The "avoid all real estate bonds" rule was born after the Vạn Thịnh Phát and An Đông scandals in late 2022, and it was the right call at the time. When the market froze and issuers defaulted in waves, that reflexive avoidance shielded many retail investors from serious losses. But by April 2026, that same filter is misreading the market in both directions: it ignores meaningful risk differentiation between issuers on the same monthly table, and it fails to identify where the actual risks are hiding.

April 2026: Real Estate Posts Its Biggest Monthly Issuance in Six Months

According to HNX data compiled by Dân Việt, the real estate sector issued VND 30,400 billion in private placement bonds in April 2026, capturing 58.7% of total private placement issuance for the entire market (VND 51,700 billion) and marking the highest monthly figure in the past six months.Dan Viet Compared to the same period last year, the figure rose 110.8%. This is not a modest recovery signal. Corporate capital is flowing back into the bond market at a meaningful pace.

The right question is not whether the real estate sector is recovering. It is: what does the credit quality behind that VND 30,400 billion look like, and where does the retail investor stand in this picture?

A 7-Percentage-Point Gap Within the Same Ecosystem

What the headline number does not reveal: in April 2026's issuance table, two entities from the same corporate group paid coupon rates 7 percentage points apart.

Vingroup (the parent) issued VND 9,200 billion at a fixed rate of 5.5% per year on a 60-month tenor.Viet Bao Vinhomes (the operating subsidiary directly exposed to sales cycles) issued VND 6,000 billion at a maximum rate of 12.5% per year for the first two periods, then floating but with a 12.5% floor.Dan Viet Minh An Real Estate Investment and Development JSC issued VND 7,500 billion at 10% to 10.5% per year on 12- to 30-month tenors, sitting between the two extremes.

That 7-point spread is not arbitrary. The market is pricing three very different things: tenor length (60 months versus 30 months), cash-flow risk structure (strategic holding company versus operating subsidiary bearing direct project sales and legal risk), and collateral quality. The real risk is exactly here: a familiar name within a large group does not automatically carry the same safety profile. Both the "trust the group brand" filter and the "avoid all real estate" filter miss this gap entirely.

In the same month, Vingroup also issued USD 350 million in international bonds with an option to receive Vinpearl shares, listed on the Vienna Stock Exchange and directed at foreign institutional investors.CafeF That tranche does not figure into the VND 30,400 billion domestic total, but it illustrates how large real estate groups are tapping every available capital channel.

The Buyers of VND 30,400 Billion Are Not Retail Investors

This is where the most important misunderstanding lies. The implication is not "real estate has recovered, so retail investors can now buy real estate bonds." The more accurate framing is: most of that VND 30,400 billion flowed to banks, insurance companies, bond funds, and a narrow cohort of high-net-worth individuals who qualify as professional securities investors.

From Decree 65/2022 through the amended Securities Law 56/2024 and Decree 245/2025, the requirements for purchasing privately placed corporate bonds have tightened continuously. An individual must hold a listed securities portfolio of at least VND 2 billion for 180 consecutive days, obtain periodic certification from a licensed securities company, and renew that certification every three months. During its first year after issuance, a private placement bond may only be transferred to fewer than 100 non-professional investors. In practice, this channel is effectively closed to ordinary retail investors.

For retail investors who do not meet the professional threshold, the practical access point is an open-end bond fund. These funds conduct due diligence on individual tranches, maintain diversified portfolios, and allow redemptions on a T+3 to T+5 cycle. Their yields are typically lower than the nominal coupon on any single issuance because of management fees and liquidity reserves, but the trade-off is insulation from a single issuer's payment delay dragging down the entire holding.

