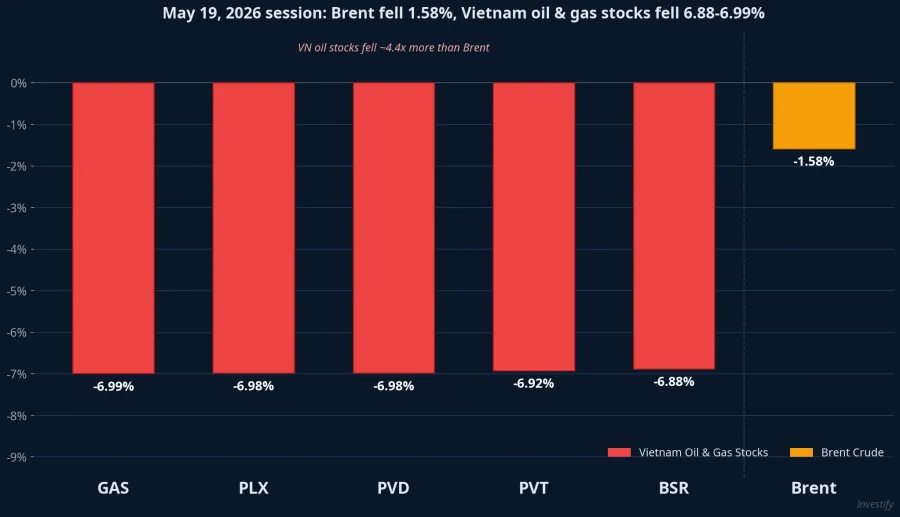

May 19 presented a clear paradox: international Brent crude fell just 1.58% on the day, yet every major Vietnamese oil and gas stock hit its trading floor limit. GAS fell 6.99% to VND 86,500; PLX fell 6.98%; PVD fell 6.98%; PVT fell 6.92%; BSR fell 6.88% to VND 31,150. The VN-Index dropped more than 15 points to close around 1,912.93.Tuổi Trẻ

Two figures sit uncomfortably side by side: global crude fell 1.6%, Vietnamese oil stocks fell nearly 7%. The transmission ratio was more than four times over. This is exactly the opposite of what retail investors holding these names expected. Their thesis had been simple: "Brent staying high is reason enough to hold."

One Month Back: Stocks Had Already Priced In the Brent Rally

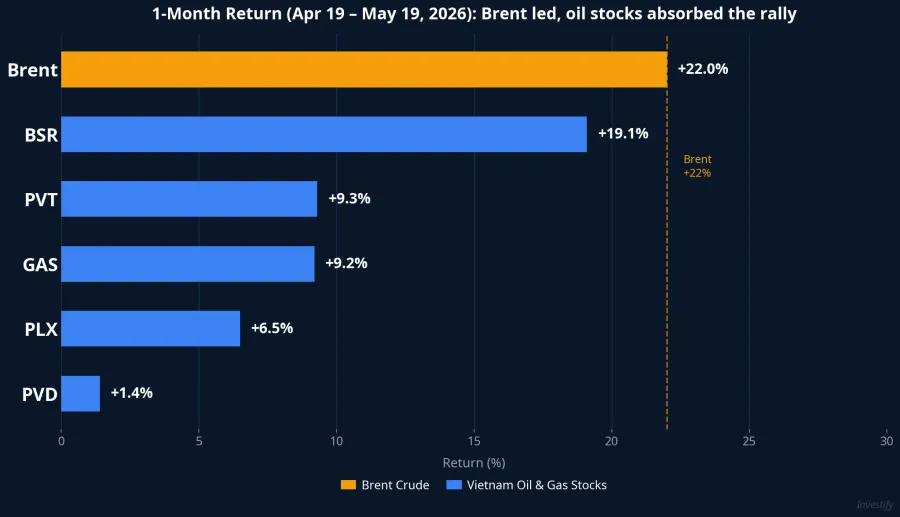

To understand May 19, you need to look at where the group started 30 days earlier. From April 19 to May 19, Brent rose approximately 22% from the $90 range to $110.32 per barrel. The rally had real foundations: geopolitical tensions around Iran, uncertainty in Middle Eastern supply, and global risk-off flows toward energy assets.

Vietnamese oil stocks moved accordingly: BSR rose 19.1%, PVT rose 9.3%, GAS rose 9.2%, PLX rose 6.5%, and PVD gained just 1.4%. Looking at those numbers, what stands out is not the absolute returns but the relationship to Brent. Brent moved 22%; the best stock in the group moved 19.1%; most moved only 6–9%.

