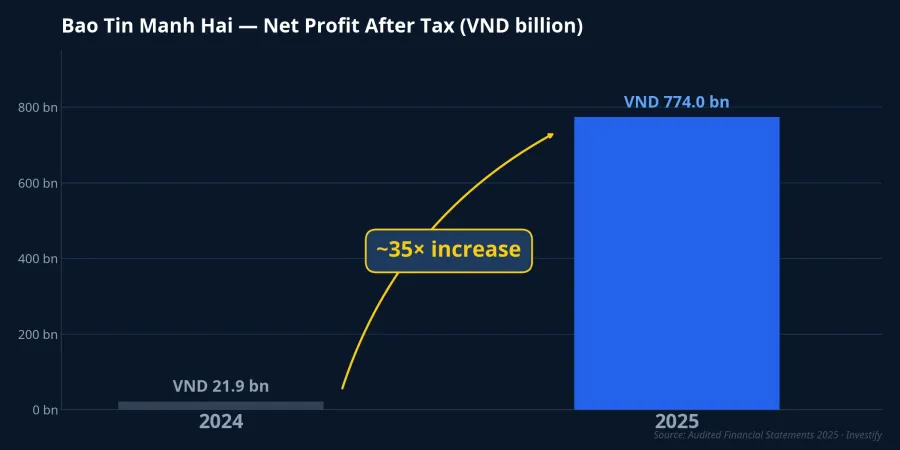

The last time HOSE welcomed a large-scale gold company was 2009, when PNJ listed. Seventeen years later, Bao Tin Manh Hai has announced plans to IPO on the exchange in Q4 2026, with SSI serving as underwriter and at least 15% of shares offered to the public.VietnamBiz Alongside the IPO announcement, the company released its audited 2025 financial statements: net profit after tax came in at VND 774 billion, up nearly 35-fold from VND 21.9 billion in 2024.

That 35x figure grabs immediate attention. But reading this IPO correctly requires working through three layers: what actually drove the profit spike, how the business model differs from PNJ, and an off-balance-sheet variable that could fundamentally reshape the company's valuation.

The Financial Picture: What's Behind the 35x Jump

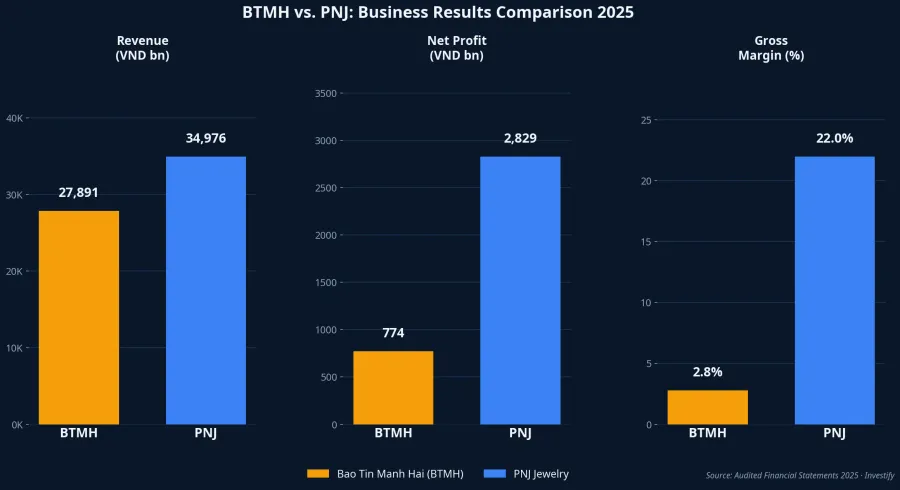

Bao Tin Manh Hai operates across three segments: SJC gold bars, 24K gold rings, and jewelry. The company generated VND 27,891 billion in net revenue in 2025, with the bulk coming from 24K gold rings, a segment characterized by thin margins but high inventory turnover.CafeBiz At year-end 2025, the company operated 12 retail stores, concentrated in Hanoi with a few outposts in Bac Ninh and Hai Duong.

Looking at the numbers, the net profit margin sits at approximately 2.8%, consistent with a business skewed toward commodity gold trading. The VND 27,891 billion in revenue does not automatically translate into large profits: thin margins and high turnover are two sides of the same structural characteristic.

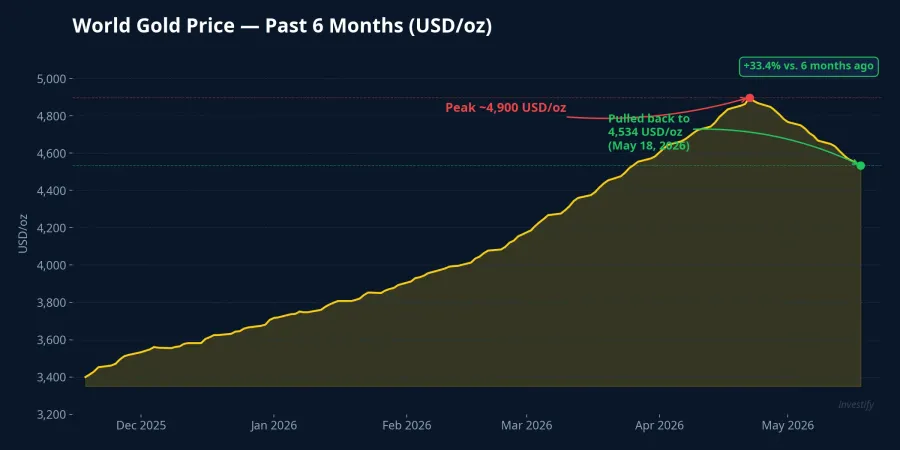

The surge from VND 21.9 billion to VND 774 billion needs to be read against the gold price cycle. 2025 was an exceptional year for gold globally, with prices climbing to a peak of around USD 4,900/oz before pulling back to USD 4,534.30/oz as of May 18, 2026.Kitco Physical gold traders benefit doubly during rallies: buy-sell spreads widen as prices climb, and inventory is marked to market each period. The exceptionally low 2024 base (VND 21.9 billion) makes the growth ratio look even more dramatic than the underlying business momentum suggests.

