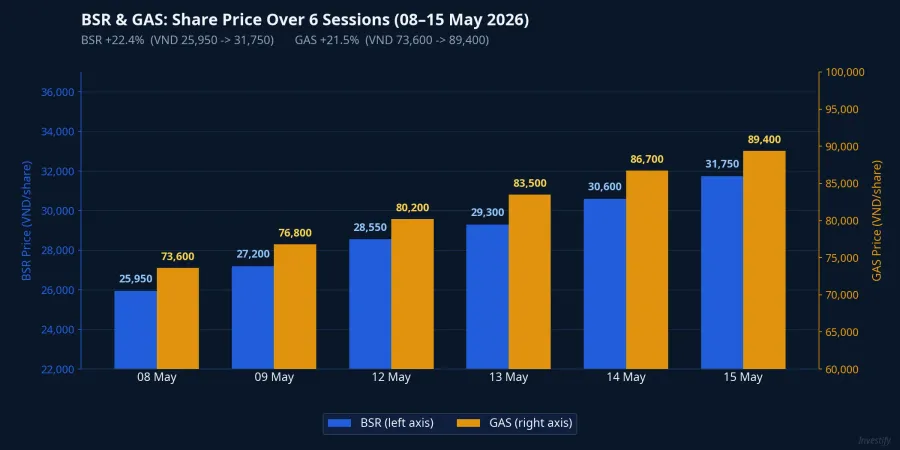

Brent closed the week at USD 108 per barrel. BSR joined the VN30. Oil and gas stocks surged in the week of May 8–15: BSR climbed 22% (from VND 25,950 to VND 31,750 per share), while GAS jumped 21% (from VND 73,600 to VND 89,400 per share). The instinct to buy this sector when oil rises is widespread. The logic seems clean: higher crude prices mean higher profits for oil companies.

That logic holds, but only partially. The part that actually determines who benefits and who bears the risk lies in supply chain structure. Vietnam's two largest refineries have completely different designs and sourcing networks, and the real risk in this crisis is sitting inside the facility whose shares cannot be bought on any exchange.

Two Refineries, Two Completely Different Supply Structures

BSR operates the Dung Quat Refinery with a flexible design capable of processing a wide range of crude grades. In 2026, BSR is permitted to retain all domestically extracted crude oil, covering approximately 90% of its design capacity.Thanh Nien The remainder comes primarily from the United States, West Africa, and the Mediterranean, with no supply routed through the Strait of Hormuz.

This was not luck. BSR's management proactively locked in long-term contracts as tensions in the Middle East escalated. For the March–May 2026 period alone, BSR contracted approximately 3 million barrels of imported crude, including Qua Iboe, Bu Attifel, Medanito, and Palanca Blend, all light sweet grades sourced from the US and West Africa.CafeF In June, BSR approved a further contract to charter a vessel carrying 650,000 barrels of Palanca Blend, valued at over VND 210 billion.Doanh Nghiep & Hoi Nhap When Hormuz tightened, BSR's feedstock pipeline kept flowing.

