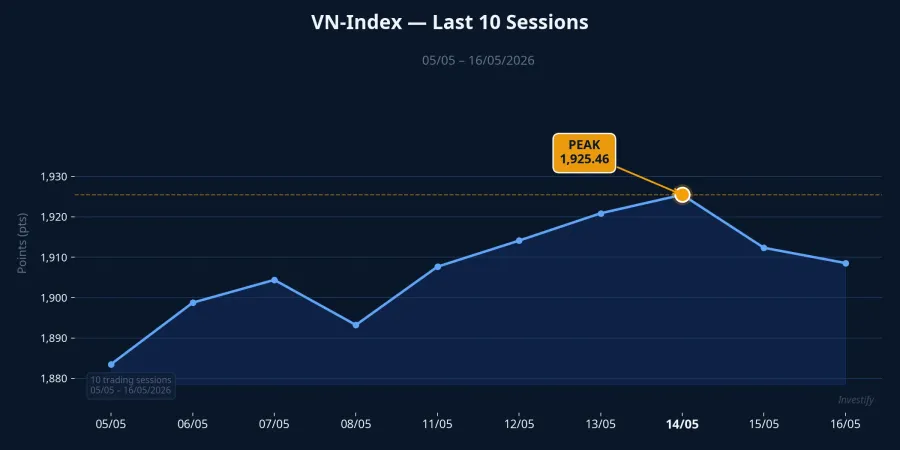

Two markets, two directions, one trading week. On May 14, VN-Index closed at 1,925.46 on the HOSE exchange, a new all-time high. Less than a day later (US time), April CPI data showed US inflation at 3.8% year-on-year, the highest since May 2023 and above analyst forecasts of 3.7%.CNBC Wall Street's reaction was swift: the Dow Jones fell 537 points (1.07%) and the S&P 500 dropped 1.24%.

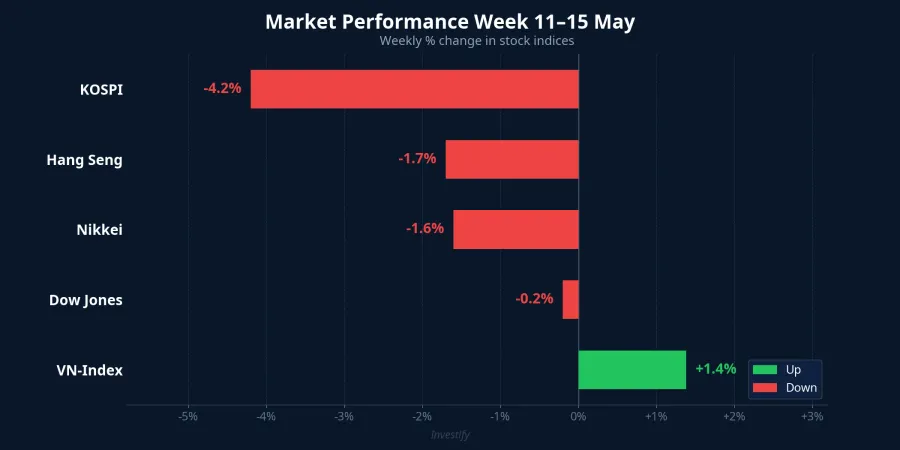

The bigger picture this week is not a simple question of winners and losers. It is a deeper question: what structural factors allowed Vietnam's market to decouple from global pressure, and how long can that decoupling last?

Early Week: Domestic Capital Holds the Line

The week opened in the red on May 11. VN-Index pulled back to 1,895.50, as foreign investors net sold over VND 1,000 billion, extending a withdrawal trend that began in April. This was not a new development: ETFs tracking the VN30 basket, including Fubon FTSE Vietnam, have maintained consistent net selling for several consecutive weeks, reflecting portfolio reallocation strategies by foreign investors amid persistently high US rates.

