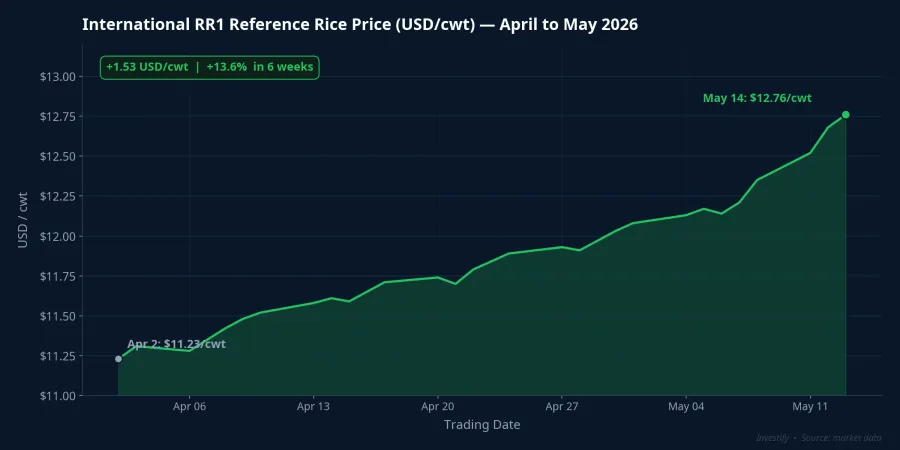

In the first week of May 2026, Vietnam's Jasmine export rice was being quoted at USD 513–517 per tonne, up roughly USD 30/t from the previous month and the highest in a decade.VnExpress On the international futures market, the RR1 benchmark price rose from USD 11.23/cwt on April 2 to USD 12.76/cwt on May 14, with almost no down sessions over the entire six-week stretch.

The instinctive read when you hear "10-year high" is to buy the sector. Looking at the numbers, the picture is considerably more complex: export prices rising is only one side of the equation, while input costs are climbing at nearly the same pace. And the single most headline-grabbing profit figure in Vietnamese agribusiness this quarter came from a one-time divestiture, not from the rice cycle at all.

Three Mechanisms Driving the Jasmine Price

The current price floor is not the product of a single catalyst. Three mechanisms are converging simultaneously to hold Jasmine above USD 510/t.

The first is a surge in strategic reserve demand. In the first four months of 2026, the Philippines imported approximately 1.46 million tonnes of rice from Vietnam, accounting for more than 86% of its total rice imports.Dân Việt The USDA has revised its forecast for Philippine rice imports in 2026 up to 5.5 million tonnes, which would be a record.Thanh Niên The 2023–2024 shortfall fundamentally changed how major regional importers manage supply: from spot-buying small lots to signing long-term forward contracts and building strategic stockpiles rather than operating on minimum buffers.

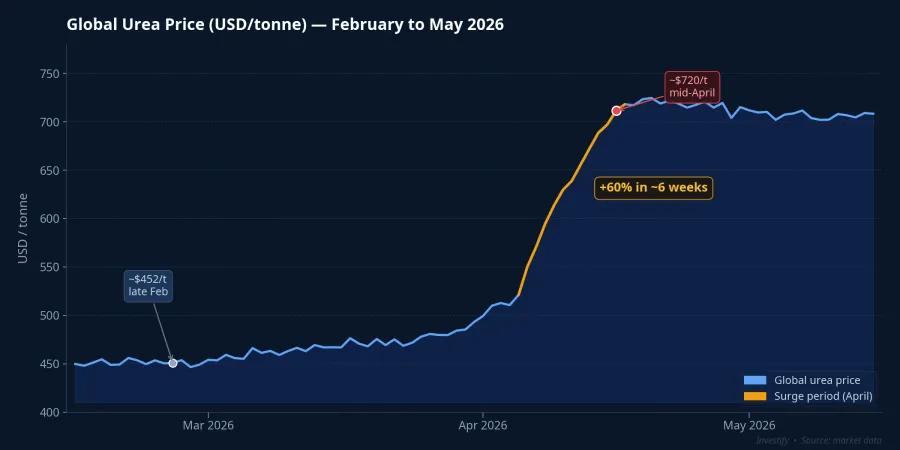

The second is a fertilizer cost shock. Global urea prices jumped from around USD 452/tonne in late February to around USD 720/tonne by mid-April, a roughly 60% increase in just eight weeks. Domestic Vietnamese urea prices rose even more sharply, from approximately USD 475/t to around USD 830/t over the same period, because the local market relies heavily on Gulf-region imports routed through the Strait of Hormuz, which has faced shipping disruptions. Since fertilizer is one of the largest cost items in paddy cultivation, this shock fed directly into farmgate cost structures. The gain farmers saw from higher rice prices was substantially offset by the increase in their input bill.

