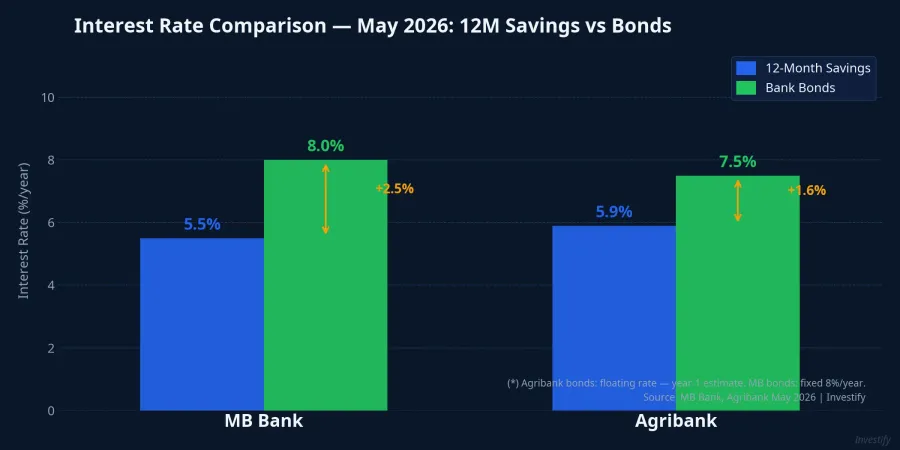

In May 2026, the same bank, at the same time, offers two products with very different returns. An Agribank customer depositing for 12 months earns 5.9% per year.VietnamBiz A buyer of MB Bank's newly issued 7-year bonds earns 8% per year, fixed for the full term.Báo Pháp Luật The 2.1 percentage-point gap is not a pricing error or a promotional gimmick. It is the premium banks must pay to pull funding out of the short-tenor zone and into the long end of the curve.

Here is the simple version: banks need long-term money to make long-term loans, but the vast majority of depositors prefer short tenors. To bridge that gap, banks must pay more. And that extra 2.1 percentage points is not free money for bond buyers. It is the price of four structural trade-offs.

The mechanism: why banks need long-term capital

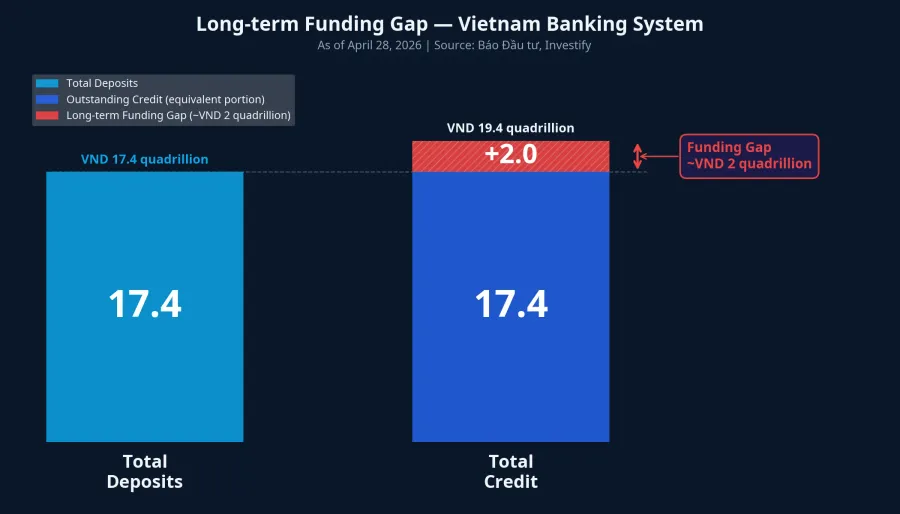

Most deposits in Vietnam's banking system today have tenors under 12 months. But outstanding credit — home loans, project financing, infrastructure lending — typically runs 5 to 15 years. Those two figures do not match, and the gap between them is what practitioners call the long-term funding gap.

As of April 28, 2026, total outstanding credit in the banking system reached VND 19.4 million billion, up 18.26% year-over-year, while deposit growth lagged significantly. The gap between credit and deposits has grown to approximately VND 2 million billion.Báo Đầu tư

In theory, a bank can fund a 10-year loan with rolling 12-month deposits, as long as depositors keep renewing. But the State Bank of Vietnam caps this practice. Under Circular 08/2020, the maximum share of short-term funding that can be used for medium- and long-term lending is 30%, a cap that took effect on October 1, 2023, stepped down from the prior 40% limit.Thư viện Pháp luật When a bank approaches that 30% ceiling, it must source funding with tenors longer than 12 months. Bonds maturing in 7 to 10 years are the most important channel for doing so.

There is an additional dimension: Agribank's newly approved bond issuance counts toward Tier-2 capital, a component of the capital adequacy ratio (CAR) under Basel II.Stockbiz Unlike ordinary deposits, every baht raised through this channel serves three purposes simultaneously: long-term funding, compliance with the 30% cap, and a boost to regulatory capital buffers. That is why banks are willing to pay significantly above their deposit rates.

