Vietnam Airlines reported consolidated after-tax profit of VND 4,514 billion in Q1/2026, with revenue exceeding VND 37,500 billion, up nearly 30% year-on-year.Vietstock On paper, a strong quarter. Yet just six weeks after the Q1 books closed, top leadership is working at half pay: the Chairman took a 50% salary cut, Deputy CEOs 40%, and department heads 30%.CafeF

These two data points are not a contradiction. Between them sits a fuel cost shock that materialized entirely after March 31. HVN investors need to read it correctly before making any second-half decisions.

The Shock That Happened After Q1 Closed

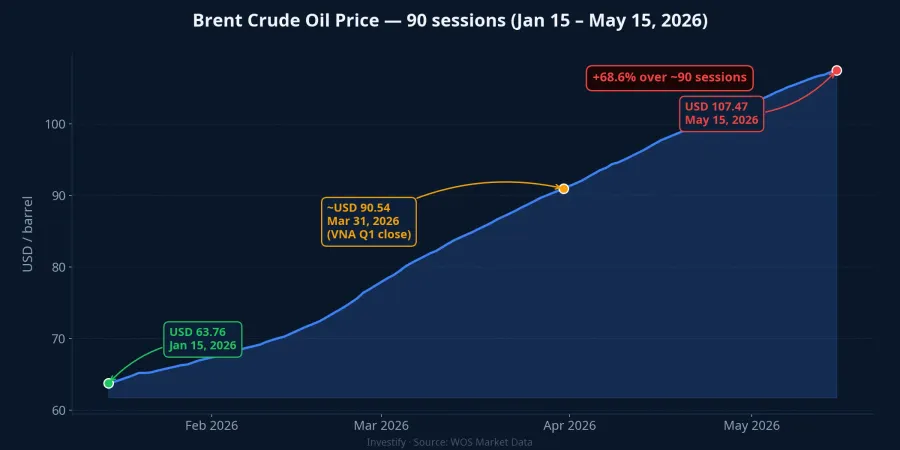

When Vietnam Airlines closed its Q1 books on March 31, Brent crude was trading around USD 90.54 per barrel. By May 15, Brent settled at USD 107.47, a gain of roughly 18.7% in just six weeks. Tracing further back to mid-January 2026, when Brent was at USD 63.76, the price has surged 69% over 90 trading sessions, driven primarily by unresolved tension around the Strait of Hormuz.

Jet A1, the refined product closest to kerosene and the primary aviation fuel, tends to move with Brent but at wider amplitudes due to refining margin dynamics. At the "Aviation and Tourism Demand Stimulus" forum on the morning of May 15, Mr. Dinh Van Tuan, Deputy CEO of Vietnam Airlines and Chairman of Pacific Airlines, stated that Jet A1 is currently hovering around USD 160 per barrel, some USD 70 to 80 above the airline's initial full-year plan.Thanh Nien

That USD 70 to 80 gap is the core of the cost calculation that follows.

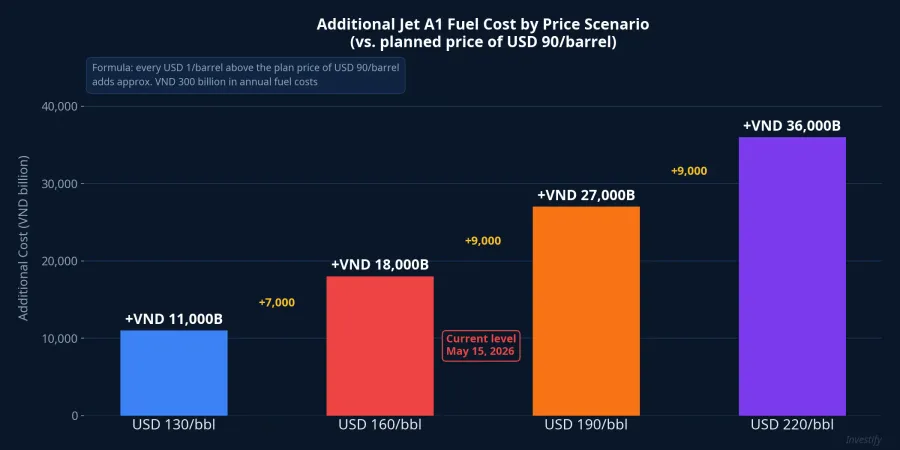

The Fuel Formula: Every Dollar Above Plan Costs VND 300 Billion

According to VNA's own disclosure, every USD 1 per barrel above the plan price translates into approximately VND 300 billion in additional annual fuel costs.CafeBiz With Jet A1 currently running USD 70 to 80 above plan, if sustained for a full year, the additional fuel bill would fall in a range of roughly VND 11,000 to 27,000 billion, depending on the actual price level.

