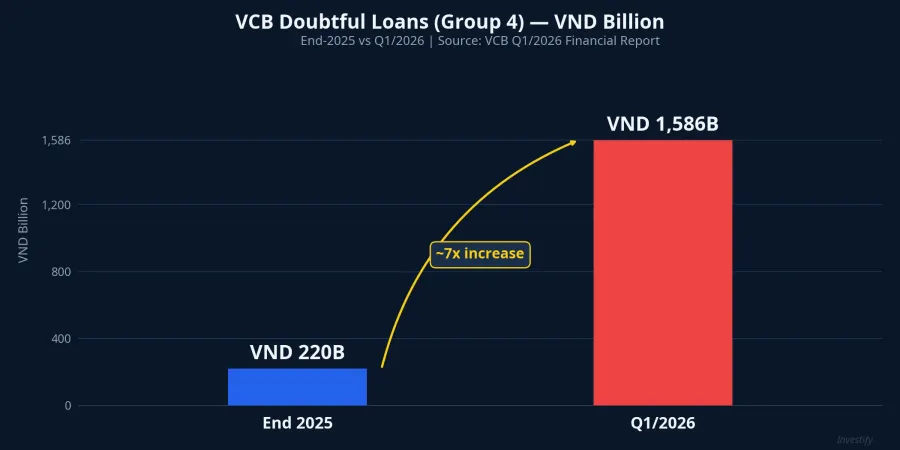

Vietcombank's (VCB) Q1/2026 financial report contains one figure that tends to stop investors cold: doubtful loans (Group 4) surged more than 7-fold in a single quarter, climbing from approximately VND 220 billion to VND 1,586 billion.Vietstock The instinctive read is "VCB's asset quality is deteriorating fast." Yet the bank's overall NPL ratio only edged from 0.58% to 0.62%, still ranking among the lowest in Vietnam's banking system. The apparent contradiction is actually the same story told from two angles: VCB is actively reclassifying its loan portfolio on a more conservative basis, not signaling a book in distress.

The Q1/2026 Numbers in Full

Before drilling into Group 4, the headline results deserve context. Pre-tax profit reached VND 11,803 billion, up 9% year-on-year.Vietstock Net interest income hit VND 17,651 billion, a 29% year-on-year increase. That profit base gives the bank enough room to materially increase provisioning without severely denting bottom-line results.

On asset quality, total NPL rose from VND 9,670 billion at end-2025 to VND 10,868 billion by end of Q1, an increase of over 12%.Người Quan Sát Breaking down that VND 10,868 billion: Group 5 (loss loans) accounts for VND 8,310 billion, or 76% of total NPL; Group 4 (doubtful) accounts for VND 1,586 billion; and the remainder is Group 3 (substandard) at approximately VND 972 billion.

Group 4 Up 7x: How to Read It

The movement across loan groups in Q1 was highly uneven. Group 2 (special mention) rose 49.4%; Group 3 (substandard) rose 27.7%; Group 4 (doubtful) surged more than 7-fold; while Group 5 (loss) actually fell 4.33%, to VND 8,310 billion.Người Quan Sát

Three observations clarify why this picture is not "7x worse."

First, the overall NPL ratio barely moved. The 0.58% to 0.62% tick tells us that total NPL is growing far more slowly than Group 4 alone; most of the movement is inter-group migration, not a wave of performing loans turning sour.

Second, Group 5 declined 4.33%. That is the opposite of what happens when asset quality genuinely deteriorates. If the book were truly under stress, Groups 4 and 5 would both be rising. The Group 5 decline indicates active resolution and recovery of older legacy loans.

Third, provisioning expense rose 3.3-fold. Credit risk provisioning expense reached VND 2,493 billion in Q1, up 3.3x versus the same period last year.Vietstock When provisioning surges yet the loan loss reserve (LLR) ratio stays above 250%, the bank is pre-emptively building buffers, not scrambling to cover losses as they emerge.

VCB vs. Peers: The Gap Remains Wide

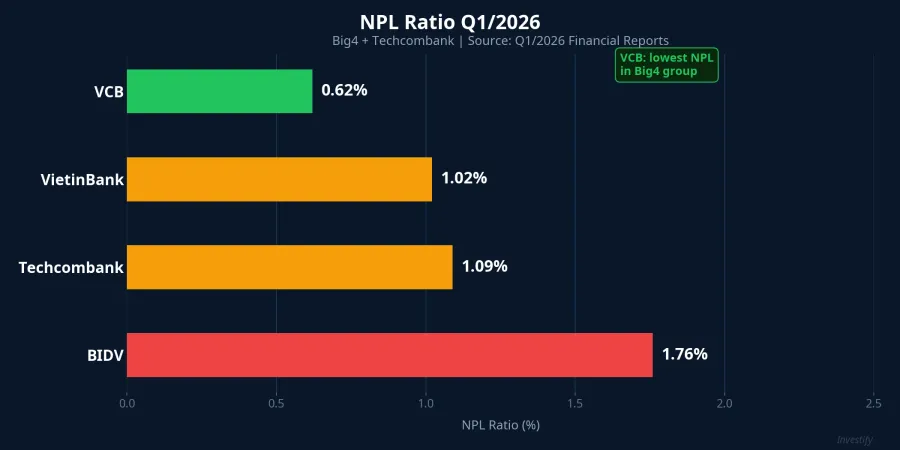

Comparing Q1/2026 data across the major banks shows a clearly diverging picture. VCB holds its NPL at 0.62%, while VietinBank sits at approximately 1.02%, Techcombank at around 1.09%, and BIDV at 1.76%.DNSENgười Quan Sát