Circular 08/2026, which took effect on May 15, adds 20% of State Treasury deposits to the LDR denominator, reducing the LDR of state-owned banks by roughly 1.1 to 1.5%.Dân Việt This helps with overall liquidity ratios but does nothing to close the maturity gap. Pressure to issue long-term bonds remains intact heading into the second half of the year.

Four things to understand before comparing 8% with 5.9%

Seeing 8% next to 5.9%, many people will quickly conclude bonds are the better deal. That logic is partially correct, but it needs to be weighed against four structural differences, each of which directly affects your wallet in specific scenarios.

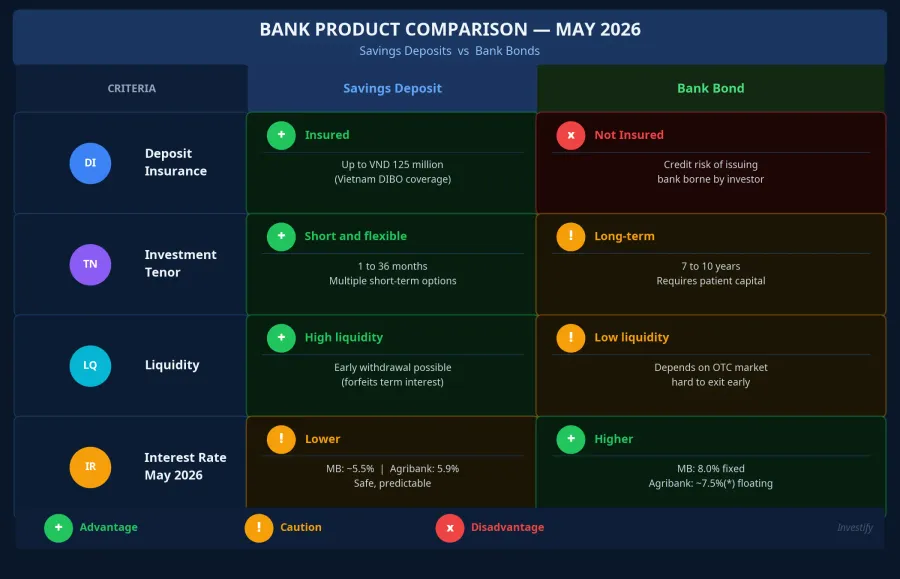

First: deposit insurance. Individual deposits at banks participating in the deposit insurance scheme are covered up to VND 125 million per depositor per bank under the Deposit Insurance Law.Báo Chính phủ Bank bonds fall outside this coverage entirely. The credit risk of the issuing institution rests with the investor. For MB Bank and Agribank, the practical risk is low, but the legal frameworks governing these two products are entirely different.

Second: tenor. A 12-month deposit can be withdrawn early at any time, forfeiting only the term interest rate and reverting to the demand rate. A bond with a 7-to-10-year maturity is meant to be held to term. To exit early, you must find a buyer in the secondary market, and the sale price depends entirely on supply and demand at that moment, which may be below par value if market interest rates have risen.

Third: liquidity. Private-placement bank bonds trade primarily in the OTC market, with no centralized exchange like the stock market provides. Finding a buyer for a specific bond code can take days to weeks. Some issuances are subsequently listed on HNX (Agribank received approval to list VND 10,000 billion of an earlier issuanceBáo Đầu tư), but that is the exception, not the rule.

Fourth: rate structure. MB Bank pays a fixed rate of 8% per year for the full 7-year term, locking in a high yield in the current low-rate environment. Agribank pays a floating rate referenced to the average 12-month rate of the Big 4 banks plus a spread. If rates rise over the next 10 years, Agribank bondholders benefit; if rates fall, their yield falls with them. The two structures suit two different interest rate outlooks, and neither is categorically superior.

Who should consider bank bonds

Most issuances like those from MB Bank and Agribank are private placements, open only to professional securities investors, defined as those with an average portfolio of at least VND 2 billion over 180 consecutive days. Investors who do not meet that threshold have two options: wait for a public offering (Agribank ran one in 2023 with more accessible denominations), or gain indirect exposure through open-ended bond funds on fintech platforms.

The practical framework is straightforward. If your investment horizon is under 12 months, Big 4 savings deposits at 5.9% with VND 125 million insurance coverage remain the most widely used defensive option. If you have patient capital for 3 to 5 years and can tolerate moderate risk, Tier-2 bonds from Big 4 or large private banks (MB Bank, ACB, VCB, BIDV) at roughly 2 percentage points above deposit rates represent a layer worth considering. The allocation, however, should not exceed the share of your portfolio that you can afford to lock up in the event you need liquidity before maturity.

Other fixed-income products on the market — open-ended bond funds and fixed-rate products on fintech platforms — typically offer better liquidity but cannot match the 8% yield available directly from an issuing bank. That is the classic trade-off between yield and flexibility.

Signals to watch in Q3

The 2.1 percentage-point gap is not a free premium. It is the compensation investors receive for accepting a 7-to-10-year tenor, forgoing deposit insurance, and depending on the secondary market if they need to exit early. The two products serve different needs, and there is no universally "better" answer. There is only the answer that fits each person's specific financial situation.

The most important signal to track heading into Q3 2026: Agribank's planned issuances in Q2 and Q3. If a public offering materializes, the question of minimum denominations and distribution channels will be answered, potentially opening this product up to a much broader retail audience.