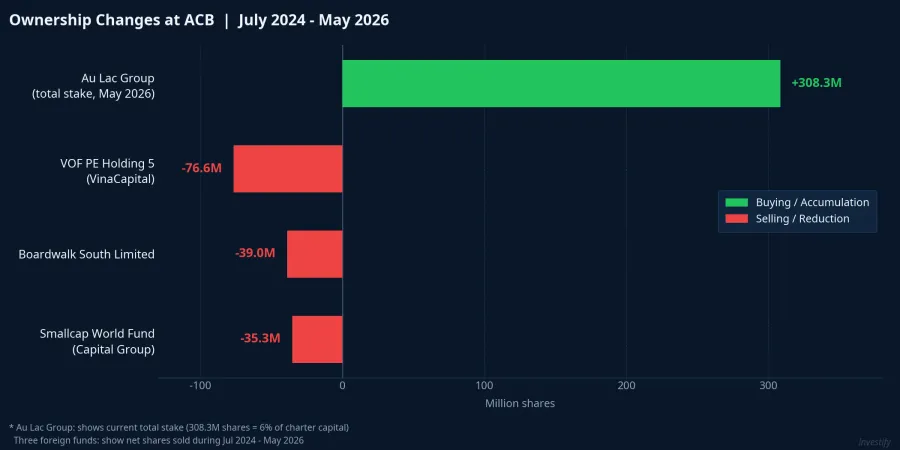

Between mid-2024 and May 2026, ACB's major shareholder register underwent a notable restructuring. Three foreign funds progressively cut their positions at different intensities, while the domestic Au Lac group accumulated 308.3 million shares, equivalent to 6% of the bank's charter capital. On the surface, this looks like two opposing trends. Look one level deeper, and you see not two trends but four completely different investment theses playing out simultaneously.

Four Institutions, Four Different Questions

VOF PE Holding 5: winding down, realizing returns. This fund is part of the VinaCapital group and carries the hallmarks of a fixed-life private equity vehicle. Its decision to exit all 76.6 million shares was not a verdict that "ACB is no longer attractive."Báo Pháp Luật This was the predictable end-of-life action for a fund structure that must return capital to its investors. The question VOF PE 5 was answering was: "Is it time to close the books?" That answer is almost entirely independent of ACB's operating story.

Boardwalk South Limited: portfolio rebalancing, stepping below the 1% disclosure threshold. This fund reduced its stake from over 82 million to 43 million shares, equivalent to 0.839% of voting capital, dropping below the threshold requiring public disclosure. This was a decision to cut more than half the position while retaining the rest. The question Boardwalk was answering was: "Does ACB's weighting in our portfolio still justify its original allocation?" When the answer was "no," they chose to trim rather than exit entirely. That signals a portfolio sizing decision, not a view on underlying asset quality.

Smallcap World Fund: maintaining the long-term thesis, trimming size. The Capital Group fund reduced its holding from 112 million to 76.7 million shares, cutting roughly one-third of the position. Its remaining 1.494% stake still exceeds the 1% major shareholder disclosure threshold. The question it was answering was: "Do we need to exit entirely?" The answer — "not yet" — signals that the long-term thesis remains intact; the fund is simply resizing. This is arguably the most important signal among the three funds: long-duration capital is still holding.

The Au Lac Group: building strategic ownership influence. The shareholder group centered on Ms. Ngo Thu Thuy, Chairwoman of Au Lac JSC, completed its accumulation on May 4, 2026, when Ms. Nguyen Thien Huong Jenny purchased an additional 8.4 million shares, bringing the group's total to 308.3 million shares, or 6% of charter capital.Dan Tri The question the Au Lac group was answering was: "Should we become a strategic shareholder in ACB?" This is an entirely different exercise from the three funds above. The objective is a seat at the table in ACB's medium- to long-term ownership structure, not short-term return optimization.

Reading the Foreign Ownership Picture Correctly

Two statistics tend to get cited together: foreign investors net-sold more than 116 million ACB shares over a recent one-month period,VietnamBiz and the three funds above collectively reduced positions by more than 150 million shares since July 2024.Báo Pháp Luật Collapsing these two numbers into a single "foreign investors are leaving ACB" message misses two important points.

First, the three funds represent three structurally different types of investor: a fixed-life private equity vehicle, a hedge fund rebalancing its book, and a long-only mutual fund. Each has a distinct allocation mandate and divestment cycle. Grouping them under a single "foreign block" label merges three separate stories into one category with no analytical content.

Second, and this is the point most often misread: ACB has spent years in the group of Vietnamese banks with their foreign ownership room fully filled, holding foreign ownership around 27–28% against the 30% legal cap for foreign investors in commercial banks. After the 2024–2026 selling cycle, foreign ownership has fallen to roughly 25.3%, opening up about 4.7% of available room. This is the first time in years ACB has had meaningful unused capacity in its foreign room. The opening of the room is the result of the selling pressure, not the cause — prior to this cycle, new foreign capital that wanted to enter ACB had no room to enter.

