Vietnam's Circular 08/2026/TT-SBV took effect on May 15, 2026, allowing banks to include 20% of State Treasury term deposits in the LDR denominator. This was the regulatory relief that the Big 4 state banks had been waiting for since the start of the year. Circular 26/2022 had progressively excluded Treasury deposits from the LDR denominator, and once the 100% exclusion kicked in on January 1, 2026, the LDR ratios of all four banks pressed up against the 85% regulatory ceiling.Nguoi Quan Sat

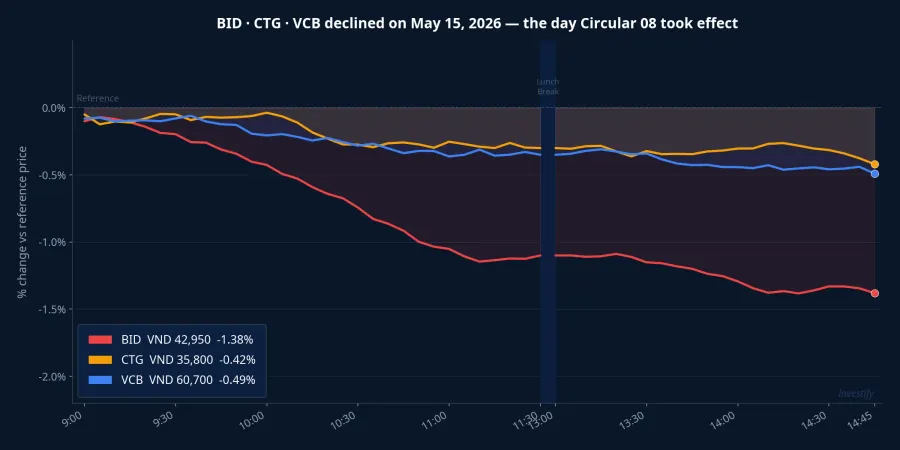

Yet on the very same session, all three listed Big 4 banks closed in the red: BID at VND 42,950 (down 1.38%), CTG at VND 35,800 (down 0.42%), VCB at VND 60,700 (down 0.49%). The market did not celebrate the good-news policy taking effect. Reading the data carefully reveals why.

What is LDR and why did the Big 4 face pressure this year

The LDR (loan-to-deposit ratio) is one of the most important safety limits in Vietnam's banking system. Under current regulations, Big 4 banks must keep this ratio below 85%. When LDR approaches the ceiling, a bank technically has little room to grow its loan book.

The pressure emerged at the start of 2026 when Circular 26/2022's final phase took hold.VietnamBiz That circular had gradually phased out State Treasury deposits from the LDR denominator: 50% excluded in 2023, 60% in 2024, 80% in 2025, and 100% from January 1, 2026. Once 100% exclusion hit, the denominator shrank sharply, pushing the Big 4's reported LDR ratios up against the 85% limit.

Circular 08 partially reverses that trajectory. Banks may now count 20% of term Treasury deposits back into the LDR denominator. The adjustment applies only to term deposits, not demand deposits, and took immediate effect from the date of issuance.

One key point to understand: this is a formula adjustment, not new capital. The denominator is wider, so the reported LDR ratio falls, but total funds actually flowing into the system are unchanged. The circular does not touch the short-term funding for medium- and long-term lending ratio either.

How much additional lending room does the Big 4 gain

The scale of State Treasury deposits at the Big 4 is striking. According to VietnamBiz, total term Treasury deposits at the three listed Big 4 banks reached approximately VND 563,036 billion at the start of 2026, up nearly 39% from end-2025.VietnamBiz The balances are distributed fairly evenly: roughly VND 188,600 billion at BIDV, VND 185,300 billion at VietinBank, and VND 189,200 billion at Vietcombank.

Applying the 20% formula, each bank's LDR denominator increases by roughly VND 37,000 to 38,000 billion. At the 85% LDR cap, this unlocks approximately VND 31 trillion in additional theoretical lending capacity per bank.

That sounds significant, but context matters. BIDV's current loan book is approximately VND 2,390 trillion; VietinBank's is roughly VND 2,030 trillion; Vietcombank's is around VND 1,750 trillion. The newly unlocked room amounts to only about 1.3 to 1.8% of each bank's existing loan portfolio. It is enough to bring the reported LDR below the safety threshold, but not a substantial catalyst for accelerating credit growth.

