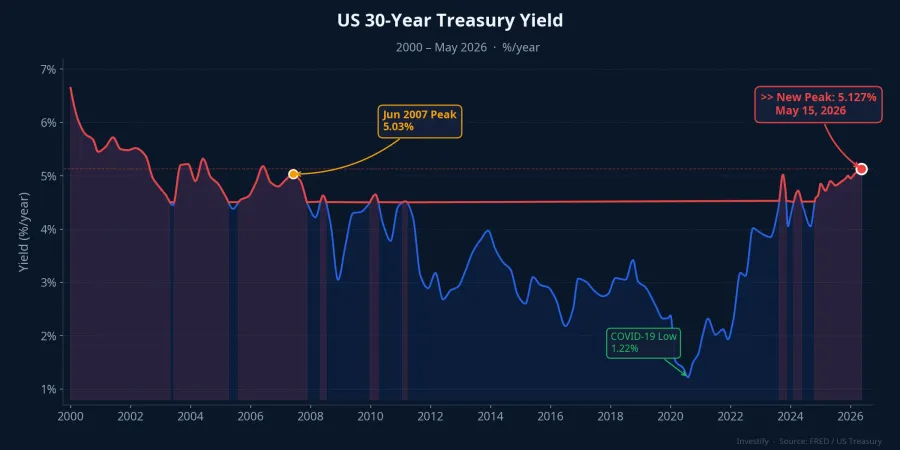

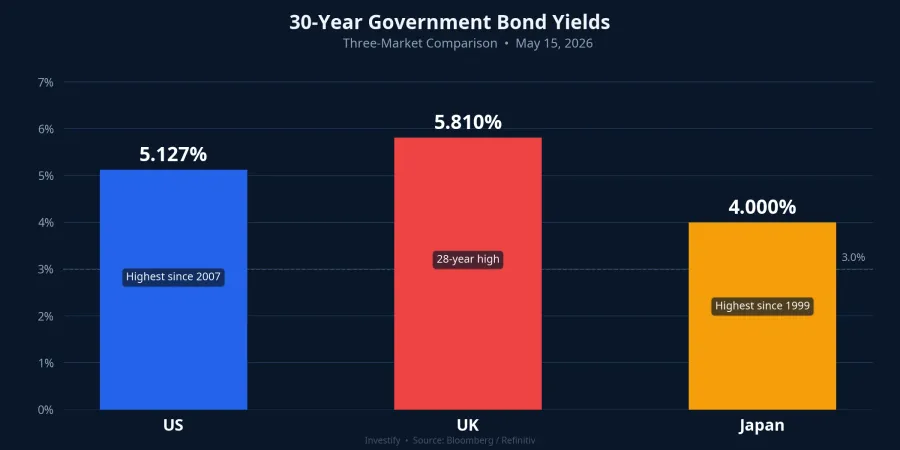

The week of May 11–15, 2026 produced a rare synchronised bond selloff across three of the world's largest markets. On May 15, the 30-year US Treasury yield hit 5.127%, the highest reading since June 2007.CNBCYahoo Finance At the same time, the UK's 30-year gilt rose to 5.81%, a 28-year peak, while Japan's 30-year government bond crossed 4% for the first time since the bond was first issued in 1999.TradingEconomics This was not an isolated selloff in one market but a simultaneous repricing of long-duration assets across the globe.

The headline "global bond selloff" instinctively signals "stay away from fixed income" for many retail investors. That instinct is half right — and half wrong.

Three Forces Pushing in the Same Direction

This week's yield surge had three identifiable sources, and they reinforced one another. In the US, April 2026 PPI came in at +1.4% month-over-month, the largest monthly jump since March 2022, pushing the annual rate to 6%.CNBC That reading sent the market-implied probability of a Fed rate hike back to nearly 50%. Brent crude held near USD 109 per barrel as US–Iran negotiations failed to produce a breakthrough, keeping the inflation narrative alive.NBC News In Japan, Bank of Japan signals of gradual tightening pushed JGB yields higher, repricing long-duration assets across Asia. In the UK, mounting fiscal concerns over heavier government borrowing, combined with persistent inflation, sent the 30-year gilt to a 28-year high.

The bigger picture is this: US inflation is anchoring dollar rate expectations higher for longer. That benchmark forces other markets to reprice upward to avoid net capital outflows. This is structural repricing of long-duration assets, a process that typically unfolds over months, not a single session.

Who Loses and Who Wins from the Same Number

The "selloff means avoid bonds" reflex is correct for a specific group of market participants. When yields rise, the market price of existing bonds falls: this is the fundamental inverse relationship. Three groups are genuinely hurt.