The third is a contraction in domestic supply. By end of March, the winter-spring crop planting area nationwide stood at approximately 2.92 million hectares, down 1.3% from the same period last year.Báo Chính phủ Many localities have been converting paddy land to higher-value crops or ceding it to infrastructure and industrial zone development. The result is less commercial rice entering the market during the peak harvest window, which adds another structural floor under export prices.

These three mechanisms do not operate in isolation. Strategic import demand pulls prices up from the buy side; rising input costs push up the production cost floor; and tighter domestic supply reduces the volume available for export. That is what is holding Jasmine at its ten-year high, not a speculative bubble.

The Value Chain Does Not Share Gains Equally

A USD 30/tonne increase in FOB price does not translate into USD 30 of additional income for everyone in the supply chain.

Farmers sit at the top of the production chain but carry the highest input risk. Farmgate paddy prices have risen year-on-year, but the real improvement in farm income is far narrower than the export price gain because fertilizer costs climbed in near-parallel. The clearest beneficiaries are large exporters that locked in long-term contracts with the Philippines or China early: they sold forward at high prices while sourcing paddy at prevailing spot prices at each harvest window. Rice millers and traders profit from inventory positioning: buy when the trend turns up, sell when the market cools. Logistics providers charge fixed per-tonne rates and have almost no direct exposure to rice price movements, though they face their own cost pressures from the same geopolitical disruption driving up fuel and insurance costs.

For investors, the practical implication is straightforward: not every stock tagged "rice sector" benefits equally when Jasmine prices rise. Where a company sits in the value chain largely determines what share of that USD 30/t increase actually reaches its bottom line.

PAN Group's "40x" Headline and the Earnings Trap

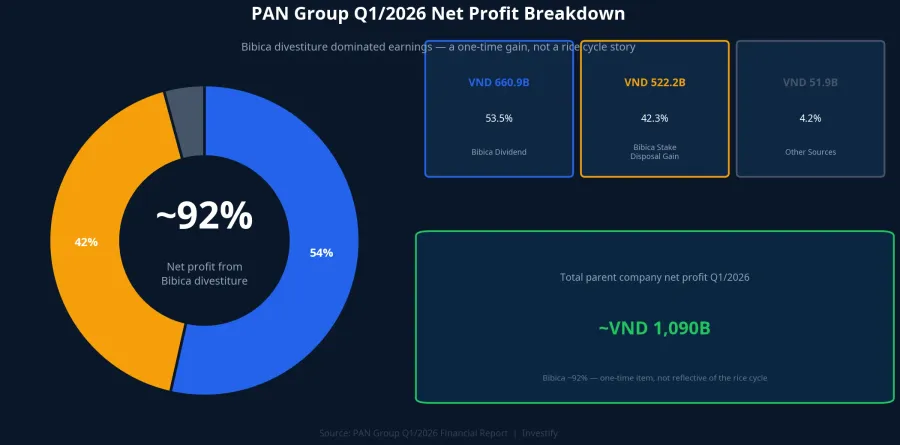

This is where new investors most easily get caught. PAN Group just reported Q1/2026 parent company net profit of approximately VND 1,090 billion, up roughly 40x year-on-year.CafeF That headline, placed next to a record rice price story, creates an easy but incorrect inference: "PAN is in rice, rice is at record prices, profits are up 40x — buy."

Looking at the revenue breakdown, that logic fails immediately.

The dominant contributors to that VND 1,090 billion figure were a dividend received from Bibica (VND 660.9 billion) and a gain on the disposal of a Bibica stake (VND 522.2 billion). Both are proceeds from a divestiture event. They occurred once and have no connection to rice price dynamics in the quarter. Even if Jasmine stays at USD 517/t through year-end, Q2 earnings will not replicate this figure through the same mechanism.

The key analytical point: the premise of the trade was wrong from the start. An investor buying PAN on a "rice cycle" thesis needs to answer a prior question: what share of PAN's revenue is directly tied to rice export operations, and how does that segment's margin behave when FOB prices move? Without that answer, the 40x number is a headline, not an investment argument.

A Framework for Commodity Stock Analysis

When analyzing a commodity-linked stock, two variables need to run in parallel: the output price and the input cost. A USD 30/t gain on rice export prices while urea costs surge 60% produces a net margin equation that is far less flattering than the revenue line suggests. A strong number on one axis can be substantially eroded by the other before any benefit reaches shareholders.

Key variables to monitor for this cycle: new import contract announcements from the Philippines and Indonesia; the international urea price index, particularly as the Hormuz situation evolves; and the summer-autumn planting report from the Ministry of Agriculture. If (a) Philippine import demand holds, (b) Hormuz shipping does not fully normalize, and (c) the summer-autumn crop area does not recover strongly, the current price level has a reasonable basis to persist at least through mid-year.

For stock selection, the working principle is to isolate the portion of a company's revenue that is genuinely tied to rice export prices from everything else under the agribusiness label. Only that segment responds to the current cycle. The rest operates on its own drivers and timeline. Mixing them all into a single "rice stock" thesis is a reliable way to misread a financial report.