This has a specific implication. The current Brent price level was already priced into the stocks. Equities don't pay for today's price; they pay for the next expectation. Once Brent plateaued around $110 with no new catalyst, stocks had no reason to keep rising. At that point, even a modest Brent pullback was enough to trigger a wave of profit-taking.

Five Names, Five Different Sensitivity Mechanisms

The reason many retail investors were caught off guard on May 19 is that they treated the oil and gas sector as a homogeneous block. In practice, each stock responds to Brent through a fundamentally different mechanism.

BSR is an oil refiner. Its profits depend on the crack spread: the margin between refined product prices (gasoline, diesel, jet fuel) and crude input cost. Brent is BSR's raw material cost. A rising Brent does not automatically help BSR unless the spread widens proportionally. In Q1 2026, BSR posted solid results because the crack spread expanded. But there have been periods in 2025 when Brent was high and the spread narrowed, compressing BSR's gross margin.

PLX is a petroleum distribution network. Retail prices are adjusted on a 7-day administrative cycle, so the benefit of rising Brent reaches PLX with a lag. PLX also carries roughly 20 days of inventory, meaning a sharp Brent reversal feeds directly into inventory losses. The scenario where Brent moves sideways at elevated levels — without continuing higher — is the least attractive for PLX: the tailwind from the old trend is exhausted, but inventory risk remains.

GAS is a gas, LPG, and condensate conglomerate. Its domestic gas business operates under regulated pricing and long-term supply contracts, giving it much lower sensitivity to short-term Brent moves than the market typically assumes.

PVD provides drilling services to oil fields. This company doesn't benefit from Brent on any given day; it needs Brent to stay high long enough for field operators to sign new drilling contracts. Until rig rental rates and utilization rates show a clear break higher, PVD will remain the weakest responder in the group. The one-month data confirms it: PVD rose just 1.4% while Brent rose 22%.

PVT provides maritime transport services to the oil industry. Its revenues depend on cargo volume and voyage distance, not directly on Brent.

Five stocks, five different mechanisms, five different Brent sensitivities. When people say "Brent is high so oil stocks should go up," they're collapsing all that complexity into a one-to-one relationship that doesn't exist in practice.

BSR and the Mechanical Demand from VN30 Rebalancing

For BSR specifically, May 19 carried an additional, distinct layer: mechanical demand from an index event that had already run its course.

From mid-April onward, anticipation of BSR's addition to the VN30 index pushed the stock progressively higher from around VND 26,150. When the VN30 was officially updated on May 13, replacing DGC, VN30-tracking ETFs were required to purchase an estimated 3 million-plus BSR shares to rebalance their portfolios.Nhà Đầu TưMekong ASEAN That forced buying drove BSR to a peak of VND 33,450 on May 18.

By May 19, the mechanical buying was complete. No more mandatory ETF purchases. Those who had bought ahead of the rebalancing — from the VND 26,000–27,000 range — were sitting on 25–27% gains. Selling pressure was intense. BSR became the epicenter of the liquidation and pulled the whole sector down with it.

This is why the group's decline on May 19 was so far out of proportion to Brent's move. It wasn't that Brent's 1.58% drop caused a 7% stock decline. Rather: the 22% Brent rally had already been absorbed into stock prices, there was no new upside catalyst, and BSR had lost its index-rebalancing tailwind after May 13. Two independent factors converged in a single session.

The Right Question to Ask

May 19 stress-tested a common flaw in the oil-stock holding thesis: confusing Brent's current price level with a change in expectations. Stocks do not pay for today's Brent; they pay for what the market expects next.

At current valuations — after one-month gains of 6–19% across the group — resuming the uptrend requires at least one of the following: Brent pushing clearly above $110 with fresh momentum; the refining crack spread widening further, supporting BSR independently of Brent direction; a specific and verifiable supply disruption (not vague "ongoing tensions"); or Q2 financial results that beat expectations convincingly enough to re-rate the group's valuation.

Conversely, a scenario where Brent holds at $105–110 for several months — with geopolitical risks maintained but not escalating — is a neutral backdrop at current prices. Not bearish, but without a new catalyst, stocks have no clear path higher.

The takeaway is not to avoid oil and gas stocks. The takeaway is to ask the right question. Instead of asking "Is Brent high?", ask "What expectations are already priced in, and what new catalyst remains to drive prices further?" Q2 earnings from BSR, GAS, and PLX will be among the most important data points this summer. These results will confirm whether crack spreads continue to expand and whether the Brent-to-earnings relationship holds at current price levels.