Agribank, the one Big 4 bank not yet listed, does not publish a separate breakdown of its Treasury deposit balance. Given its loan book of roughly VND 2,000 trillion and its historical role as a major Treasury fund channel into agriculture and rural areas, the benefit it gains is likely similar in magnitude to the three listed peers.

Why bank stocks still fell despite the good news

The liquidity story in 2026 is about more than just the LDR formula. Báo Đầu Tư posed the question directly: even with looser LDR rules and a higher Treasury deposit ceiling, the banking system's liquidity thirst in 2026 remains unquenched.Báo Đầu Tư

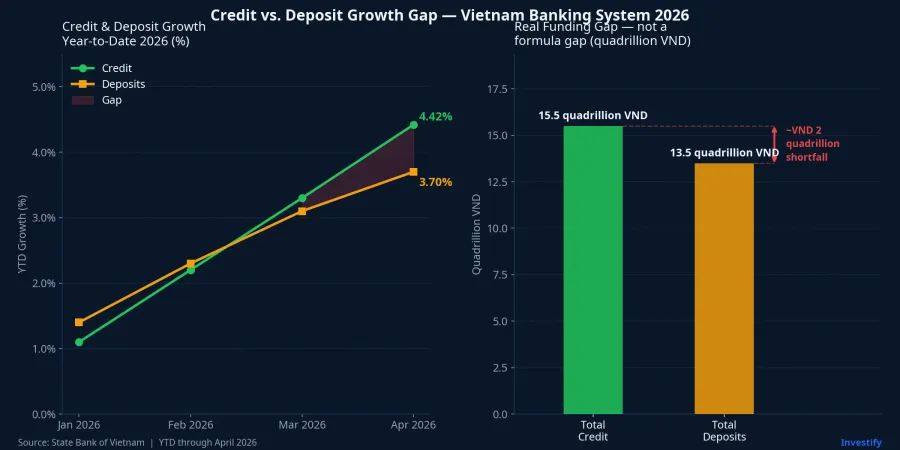

The first pressure is a real funding gap. The gap between total system credit and total deposit mobilization has widened to approximately VND 2,000 trillion: credit grew 4.42% year-to-date through April 2026 while deposit growth lagged behind. Circular 08 only allows banks to re-classify existing deposits in the formula; it does not create new funding.

The second pressure is a structural maturity mismatch. Most deposits in the system carry short maturities, while demand for medium- and long-term loans continues to grow. This structural issue lies entirely outside the scope of an LDR formula change.

The third pressure is the distinction between "permitted lending room" and "cash available to disburse." Even with the formula-based LDR eased, a bank that wants to actually grow credit must still raise additional deposits. This circles back to pressure number one.

Two scenarios for using the new headroom

With roughly VND 31 trillion in fresh LDR headroom, each Big 4 bank has two paths. The first is to push credit: deploy the headroom to grow the loan book and lift net interest income. The second is to ease funding pressure: use the headroom to reduce the urgency of deposit-raising, which in turn creates room to lower deposit rates and trim funding costs.

The May 15 session suggests the market is pricing in the second scenario. The logic is straightforward: if the Big 4 were gearing up to aggressively expand credit on the back of the new headroom, institutional buyers would typically front-run the news before it takes effect, not sell into it afterward. The fact that all three listed names closed lower on the day Circular 08 became law implies that investors read it as a defensive move — loosening one binding constraint — rather than a growth catalyst.

Two signals to watch over the next two to four weeks

Two data points will clarify which scenario is playing out.

The first is the Big 4's 12-month deposit rate. These banks currently offer roughly 5 to 5.5% per annum on 12-month savings. If, over the next two to four weeks, any of the Big 4 trims its longer-term deposit rates, it signals that the LDR headroom is being used to cut funding costs rather than to scale up lending.

The second is weekly credit growth data from the State Bank of Vietnam. System credit is currently running at 4.42% YTD through April 2026. If growth accelerates into the 5.5 to 6% range in May and June, the Big 4 are deploying headroom to genuinely expand lending, not just to manage their regulatory ratios.

Circular 08 has removed one of three constraints on Vietnam's banking system liquidity in 2026. Any expectation of its impact on Big 4 earnings should be calibrated accordingly: the new headroom represents 1.3 to 1.8% of the existing loan book: enough to improve reported safety ratios, but not enough to shift the full-year credit growth trajectory materially. Which scenario prevails will become clearer within the next two to four weeks, once the two signals above begin to emerge.