VIC closed at VND 228,000 on May 15, 2026; VHM at VND 158,000. Both sit near all-time highs. For most retail investors, the instinct is familiar: prices have run far, risk is elevated, better to stand aside and wait. Meanwhile, Dragon Capital — managing nearly USD 2 billion in assets — just increased its allocation to both names to approximately 17% of NAV, a concentrated position for an active fund that otherwise prioritises diversification.Nhịp Sống Nhà Đất

Two camps, same prices, two completely different readings. Dragon Capital has a specific valuation framework. They laid it out directly in a webinar on the afternoon of May 15, 2026. This post unpacks that framework and, more importantly, the three risks that could break the "not yet the peak" thesis.

April Action: Three Member Funds Buying in Unison

April 2026 transaction data shows the accumulation was not from a single fund. At least three Dragon Capital member funds moved in the same direction simultaneously.VietnamBiz

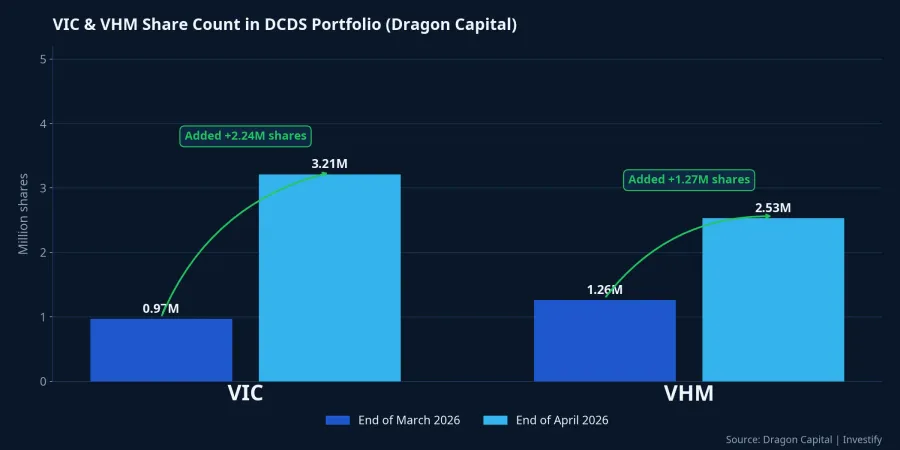

DCDS — the flagship equity fund of the group — logged the largest shift. Its VIC holding grew from 965,800 shares at end-March to 3.21 million shares at end-April, an addition of over 2.24 million shares. VHM grew from 1.26 million to 2.53 million shares, adding nearly 1.27 million. DCDE opened new positions in both VHM and VRE during the month. VEIL — the largest foreign-facing fund in the Dragon Capital system — raised its allocation to both VIC and VHM as well.

By the May 8 and 11 snapshots, DCDS alone held VIC at 10.45% of NAV and VHM at 5.63% of NAV. Across the whole group, the combined weight of the two names reached approximately 17% of NAV. That figure is significant because DCDS avoided VIC and VHM for years, returning only in 2025. That pivot contributed substantially to the fund's more than 30% return that year.VnExpress Continuing to build in April 2026 signals a long-term position, not a short-term trade.

The Two Valuation Frameworks Dragon Capital Uses

In the May 15 webinar, Dragon Capital's analyst addressed the "overheated" question head-on with two comparative frameworks.

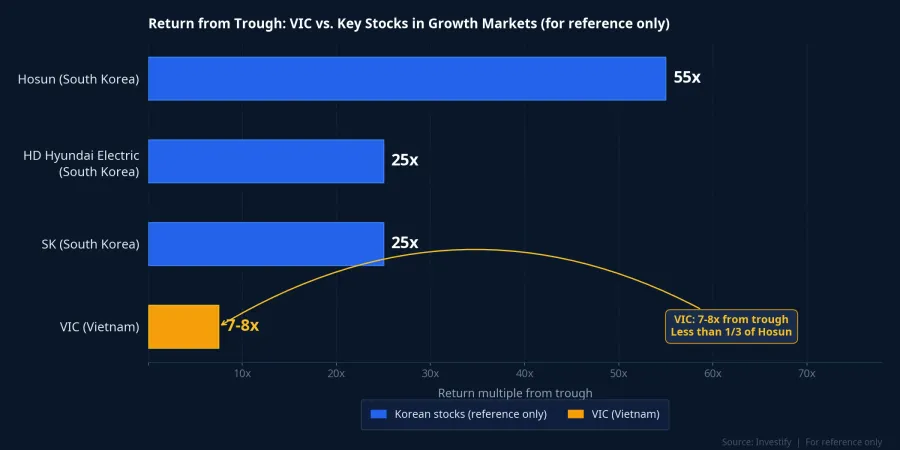

Framework 1: Against anchor stocks in other growth markets. The analyst cited South Korean equities: Hosun rose 55x from its trough; HD Hyundai Electric and SK each rose approximately 25x during phases of clearly led economic expansion.CafeF Against that backdrop, VIC has risen roughly 7-8x from its trough: less than one-third of Hosun, less than half the 25x group.

This framework does not claim VIC will follow Hosun's trajectory. Each market has its own dynamics. What Dragon Capital is trying to break is the psychological reflex that "7-8x must be the top": in historical growth cycles, 7-8x has typically been the midpoint, not the ceiling.

