The Quy Xa iron ore deposit in Van Ban, Lao Cai is among the largest iron ore mines in Vietnam, with estimated reserves of approximately 120 million tonnes. For more than 13 years, the Vietnam-China joint venture known as the Vietnam-China Minerals and Metallurgy Company (VTM) extracted less than one-sixth of those reserves, accumulated roughly VND 6,500 billion in debt, and ultimately saw its Chinese partner walk away. On May 18, 2026, CafeF reported that Hoa Phat and Dai Quang Minh had completed the capital structure to take over the entire mining complex through a new legal entity.CafeF

This is more than a financial transaction. It is Hoa Phat's first move up the steel value chain. The company is shifting from total dependence on imported ore toward a domestic source that can serve as a long-term strategic anchor.

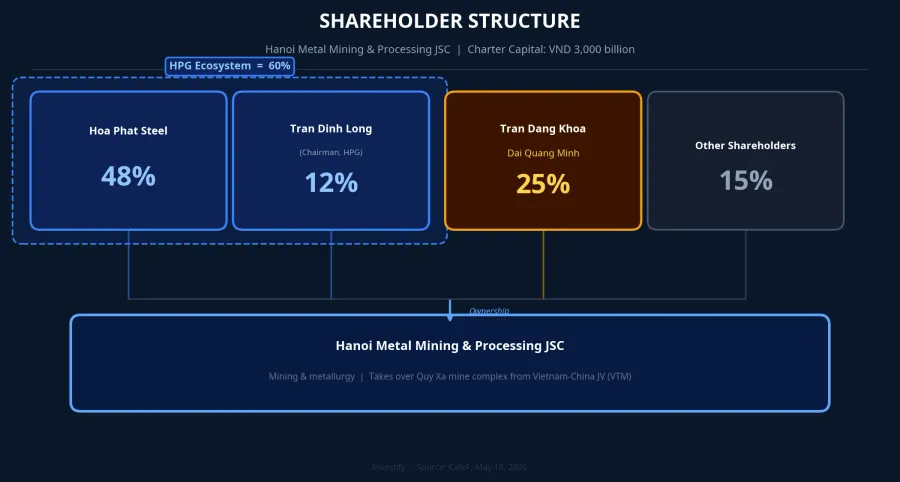

Capital Structure: HPG at 60%, Dai Quang Minh at 25%

The new legal entity is Hanoi Metal Mining and Processing JSC (CTCP Khai thac va Che bien Kim loai Thu Do), whose charter capital was raised from an initial VND 1,200 billion to VND 3,000 billion in just a few months.CafeF In the founding shareholder structure, Hoa Phat Steel JSC holds 48% of charter capital. Mr. Tran Dinh Long, Chairman of Hoa Phat Group JSC (HPG), holds an additional 12% directly. In aggregate, the HPG ecosystem controls 60% of the new company.

On the partner side, Mr. Tran Dang Khoa, Chairman of Dai Quang Minh Real Estate Investment JSC, contributed VND 300 billion representing 25% in the initial funding round before the capital increase.CafeF Dai Quang Minh is a major real estate and infrastructure company within the THACO ecosystem, with charter capital recently raised to nearly USD 1 billion.VietnamBiz This is not the first time HPG and Dai Quang Minh have worked together: the two were co-investors in a consortium for the Red River scenic axis project valued at approximately VND 855,000 billion.Dan Viet

The new company takes over all of VTM's mining complex assets, together with the accumulated debt of approximately VND 6,500 billion that it will need to resolve.

13 Years of Vietnam-China Joint Venture: Only One-Sixth Extracted

By the numbers, this stands as one of the most prolonged failures in the history of mineral joint ventures in Vietnam. VTM received its mining license in 2007 with a shareholder structure comprising VNSTEEL (46.85%), Lao Cai Minerals (8.1%), and China's Kunming Steel (45%). After more than 13 years of operation, the joint venture extracted only approximately 20 million tonnes of ore from the mine, equivalent to one-sixth of total reserves of 120 million tonnes.CafeF

Multiple overlapping causes led to this outcome. An inspection report from 2017 found that the Chinese partner had controlled export coordination and was involved in the irregular sale of nearly 7 million tonnes of ore.Bao Phap Luat Kunming Steel, facing serious financial difficulties at home, progressively reduced its capital contributions and eventually withdrew from the joint venture. On VTM's side, accumulated losses combined with unresolved environmental violations prevented regulators from renewing the mining license.