One figure worth examining closely is management's 2026 target: revenue above VND 74,000 billion (2.65× the 2025 figure) and net profit of VND 1,574 billion (approximately double 2025). The plan rests on opening 68 new stores in a single year, growing from 12 to 80 by end-2026 and targeting 450 stores by 2030. This is an aggressive expansion scenario that depends on both execution speed and the trajectory of global gold prices. If gold trades sideways or corrects further, 2026 profit could fall well short of 2025, since both spread income and inventory revaluation gains would shrink in parallel.

BTMH vs. PNJ: Two Models, Two Valuation Frameworks

PNJ remains the only gold company on HOSE today, making it the natural reference point as BTMH approaches the market. In 2025, PNJ reported revenue of VND 34,976 billion and net profit of VND 2,829 billion, up 33.9% year-on-year, with an average gross margin of 22% for the year.PNJ As of the May 18, 2026 close, PNJ traded at VND 64,700 per share, implying a market capitalization of VND 22,100 billion and a P/E of approximately 13×.

The fundamental difference between the two companies lies in revenue composition. PNJ's core business is 18K–24K jewelry, where value creation comes from design, brand, and a nationwide distribution network. Its 22% gross margin is resilient across gold price cycles because sales do not depend directly on physical gold trading spreads. Bao Tin Manh Hai leans heavily toward 24K gold rings and gold bars, with thinner margins, larger revenue volume, and significantly higher sensitivity to gold price movements.

The valuation implication is direct: applying PNJ's P/E multiple straight to BTMH produces a misleading result. BTMH's earnings swing sharply with the gold price cycle, so a fair valuation must discount for that cyclicality, or use cycle-adjusted metrics rather than peak-year P/E. Applying 13× to the 2025 peak earnings of VND 774 billion implies a market cap of roughly VND 10,000 billion. That figure uses the cycle peak as the denominator, so it risks overvaluation if gold reverses.

Decree 232 and the Variable That Determines Valuation

The hardest valuation question is not in the financial statements. It sits in a regulatory variable outside the balance sheet.

Government Decree 232/2025/ND-CP took effect on October 10, 2025, ending the exclusive gold bar production license that SJC had held since 2012.Banking Journal Since then, qualified enterprises have been able to apply for gold bar production licenses. As of April 14, 2026, the State Bank of Vietnam had received 11 applications from companies and credit institutions, including Bao Tin Manh Hai.Bao Xay Dung

The licensing criteria require a minimum charter capital of VND 1,000 billion. Bao Tin Manh Hai raised its charter capital from VND 300 billion to VND 500 billion during 2025 through a private placement. After the IPO — if priced high enough — the company will clear the regulatory capital threshold. This explains why the IPO and the licensing application are happening simultaneously: they are complementary steps, not coincidence.

Scenario one: BTMH secures a gold bar production license in the second half of 2026. At that point, the company stops being purely a gold retailer and steps into the role of gold bar manufacturer — a position previously held exclusively by SJC. Manufacturing margins are higher than distribution, supply becomes more self-determined, and an entirely new revenue stream opens that the 2025 financials do not yet reflect. The valuation framework needs to be rebuilt from scratch because the profit structure changes qualitatively.

Scenario two: the application is rejected or delayed indefinitely. In that case, the IPO must be valued entirely on the existing distribution business, where earnings absorb the full impact of the gold price cycle. The gap in fair market capitalization between these two scenarios is substantial, and the prospectus has not yet been published to anchor either one.

Three Signals to Watch Before the Prospectus

The right question for investors is not whether to participate in the IPO, but rather what valuation makes sense under each scenario. Three signals matter before the official prospectus is released.

The first is the detailed revenue breakdown. The proportion of SJC gold bars, 24K rings, and jewelry determines how sensitive earnings are to gold price movements. The same VND 774 billion net profit looks very different depending on whether it came primarily from jewelry (more stable) or from gold bar transactions (more cyclical).

The second is the licensing timeline under Decree 232. The State Bank's decision in H2 2026 will fork BTMH's valuation into two structurally different paths. Investors who prefer waiting for that signal before committing significant capital have a rational basis for doing so at this stage.

The third is governance quality and ownership structure post-IPO. Family-owned businesses transitioning to the public market typically go through a governance adjustment period, particularly in a tightly regulated sector like gold. The prospectus will reveal the actual degree of management professionalization and internal control mechanisms.

As the first gold company expected to list on HOSE in 17 years, Bao Tin Manh Hai is worth watching closely. The 35x figure earns that attention. The investor roadshow starting in June and the official prospectus are the two milestones that will provide a genuine basis for valuation, one that moves beyond the headline ratio to the underlying question of what this company actually becomes.