Framework 2: Against its own adjusted historical price. Taking VIC's 2018-2019 highs as a baseline and adjusting forward, the current price still represents less than 5x growth over nearly 7-8 years. For VHM, today's price is only about 100% above its peak from five years ago. At that pace of appreciation, Dragon Capital argues, we are looking at normal compounding for a business operating at full capacity, not a bubble.

Two Different Valuation Stories Inside the Same Group

Dragon Capital bought both VIC and VHM, but the two names carry entirely different valuation logic. This is the distinction retail investors typically miss when they lump "Vingroup stocks" into one bucket.

VHM trades at a low valuation multiple by Dragon Capital's framework: P/E in the single digits, well below the 2023-2025 historical range. This is a cash-flow delivery story. VHM books revenue when it hands over completed apartments, and it maintained strong delivery pace throughout 2025. Investors are buying a predictable earnings stream, conditional on deliveries staying on schedule.

VIC is a completely different bet. Its current price reflects expectations about VinFast and the broader group restructuring, not existing earnings power. Dragon Capital is running both positions in parallel: VHM for current cash flows, VIC for the upside scenario if VinFast crosses into profitability. These are two independent investment theses packaged in the same portfolio because they complement each other, not because they are similar.

Three Risks That Could Break the Thesis

The "not the peak" thesis is logically grounded. But it is not unconditional. There are three layers of risk investors need to monitor.

VinFast execution risk. Per its 2025 annual financial results, VinFast recorded a net loss exceeding VND 97,000 billion, with negative equity of more than VND 90,000 billion.VnExpress The restructuring plan calls for transferring VND 182,000 billion in debt to another entity within the group, with a target of reaching profitability by 2027.BaoMoi If the target of 300,000 vehicle deliveries in 2026 falls short, or if expansion costs in the US, India, and Indonesia exceed projections, the expectation premium embedded in VIC's price will need to be repriced — and quickly.

VHM delivery progress. The VHM thesis rests on one clear assumption: deliveries stay on track or ahead of schedule. In 2025, VHM delivered on that. But the 2025-2037 project pipeline — including a complex of more than 58,000 apartments in central Vietnam — carries legal, land clearance, and market absorption risks. A single slow quarter on deliveries is enough to pull revenue and cash flow below the model that today's low valuation multiple implies.

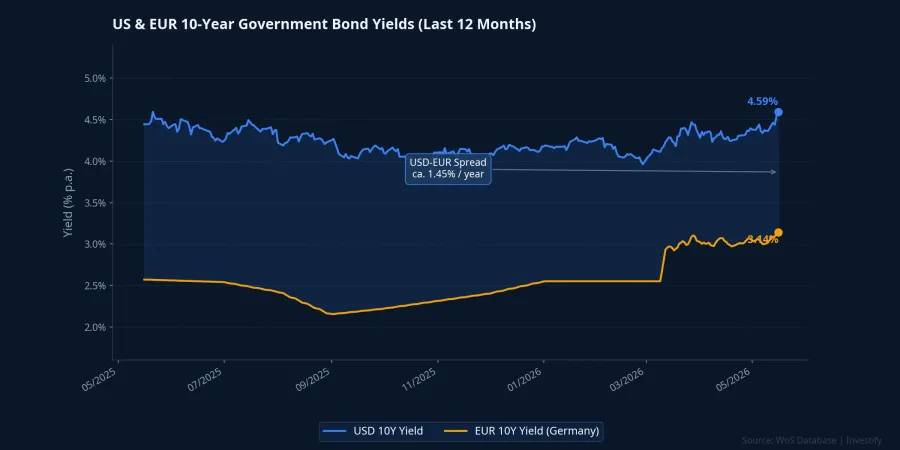

International interest rates. Vingroup is planning to issue up to USD 350 million in international bonds in Q2/2026, with a maximum nominal rate of 5.75% per annum over a 5-year term.Tin Nhanh Chứng Khoán The macro backdrop is not supportive: the Fed is expected to cut only once in 2026, while the 10-year German Bund yield has surged from around 2.5% to above 3% since the start of 2026 on fiscal expansion. Sustained elevated USD and EUR rates will push Vingroup's foreign borrowing costs higher and compress the discount rate on which VIC's long-duration valuation partly depends.

A Decision Framework for Investors

The VN-Index closed at 1,921.60 points on May 16, 2026, just below its all-time high of 1,925.46 set on May 14. With the market near its peak and VIC and VHM also near their historical highs, the question of "hold or trim" has no universal answer.

What stands out in Dragon Capital's thesis is its conditional structure. The fund is not saying "buy at any price." It is placing a bet anchored on two comparative frameworks and two specific outcome scenarios: VinFast crossing into profitability, and VHM sustaining delivery pace. Both are testable hypotheses, and both will be resolved over the coming quarters.

For investors already sitting on 30-40% or more in VIC or VHM, trimming a portion to reduce exposure at a resistance zone is a standard defensive tactic, entirely rational even without rejecting the long-term thesis. For those without a position, the decision to enter should not be driven by price level alone, but by one's own conviction regarding the three risks outlined above.

Three data points worth tracking over the coming quarters: VinFast actual vehicle deliveries versus the 300,000-unit target for 2026; VHM revenue recognition from completed handovers in the Q2 and Q3 financial reports; and the final coupon on Vingroup's planned USD 350 million international bond issuance. Those three figures, not the level of the ticker on a brokerage screen, will determine whether Dragon Capital's framework continues to hold.