The turning point came on May 12. VN-Index recovered to 1,901.10, with market-wide liquidity holding in the VND 12,000–19,000 billion range every session for the remainder of the week. The key detail: most of that liquidity came from domestic participants, not foreign flows. This is the first structural distinction worth noting: Vietnam's market this week was supported by domestic capital, not driven by foreign inflows.

Mid-Week: A New Record While Asia Sells Off

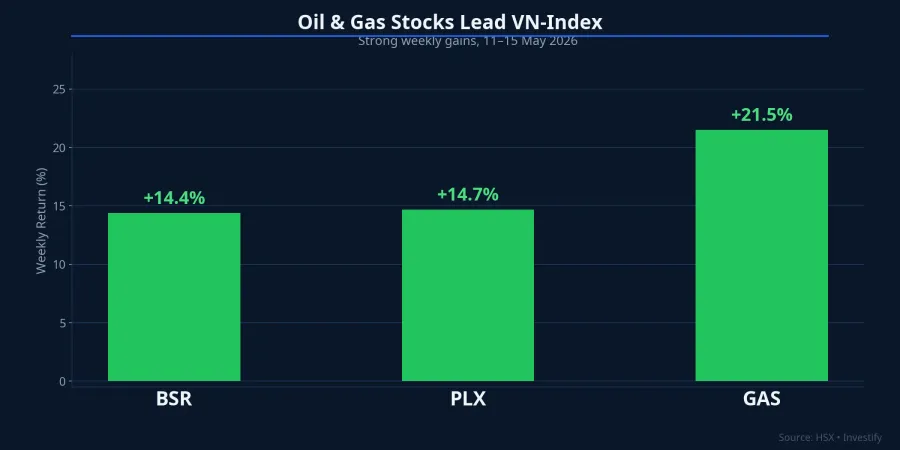

May 14 was the week's high point. VN-Index closed at 1,925.46, clearing the 1,915 level set on May 8 and establishing a new all-time record. The driving force was the oil and gas sector: BSR gained 14.4%, GAS surged 21.5%, and PLX rose 14.7% for the week. Brent crude climbed 6.6% over the same period, reaching approximately $108 per barrel, providing a direct revenue tailwind for these companies.

Across Asia, the picture was starkly different. Korea's KOSPI fell 4.2% for the week, Japan's Nikkei dropped 1.6%, and Hong Kong's Hang Seng shed 1.7%. The divergence comes down to sector composition: KOSPI is heavily weighted toward semiconductors, with Samsung Electronics and SK Hynix together accounting for a large share of the index. When profit-taking hit the chip sector after a strong run-up, KOSPI bore the full impact. VN-Index carries no such concentration. Vietnam's index is more diversified, with energy and utilities occupying meaningful weight, precisely the sectors that benefit when oil prices rise.

Also on the night of May 13 (US time), the US Senate confirmed Kevin Warsh as Chairman of the Federal Reserve. Markets initially absorbed the news slowly; the full policy implications only became clear by the end of the week.CNBC