Financials and Valuation: The Foundation of Au Lac's Thesis

The next layer to examine is the underlying data that informed the Au Lac group's decision.

ACB reported after-tax profit of VND 4,320 billion in Q1 2026, up 17.5% year-on-year.VnExpress The cost-to-income ratio (CIR) declined to approximately 32%, reflecting improving operational efficiency.Vietstock Outstanding loans reached more than VND 711,000 billion, up 3.2% year-to-date. This is a bank with stable operating performance: not a recovery story from the trough, but a steady, consistent growth trajectory.

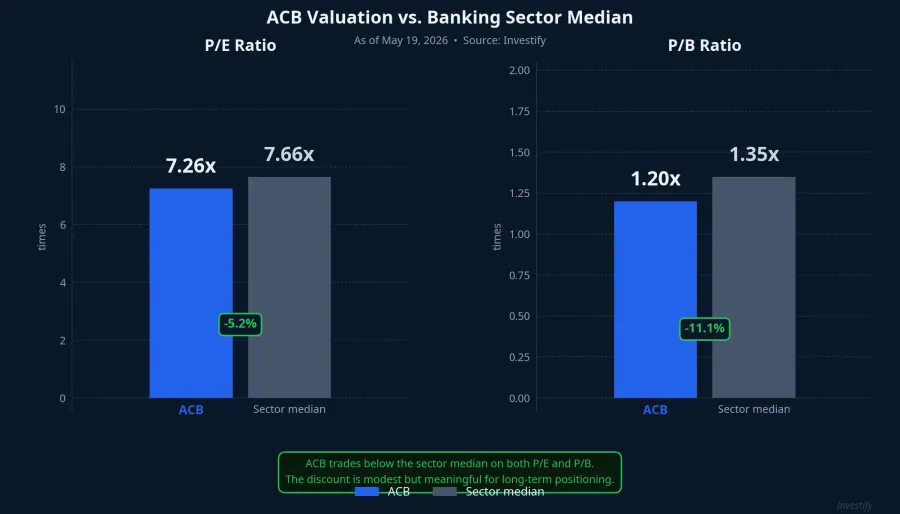

On valuation: ACB closed the morning session on May 19, 2026 at VND 23,000 per share,CafeF implying a market capitalization of approximately VND 118,100 billion. At that price, the stock trades at a P/E of approximately 7.26x and a P/B of approximately 1.20x, a modest discount to the listed banking sector median (P/E 7.66x, P/B 1.35x).

The discount versus peers is not dramatic, but it appears sufficient for the Au Lac group to consider VND 23,000 a reasonable entry point for a strategic 6% position.CafeF The critical point is that Au Lac's thesis is not a bet on this quarter's earnings versus next quarter's. Their thesis is about having a voice in ACB's ownership structure over the medium and long term. A P/B of 1.20x is one supporting data point that the entry price is acceptable. It is not the primary driver of the decision.

Positioning Against Your Own Time Horizon

Retail investors often default to a simple heuristic: "foreign selling is bearish, domestic buying is bullish." The ACB situation shows that both sides of this rule oversimplify the picture. The more useful question to ask is: what problem am I actually trying to solve?

Three common frameworks, each answering a different question:

For investors with a sub-12-month horizon focused on supply pressure in the order book, the signal worth watching is the pace of foreign net selling through May and June 2026. Q2 earnings are not the primary variable in this framework.

For investors with a 2-to-3-year horizon evaluating on valuation, the P/B of 1.20x and P/E of 7.26x are datapoints to benchmark against Q2 financials, due in late July. Key metrics to monitor include: non-performing loan (NPL) ratio, credit growth pace, and whether CIR continues its improvement trajectory.

For investors treating bank equities as part of a long-term asset allocation, the most important development is not this week's price. It is the shift in ownership structure from foreign financial institutions to a new domestic strategic group, a transition that will shape ACB's governance dynamics for years ahead.

Two Signals Worth Watching in the Weeks Ahead

The different theses held by these four institutions are not in conflict in a "right versus wrong" sense. They are answering different questions over different time horizons.

Specific signals worth monitoring over the next 4 to 6 weeks: ACB's Q2 financial report (expected in late July) will confirm whether credit growth and asset quality are sustained after Q1. Equally important is the posture of Smallcap World Fund, the only one of the three foreign funds still holding above the 1% disclosure threshold at 1.494%. If the fund reduces further below that threshold in Q2 2026, that is a clearer signal that long-duration foreign capital is pulling back. If it does not, Smallcap's maintained position remains a meaningful counterpoint when assessing the full picture of ACB's ownership landscape.