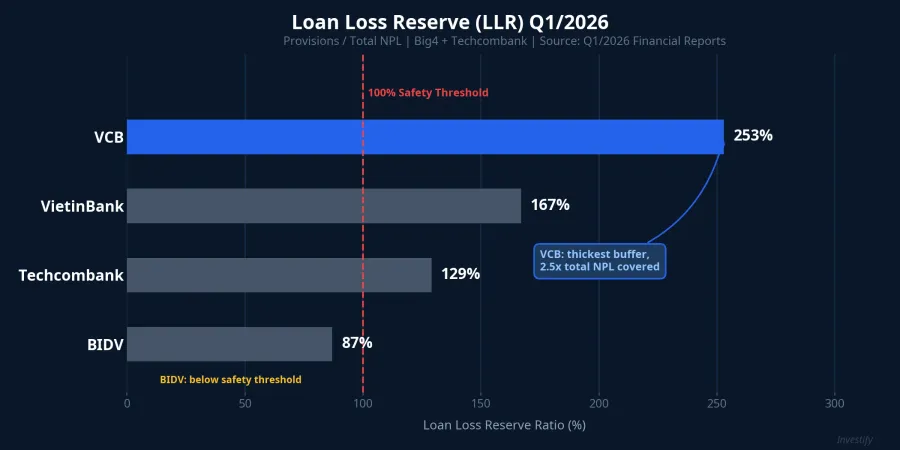

The divergence is even starker on LLR. Across the entire banking sector in Q1/2026, only five banks maintained an LLR above 100%: VCB, VietinBank, Techcombank, ABBank, and ACB. VCB leads at above 250%, nearly double the runner-up. VietinBank stands at approximately 167.2%, Techcombank at around 129.4%, while BIDV trails at 86.9%, below the 100% threshold.

LLR directly measures the capacity to absorb latent losses: for every VND 100 of NPL on the books, VCB has already set aside over VND 250 in provisions. That buffer does not shrink simply because Group 4 moved around within a single quarter.

The Classification Mechanism: Why Group 4 Rising Is Not Necessarily Bad

Circular 11/2021/TT-NHNN divides loans into five groups with escalating provisioning requirements: Group 1 (pass) at 0%, Group 2 (special mention) at 5%, Group 3 (substandard) at 20%, Group 4 (doubtful) at 50%, and Group 5 (loss) at 100%.

When a loan shows early signs of repayment stress, a bank may proactively transfer it into Group 4 as a precaution, even if the borrower has not yet technically defaulted. This is active risk management, not a credit event. A quarter with strong profits is the ideal window to do this, since the additional provisioning cost does not materially impair the income statement.

Two Alternative Explanations

Two alternative readings deserve a fair hearing before committing to a conclusion.

The first is that VCB is deliberately delaying the migration of Group 4 loans into Group 5 to avoid the 100% provisioning hit. This runs into a straightforward contradiction: provisioning expense already jumped 3.3x. A bank trying to defer risk recognition would reduce provisioning, not accelerate it. The actual behavior contradicts the hypothesis.

The second is that one or a handful of large borrowers simultaneously downgraded, pulling the entire Group 4 figure upward. This cannot be fully ruled out from published data alone. However, a VND 1,586 billion Group 4 balance on the books of a bank with a market cap exceeding VND 514,000 billion, combined with an LLR still above 250%, makes severe single-borrower concentration look unlikely. The semi-annual review report will provide the granular data needed to test this cleanly.

Metrics That Actually Matter When Reading a Bank's Balance Sheet

A single loan-group swing in one quarter is a poor proxy for asset quality direction. Investors reading bank financials should prioritize the following metrics instead.

Loan loss reserve (LLR) is the best single measure of loss-absorption capacity. A high LLR means the bank has provisioned adequately and is insulated against short-term noise from individual loan group movements.

Group 2 loans (special mention) deserve more attention right now than Group 4. VCB's Group 2 rose 49.4% in Q1, meaningfully faster than loan book growth. Group 2 is the primary pipeline feeding Groups 3 through 5 in subsequent quarters; sustained rapid growth here is the earliest reliable signal of real asset quality pressure.

Provisioning expense as a share of loan book indicates how proactively a bank is recognizing risk. Voluntary provisioning during a high-profit quarter is good long-run management, even if the quarterly numbers look less attractive on the surface.

Net loan migration captures the underlying trend. Positive migration (loans returning to lower-risk groups) signals resolution; persistent negative migration over multiple quarters is the genuine warning.

Restructured loans kept in original classification are the portion of risk not yet visible on the official NPL line, particularly important following the restructuring period under Circular 02.

Conclusion: Asset Quality Thesis Intact

Taken together, VCB's Q1/2026 data does not tell the story of rapid asset quality deterioration. The bank used a strong-profit quarter to reclassify loans more conservatively, build ahead of potential losses, and continue resolving its legacy Group 5 book. The 7-fold surge in Group 4 is a governance behavior, not a symptom of a collapsing portfolio.

The two pillars of VCB's best-in-class asset quality thesis remain in place: an LLR above 250% and an NPL ratio of 0.62%. On the morning session of May 18, VCB shares traded at VND 61,500, up 1.32%.

The signal worth monitoring is not Group 4 next quarter but the trajectory of Group 2. A 49.4% increase in a single quarter, well ahead of overall loan book growth, is the data point that warrants ongoing scrutiny. If Group 2 continues to accelerate through Q2, that is when genuine asset quality pressure may begin to materialize, and when it would be appropriate to revisit the thesis. One alarming-looking number in isolation is not that moment.