The deeper problem lay in the business model itself. When global ore prices swung sharply between 2014 and 2020, VTM's dependence on raw ore exports eroded margins. Without a metallurgical partner capable of absorbing domestic production, and with outdated technology driving up extraction costs, VTM spiraled into losses. The VND 6,500 billion debt is the accumulated consequence of a split governance structure where neither party had the full capability to close the value chain from mine to finished product.

Three Benefits HPG Gains from a Domestic Mine

Hoa Phat currently imports iron ore primarily from the Robe River and Pilbara regions of Australia and from Vale in Brazil, arriving by sea before entering the blast furnaces. Once the Quy Xa mine is restarted, HPG stands to gain three things that a maritime supply chain cannot provide.

First, a shorter logistics chain. The route from Quy Xa to Hoa Phat Dung Quat and Hoa Phat Hai Duong runs overland by road and rail, bypassing the sea entirely. During periods of global supply chain stress, dependence on shipping schedules has been a recurring vulnerability for HPG. Second, reduced exposure to USD/VND exchange rate swings: imported ore is priced in USD, while domestic ore is settled in VND. Third, a negotiating counterweight when discussing pricing terms with Vale and Australian suppliers once a domestic alternative exists.

Against a backdrop of iron ore 62% Fe CFR prices ranging between approximately USD 107-111 per tonne in the first weeks of May 2026, near a 15-month high,Thi truong hang hoa some 100 million tonnes of remaining geological reserves at Quy Xa represent a strategic buffer for HPG's margins if global ore prices enter a structurally higher phase.

Three Hurdles Before the Mine Contributes to Output

The picture is not as simple as "owning the mine means having the ore." The 100 million tonnes of unextracted reserves on paper must clear three layers of obstacles before they become commercial production.

The first hurdle is regulatory. The new company must complete the formal closure of the old mine and apply for a fresh mining license under the current Mineral Resources Law, including resolving environmental violations inherited from VTM. The second hurdle is financial: the VND 6,500 billion of inherited debt and outstanding legal obligations require a concrete restructuring plan before the operation can run stably. The third hurdle is infrastructure: VTM's extraction, ore processing, and transport systems have been assessed as outdated and will need complete reinvestment.

On timing, a mine restart in Vietnam typically takes 18-36 months from the point of licensing to commercial-scale production, not counting the inherited legal risks from VTM. That means Quy Xa is unlikely to contribute meaningfully to HPG's margins before 2027-2028. The risk-sharing structure also reflects this caution: HPG does not hold direct majority control (only 48% through Hoa Phat Steel) and has publicly stated a position of waiting for concrete results. Dai Quang Minh brings infrastructure construction capability and project financing; HPG brings metallurgical capacity and a guaranteed off-take for the mine's output. This division of labor is a rational structure for the early stage.

How to Read This News If You Hold HPG

Key figures from HPG's most recent quarterly results are worth noting: in Q1/2026, the company reported revenue of VND 53,300 billion and net profit of VND 9,056 billion, a rise of approximately 170% year on year.Nguoi Quan Sat Market capitalization as of May 15 stood at VND 203,800 billion. These numbers show that HPG has the financial strength to absorb the Quy Xa deal without meaningful near-term cash flow pressure.

Notably, HPG shares closed at VND 26,550 on May 18, down 1.85% from the previous session, coinciding with the day the Quy Xa news was widely reported.Simplize The market's muted reaction accurately reflects the reality: no license yet, no debt resolution plan yet, no infrastructure investment yet.

The right analytical framework is to separate two questions. First, does the long-term investment thesis for HPG change? The answer is no: Quy Xa reinforces HPG's raw material advantage but does not reverse the existing thesis. Second, does the valuation need immediate revision? Also no, because cash flows from the mine will not materialize for at least six to eight quarters.

Three signals worth tracking in the coming quarters: the progress of a new mining license from the Ministry of Natural Resources and Environment; a concrete plan for resolving the VND 6,500 billion of VTM debt; and the scale of capital expenditure for mine infrastructure disclosed in HPG's 2026 annual report. When those three pieces are in place, the market will have a foundation for repricing Quy Xa's contribution to Hoa Phat's value chain.