The first is institutional holders who must mark portfolios to market: open-end bond funds, insurers, banks. A rise in yields directly erodes NAV and regulatory capital. The second is leveraged portfolios with long-duration strategies: rapid price declines can trigger margin calls and forced sales. The third is entities preparing to issue new debt, since borrowing costs have suddenly risen.

For these groups, the week's yield surge is unambiguously bad news. International coverage written from their perspective is accurate within that scope.

But there is a fourth group for whom the "stay away" reflex is pointing in the wrong direction: investors who hold no bonds, are seeking stable income, and want to lock in a long-term yield. For them, 5.127% on US 30-year Treasuries is a level not seen in nearly 19 years, well above the 2.5–3.5% range that prevailed through 2020–2024. Buying now means locking in a 5.127% coupon stream for the next three decades, regardless of what the Fed does afterward. The same 5.127% figure means two different things because two groups stand at opposite points in the same cycle.

How 5.127% Looks from a Vietnamese Portfolio

Placing that number alongside domestic fixed-income channels reveals a more nuanced picture than "US yield is higher, therefore more attractive."

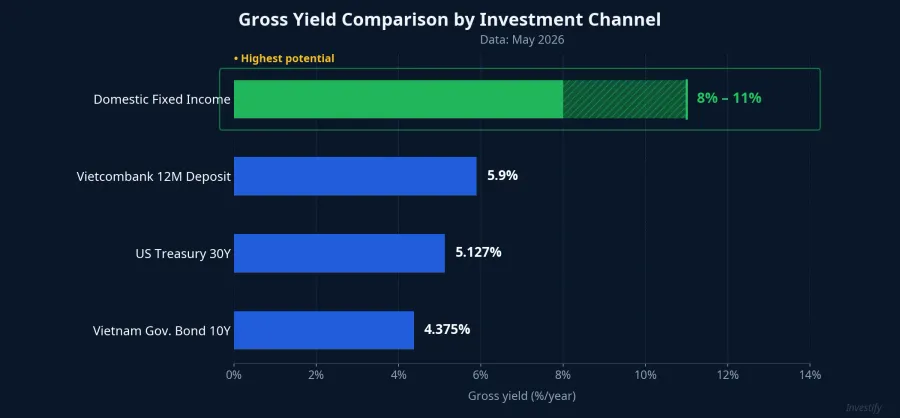

Vietnam's 10-year government bond was trading around 4.375% per market data on May 15, roughly 75 basis points below the US 30-year. But the 12-month deposit rate at Vietcombank currently sits at 5.9% per year24hmoney, which actually exceeds the US 30-year gross coupon in VND terms. The nominal yield gap does not tilt toward US Treasuries when viewed at face value in dong terms.

The real challenge is 30-year currency risk. The USD/VND rate stood at approximately VND 26,363 per dollar on May 15, roughly stable through the week. But over a 30-year horizon, compounding exchange-rate shifts become the dominant variable that most retail investors underestimate. Two scenarios matter independently. If holding in USD without hedging, the net VND yield could be very high if the dollar strengthens over time, or could be entirely wiped out if the dong appreciates, turning this into a leveraged currency bet layered on top of the yield bet. If hedging via forward contracts, the current interest-rate differential between USD and VND means hedging costs typically pull the net yield back toward domestic VND rates.

The practical outcome for most Vietnamese retail investors without a currency management framework: a 5.127% USD yield hedged back to VND works out to roughly 5–6% per year, not meaningfully different from a long-term Big 4 deposit, while domestic fixed-income products in the 8–11% range clearly outperform on a gross basis.

Which Channel Fits Whom

The May 11–15 bond selloff does not overturn the core question for Vietnamese retail investors. It simply restates it more clearly. At current yield levels and after fully accounting for currency risk, domestic fixed-income channels are where Vietnamese individual investors hold a genuine comparative advantage, not US 30-year Treasuries.

For portfolios weighted heavily toward equities — at a moment when global markets are signalling a broader repricing (Dow Jones down 1.1%, S&P 500 down 1.2% in the May 15–16 sessions) — considering a 20–30% allocation to domestic fixed income represents a common defensive framework under these conditions. The precise allocation depends on each portfolio's accumulation stage and risk tolerance.

The most important data point to monitor over the next four to six weeks is not the 5.127% figure itself but the US May CPI release, expected mid-June. If US inflation remains persistent, global yields will face another round of upward pressure, and the transmission channel to Vietnam's policy rate — currently at 4.50% — will matter far more for domestic investors than the raw comparison of gross yields across two very different currency regimes.