End of Week: Global Cost of Capital Shifts

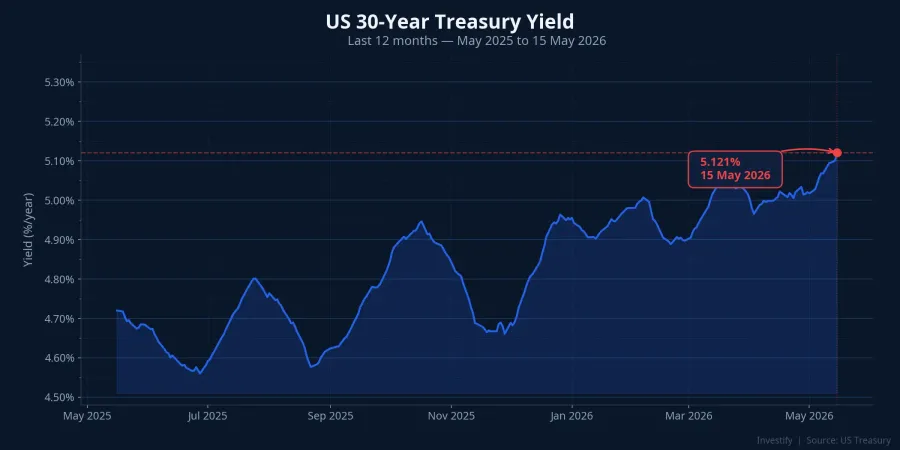

On the morning of May 15 (US time), April CPI came in at 3.8% year-on-year, the second consecutive month of US inflation rising rather than falling, and above the 3.7% consensus forecast.CNBC This was the most significant shift in rate expectations in many weeks.

The reaction spread quickly into bond markets. The US 10-year Treasury yield climbed to 4.59%, while the 30-year yield hit 5.121%, a level not seen since May 2025.CNBC The transmission mechanism to equities is direct: as long-duration yields rise, future corporate cash flows are discounted more heavily, and growth stock valuations must compress. US technology stocks felt the pressure immediately that session.

Back in Vietnam, VN-Index on May 15 traded above 1,920 intraday before a wave of late-session profit-taking, closing at 1,921.60, down 3.86 points from the previous day's all-time high. The pressure was not coincidental: Wall Street headlines and rising US yields affected domestic investor sentiment before the local close.

Why Vietnam Decoupled, and Where the Limits Are

The gap between VN-Index and most of Asia this week has three clear structural explanations.

First, domestic capital dominance. Retail investors, proprietary trading desks, and domestic mutual funds now account for the bulk of Vietnam's market liquidity. When US rates shift, the impact on this group flows primarily through psychology and the exchange rate, not through the direct redemption pressure that hits foreign ETFs.

Second, sector composition protects the index. Energy and utility stocks benefit from higher oil prices, moving in the opposite direction to the pressure that the same inflationary cycle puts on technology. While KOSPI dropped 4.2% on semiconductor weakness, VN-Index had BSR and GAS leading the rally.

Third, the FTSE upgrade narrative due in September 2026 remains a medium-term anchor for market valuations. Circular 08, which took effect on May 15, is expected to ease the loan-to-deposit ratio constraint for major banks, though the near-term impact on bank stock prices was not yet visible: BID, CTG, and VCB all closed in the red on May 15.

These three factors, however, are not permanent. If US Treasury yields remain above 5% for an extended period, the USD/VND exchange rate will face sustained pressure, and foreign investors are likely to continue net selling. At some point, domestic liquidity can stabilize the index but cannot push valuations meaningfully higher. VN-Index may then enter a phase of range-bound trading between 1,900–1,950 rather than continuing to break records.

Week of May 18–22: What to Watch

Next week's macro calendar is light in volume but heavy in significance. On the US side, the April FOMC minutes will be released, and more importantly, Kevin Warsh, Chairman of the Federal Reserve, will make his first public statement as head of the institution. This will be the clearest policy signal since the 3.8% CPI reading shifted market expectations. Any language on the rate path will be parsed carefully.

Domestically, two notable insider transactions: ABB has registered to sell 300,000 shares on May 18, and CMG has registered to sell 100,000 shares on May 19. These transactions are unlikely to move the index materially, but they offer a signal about internal corporate sentiment at current price levels.

Three concrete indicators to monitor. First, whether market-wide liquidity holds above VND 18,000 billion per session. Second, whether oil and gas stocks sustain their momentum after a strong week of gains. Third, whether foreign investors begin shifting from net selling to light buying as valuations adjust.

This week's picture confirms that Vietnam's market is operating in a structurally different position from much of Asia. That difference is real and has clear underlying explanations. But with global cost of capital in a period of transition — the 30-year Treasury yield having just touched 5.121% — that gap will face continuous testing in the weeks ahead. The decisive factor is not where VN-Index set its record. It is whether domestic liquidity is durable enough to defend key support levels when external pressure intensifies.