SpaceX is expected to price its IPO on June 11 and begin trading on the Nasdaq under the ticker SPCX on June 12, targeting a valuation of approximately $1.75 trillion and raising roughly $75 billion.Fortune That $75 billion figure is more than 2.5 times the size of the Saudi Aramco offering in 2019, the previous record holder, which raised $29 billion. The underwriting syndicate includes JPMorgan, Goldman Sachs, Morgan Stanley, Bank of America, and Citi, with the roadshow expected to kick off in early June. For investors in Vietnam, there is no direct way to buy SPCX through a domestic brokerage on opening day. There are, however, three access paths, each with different implications for timing, fees, and regulatory complexity.

Most of the $1.75 Trillion Valuation Is Not About Rockets

When most people think of SpaceX, they picture a Falcon 9 sticking its landing or Starship roaring toward orbit. Here is the simpler way to think about the valuation: the bulk of that $1.75 trillion figure does not come from launch services at all. It comes from Starlink, the satellite broadband network that charges monthly subscription fees to customers worldwide.

Think of Starlink as a global internet provider that reaches places no fiber cable or cell tower can: open ocean, rural Africa, mountainous South America, cargo ships, commercial aircraft. That creates a predictable, recurring revenue stream that large institutional investors prize far more than lumpy, contract-by-contract launch revenue. This framing explains why SpaceX commands a valuation several times higher than any pure-play aerospace company.

Starlink: Revenue Nearly Tripled in Two Years, Margins Closer to Software Than Telecom

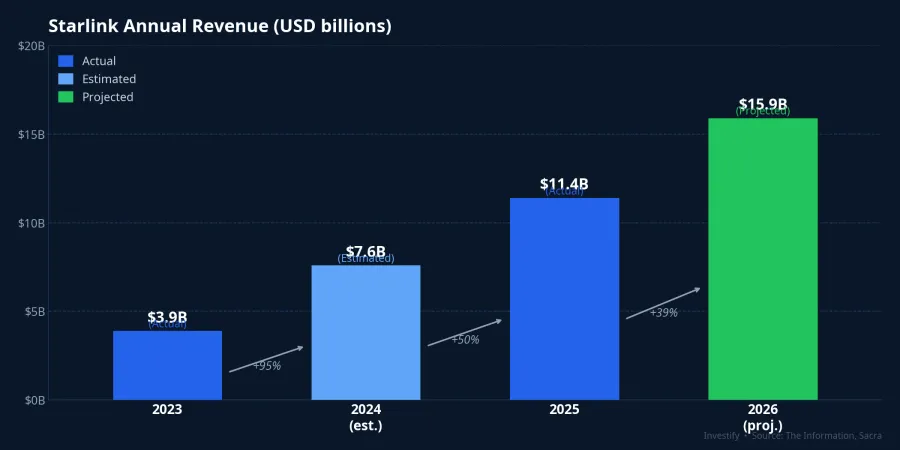

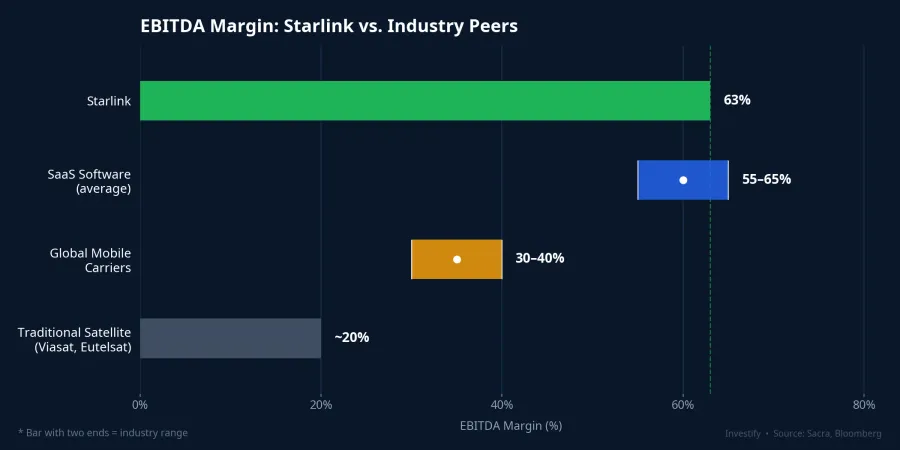

Starlink's revenue reached $11.4 billion in 2025, up 50% from 2024 and nearly triple the $3.9 billion recorded in 2023.TradingKey EBITDA came in at $7.2 billion, implying an adjusted EBITDA margin of approximately 63%. Projections for 2026 point to $15.9 billion in revenue and nearly $11 billion in EBITDA, though these are estimates that SpaceX has not officially confirmed.