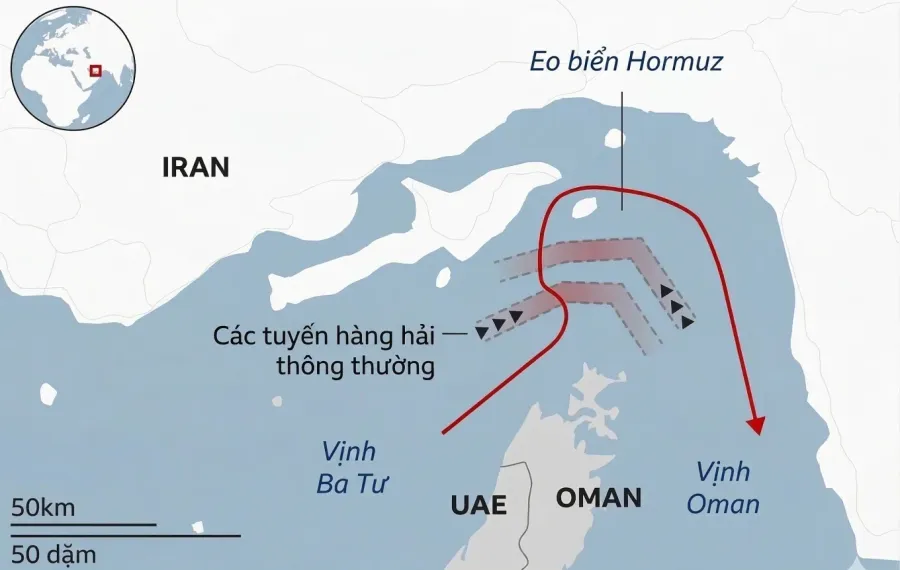

Nghi Son is the opposite story. The refinery supplies approximately 40% of Vietnam's domestic fuel demandVietnamNet, with a design capacity of 200,000 barrels per day, optimized for Kuwaiti crude. Supply comes via long-term contracts with Kuwait, and tanker routes pass directly through the Strait of Hormuz. This is a structural vulnerability, not an operational failure. Reconfiguring refinery processing to handle a different crude grade requires engineering trials and extended timelines, and cannot be done in a matter of weeks. Kuwait accounted for approximately 81% of Vietnam's total crude imports in the eleven months of 2025ZNews, with the bulk of that volume flowing into Nghi Son.

Nghi Son's Workarounds: Higher Costs, Hidden Risk

To protect production, Petrovietnam and Nghi Son deployed multiple measures simultaneously. The CEO of Nghi Son Refinery and Petrochemical is studying a plan to use Vietnamese-flagged vessels in coordination with PVTrans to receive crude directly at Kuwaiti ports.VietnamBiz Japan's Idemitsu Kosan, a major shareholder in Nghi Son, arranged nearly 4 million barrels of crude via an alternative route bypassing Hormuz.The Saigon Times Earlier in 2026, Nghi Son also successfully trialed approximately 1 million barrels of UAE Das Blend, opening another avenue for feedstock diversification.

These measures have kept the refinery running through the end of May 2026 per official communications, but all of them are contingency solutions. Each alternative route carries higher logistics costs than the standard Hormuz passage, which compresses margins even when the plant continues operating at capacity.

The core problem for retail investors is this: Nghi Son is not listed on any stock exchange. The largest structural risk in Vietnam's refining supply chain sits entirely outside the capital market's reach. There are no shares to sell when risk rises, and no quarterly financial reports to track actual costs. BSR and GAS surged last week largely because capital was searching for listed "sector proxies," even though the two tickers' actual exposure to Hormuz risk has been fundamentally different from Nghi Son's since the start of the year.

The Real Mark of the Shock: Diesel Prices Haven't Returned to Base

The cost transmission is most visible in diesel pricing. From VND 19,570 per litre at the end of February, Vietnam's diesel V price surged to a peak of VND 44,980 per litre on April 3, rising over 130% in roughly five weeks as markets panicked over Hormuz. The price then fell sharply by 22% in a single session on April 9, before an official downward adjustment of 9.88% on April 21. As of May 14, the price stood at VND 28,480 per litre: 37% below the peak, but still 56% above the VND 18,200 per litre level recorded on January 22.

In other words, the worst of the spike has passed, but prices have only retreated to early March levels, not to the pre-shock baseline. Q2 2026 is the quarter bearing the heaviest burden: April averaged approximately VND 33,000–35,000 per litre, May around VND 28,000–29,000 per litre. Both months fall squarely within the reporting period.

The sector absorbing the most direct pressure is road freight and domestic coastal shipping, where fuel costs constitute a large share of cost of goods sold. Fuel surcharges typically lag input price moves by a quarter, meaning transport companies absorbed the full burden of April and May's elevated prices before they could pass costs on to customers. Seafood exporters such as MPC and VHC face an additional layer: domestic refrigerated trucks, refrigerated containers to port, and maritime fuel surcharges all increased simultaneously within the same quarter. Textile manufacturers are under moderate pressure overall, since logistics is a smaller share of their cost base, but companies with high export exposure will be more sensitive to surcharge volatility.

How to Read the Q2 Reports

The Q2 2026 earnings season is where these supply chain narratives will crystallize into actual numbers.

For BSR, the lines worth monitoring are feedstock costs and the gross refining margin. Did the supply diversification strategy actually protect margins, or is BSR still squeezed by Brent prices pulling global feedstock costs higher across the board? High oil prices are simultaneously favorable for refined product prices and unfavorable for raw material costs. The reported gross margin will answer this question.

For transport and seafood companies, the lines worth monitoring are the ratio of cost of goods sold to revenue, and the degree to which costs have been passed through to customers. Companies with flexible fuel surcharge mechanisms, those that adjust pricing over short cycles, will be under less pressure than those locked into long-term fixed-price contracts.

What the daily price board does not show: the real risk from this Hormuz crisis does not sit with BSR or GAS. It sits with Nghi Son, a refinery the market cannot price because it has no listed shares, and with diesel costs that have already been absorbed into the cost structure of dozens of downstream industries throughout Q2. None of that is visible from a share price chart.

The signals worth watching over the next two weeks: whether Nghi Son's June production volumes can be secured, and the logistics contract disclosures appearing in the quarterly reports of transport operators.