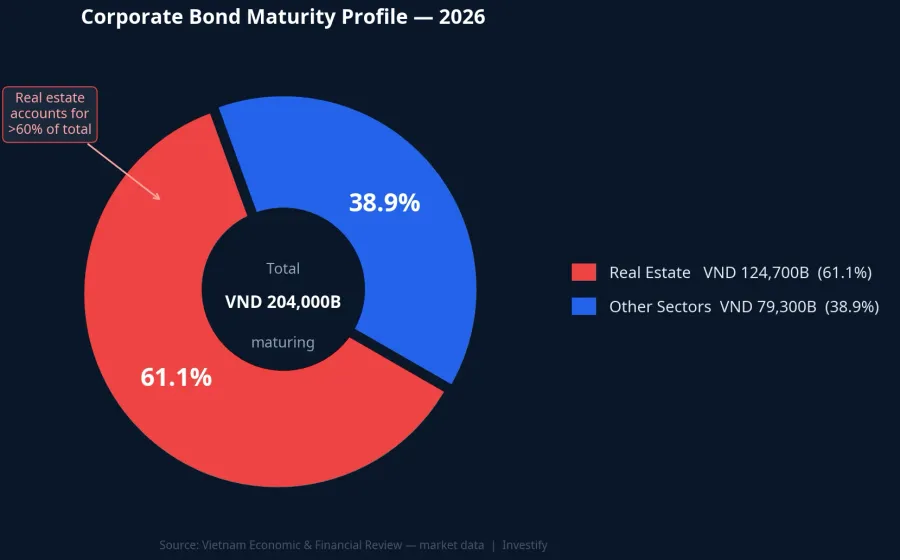

The Maturity Wall Has Not Yet Been Cleared

Most of the real estate recovery narrative is focused on the positive side of the ledger. What is less often stated is that maturity pressure in the second half of 2026 has not yet peaked.

According to Vietnam Economic and Financial Review, approximately VND 204,000 billion in corporate bonds mature across the full year 2026, with real estate accounting for roughly VND 124,700 billion, or more than 60% of the total.Tap chi Kinh te Tai chinh The majority of that burden falls in the second half. Already in Q1 2026, approximately VND 3,732 billion in principal and interest was recorded as late, up from the prior quarter.

What do these two numbers tell us? Issuers with clean project permits, clear land banks, and low leverage are rolling over maturities at 5.5% to 10%. Issuers with high leverage, pending legal approvals, and sluggish pre-sales must accept coupon rates of 12% or above, or negotiate extensions under the mechanism established by Decree 08/2023, which allows a maximum two-year deferral and permits repayment in assets other than cash if bondholders consent. A 12.5% coupon against the Big 4 banks' current 12-month deposit rate of approximately 5.9% per year at the counter sounds compelling on paper.CafeF But that spread is exactly what the market charges for restructuring risk, extension risk, and partial principal loss risk in adverse scenarios.

Three Screening Layers for H2 2026

For retail investors considering corporate real estate bonds as an asset class, three default screening layers need to be applied before any decision.

Layer one: Confirm access eligibility. For anyone who does not meet the professional securities investor threshold, an open-end bond fund is the only legally viable and practically realistic channel for accessing yields above deposit rates without self-assessing individual tranches. Purchasing privately placed bonds directly when lacking the legal qualification is a regulatory violation, not merely a financial risk.

Layer two: Read yield as a risk signal, not an opportunity signal. In a single month, an issuer pricing at 5.5% and an issuer pricing at 12.5% are not offering two versions of the same investment. The yield spread reflects what professional institutions are charging because they have assessed the credit, tenor, and project legal risk. Retail investors rarely have an information edge over that institutional assessment. High coupons carry commensurate risk. There is no free lunch.

Layer three: Track H2 2026 maturity pressure. The approximately VND 124,700 billion in real estate bonds maturing in 2026 represents systemic risk at the sector level, not just individual issuer risk. For investors accessing the sector through open-end bond funds, prioritize funds with clearly disclosed portfolio composition, reasonable diversification, and limited concentration in unusually high-coupon issuers.

The 2022 filter emerged for valid reasons: a frozen market, loose governance, and opaque data. The 2026 filter needs to be more nuanced because the regulatory framework has been standardized, the buyer base has been professionalized, yet the maturity peak for the second half of the year is still ahead. The meaningful question to track through Q3 and Q4 2026 is: how much of those VND 124,700 billion gets resolved cleanly, how much gets extended, and whether that pressure creates a second wave of delayed payments. That is the genuine signal for reading market health, not the headline issuance total.