That 63% margin is worth pausing on. Global mobile carriers like AT&T and Verizon typically operate at EBITDA margins of 30-40%; traditional satellite operators such as Viasat and Eutelsat run closer to 20%. Starlink's margins look more like a software-as-a-service business than a telecommunications company. The intuition behind this: once the satellite constellation is deployed, the incremental cost of adding each new subscriber is far lower than building another cell tower.

One counter-data point deserves an honest mention. Average revenue per user (ARPU) fell approximately 18% to around $81 per month between 2023 and 2025, even as the subscriber base quadrupled.bwtechzone This is a deliberate strategy: cut prices in emerging markets to grow total subscribers, trading per-user revenue for global scale. By February 2026, Starlink had surpassed 10 million active customers across 160 countries and territories. The model holds up only if the cost of manufacturing and launching satellites continues to fall as Starship matures into commercial operations.

Why BlackRock Is Weighing a $5-10 Billion Bet on Starlink

According to The Information, BlackRock has discussed investing between $5 billion and $10 billion in the SpaceX IPO, drawing from its $536 billion pool of actively managed funds.SeekingAlpha Neither BlackRock nor SpaceX has publicly confirmed this, and the final figure could shift based on how the IPO is priced. Even at the top of the reported range, a $10 billion commitment represents less than 2% of BlackRock's active book — a meaningful position, not a full conviction bet.

The institutional logic here is not about the space race narrative. Firms like BlackRock are drawn to Starlink as recurring-fee infrastructure serving markets where no real competition exists. That said, real risks deserve acknowledgment. Amazon's Project Kuiper is preparing a commercial launch at scale and could compress pricing in markets with existing connectivity infrastructure. If Starship continues to miss its launch schedule, the satellite production cost curve does not fall as projected, and margins follow. These are genuine variables, not hypothetical edge cases.

Three Access Paths for Vietnamese Investors

Path one: ETFs tracking the Nasdaq-100 or S&P 500. No ETF listed on Vietnam's HOSE currently tracks a U.S. equity index. Investors interested in this route need to open an account with an international brokerage to buy funds such as QQQ (Nasdaq-100) or VOO (S&P 500), gaining indirect exposure to SpaceX once it joins the index.TradingKey One development worth noting: Nasdaq implemented a new Fast Entry rule in May 2026 that allows a newly listed company to join the Nasdaq-100 in under a month if its market capitalization ranks in the top 40 of the current index. At a valuation of approximately $1.75 trillion, SpaceX is likely to qualify, potentially shortening the wait significantly compared to the old timeline of several months to over a year. This path carries the lowest legal risk but offers only indirect SpaceX exposure, with a small initial weight in the index.

Path two: Vietnamese mutual funds with foreign investment provisions. Some flexible open-end funds operating in Vietnam have clauses permitting a portion of assets to be allocated to foreign ETFs or fund certificates, but the allocation is at the fund manager's discretion and is typically small. Management fees generally run 1-2% per year, minimum investment amounts start from around VND 1 million depending on the fund, and transactions settle at net asset value (NAV) on a T+1 to T+2 cycle. Choosing this path means delegating the allocation decision entirely to the fund manager. SPCX exposure within any specific Vietnamese fund's portfolio may be minimal or absent depending on the fund's strategy.

Path three: Open an account directly with a U.S. brokerage. Interactive Brokers, Charles Schwab, and TD Ameritrade all accept customers holding a Vietnamese passport. This is the only path that allows buying SPCX on the June 12 opening session. Account opening typically takes 2-5 business days, and funding is done via international wire transfer from a Vietnamese bank. Three points require careful attention upfront: completing the U.S. tax declaration form (W-8BEN); the fact that transferring foreign currency abroad for individual securities investing does not yet have a complete legal framework in Vietnam; and the currency risk from VND/USD conversion when repatriating funds.

What to Watch After the Opening Bell

The approximately $1.75 trillion valuation rests almost entirely on Starlink sustaining its roughly 63% EBITDA margin while continuing to expand. The two most important signals to track in the first three to six months after listing are Starlink's revenue and EBITDA in the first post-IPO quarterly report, and Starship's commercial testing progress. If Starship hits its launch schedule and per-satellite manufacturing costs fall as projected, the thesis supporting the valuation gains evidence. If ARPU continues declining faster than subscribers are added, margins will compress.

For investors just starting to explore this topic, the practical question is not whether SpaceX is a compelling story. The valuation makes it plain that many institutional investors already think so. The real question is which of the three paths fits your own appetite for regulatory complexity and the kind of exposure you want. Path one through ETFs carries the lowest friction and legal risk, with the trade-off of indirect, time-delayed exposure. Path three lets you buy SPCX directly on day one, but requires navigating international account opening and accepting currency risk. The first quarterly earnings report after listing will be the earliest real test of whether today's expectations hold.