The resulting wider foreign room reflects this selling, creating supply pressure in the market rather than any operational weakness. This is also where FPT has limited near-term control: an open foreign room could attract fresh foreign capital back in, but it could also widen further if the selling wave continues.

Force two: AI concerns eroding outsourcing margins. This is a structural risk that a single strong quarterly report cannot dismiss. As AI coding models become cheaper and more capable of automation, the direct question is whether clients will continue paying the same rates for the same volume of outsourced IT services.

On the other hand, FPT is actively repositioning its portfolio: revenue from AI/Data is growing rapidly, and the company is pushing higher-value digital transformation services over traditional outsourcing. Whether this shift can keep pace with the speed at which AI compresses margins remains an open question that current data cannot yet answer.

Beyond those two main forces, JPY/USD volatility adds a smaller headwind. USD/JPY has risen roughly 7% over the past 12 months while USD/VND has been far more stable. Revenue from the Japanese market, when converted to VND, faces pressure from a weaker yen, though this effect is generally smaller than the two primary forces described above.

Three Signals to Watch in the Coming Months

At a forward P/E of 11.7x, the price has already discounted quite deeply both the AI risk and the foreign selling pressure, relative to FPT's own valuation history. BSC's 24% upside estimate rests on two assumptions: FPT sustaining profit growth of 15–16% through 2026–2027, and the market accepting a P/E recovery to 15x (not the 20x of the previous cycle).

Against that framework, three signals are worth monitoring:

Signal 1: Do new monthly contract signings sustain double-digit growth? April's record VND 6,143 billion is encouraging, but two to three more months of data are needed to confirm whether this is a durable trend or an exceptional single month.

Signal 2: Does foreign ownership show signs of re-accumulation? This variable is driving near-term price action more than any business metric. If the foreign room starts narrowing again, market sentiment toward FPT could shift fairly quickly.

Signal 3: Does Q2 — due late July — confirm that gross margins are holding despite AI pressure? If the overseas IT segment's gross margins remain stable under AI headwinds, that would be the strongest evidence pushing back against the "AI is eroding FPT" thesis.

The VN-Index closed May 19 at 1,912.93 points, pulling back roughly 15 points from the prior session's peak. With the broader index retreating from highs, large-cap stocks whose valuations have compressed sharply — like FPT — represent one of the few areas worth monitoring closely. The question is not whether FPT is cheap: at 11.7x P/E against a 5-year history, the answer is fairly clear. The real question is which signal on foreign fund flows and May contract bookings will arrive early enough to confirm or refute the recovery thesis.