Fuel accounts for 30 to 40 percent of VNA's total operating costs. That cost structure makes VNA far more sensitive to oil price swings than most listed companies. Paradoxically, VNA reacts to Brent moves in the opposite direction to oil stocks, and with a larger relative magnitude: rising prices compress margins rather than expand them.

Q1's VND 4,514 billion profit is a meaningful buffer, but only if Brent retreats quickly toward the plan price. If Jet A1 holds near USD 160 per barrel through the remaining three quarters, that Q1 cushion will not cover the accumulated cost overage.

Three Scenarios, One Variable

VNA's accumulated losses stood at VND 22,303 billion as of March 31. At the May 15 forum, Mr. Tuan stated that if the airline maintains its planned capacity while current fuel prices persist, accumulated losses could rise to approximately VND 30,000 billion by the end of 2026.CafeBiz The VND 7,700 billion gap between these two figures represents the additional loss VNA projects over Q2 through Q4 if the worst-case scenario persists.

Three paths diverge from here, distinguished by exactly one variable: Brent crude prices from now through year-end.

Scenario 1: Hormuz tension persists, Brent stays above USD 100 through 2026. Jet A1 near USD 160 per barrel sustained through the year pushes additional fuel costs toward the upper end of the range. Q1's VND 4,514 billion profit is insufficient to offset the compounding cost overruns in Q2 through Q4. VNA posts a net annual loss, and accumulated losses swell toward VND 28,000 to 30,000 billion. Equity turns negative, replicating the scenario that played out after Covid and required a special National Assembly support package in 2024. Valuation pressure on HVN under this path is unambiguous.

Scenario 2: Iran negotiations succeed, Brent retreats to USD 85 to 90 by June or July. Jet A1 eases to roughly USD 110 to 130 per barrel, still USD 30 to 50 above plan. Full-year additional costs fall into the middle of the range. VNA may preserve a thin net profit, supported by the Q1 baseline and peak summer travel revenue. Accumulated losses decline slowly; the path to full loss elimination extends into 2027 or 2028 rather than closing in 2026 as originally targeted. HVN avoids balance sheet stress but does not deliver a clear recovery story.

Scenario 3: VNA reduces capacity and restructures its route network in June or July. This is the option leadership is explicitly leaving open. Salary cuts are a short-term measure; the bigger lever is the flight schedule and fleet deployment. Cutting flights on routes with negative contribution margins and deferring summer capacity additions reduces fuel costs proportionally, but revenue falls with it. This is a "stop the bleeding" scenario rather than a cure: it avoids Scenario 1 but cannot replicate Scenario 2.

On the price chart, HVN has corrected from the VND 22,800 to 23,100 range in mid-April to VND 21,350 on May 15, a decline of roughly 7% over six weeks. Market capitalization stands at approximately VND 66,400 billion. The move tracks the Brent surge in direction but has not yet fully priced in Scenario 1.

Three Signals That Separate the Scenarios

The practical question is not "buy or sell HVN" but "which scenario is currently materializing." Three signals can resolve this within the next four to six weeks.

The first is Hormuz. If tensions escalate further through late May, Scenario 1 becomes the working assumption. Any credible signal of Iran diplomatic progress opens Scenario 2.

The second is VNA's June and July flight schedule. If the airline announces route suspensions or capacity reductions on low-margin routes, Scenario 3 is being activated, signaling that management believes Brent will remain elevated.

The third is the USD 100 per barrel threshold. Brent closing below USD 100 for three consecutive sessions is an early indicator of Scenario 2. Sustained closes above USD 110 per barrel confirm Scenario 1.

The Data Point That Matters Most

The structurally important feature of HVN is its asymmetric oil sensitivity. Energy stocks benefit when Brent rises; VNA is hurt, and typically with a larger relative move. That is a permanent characteristic of the cost structure, not a cyclical anomaly.

Q1's VND 4,514 billion profit is a solid starting point, but it is already history. The decisive variable for the rest of 2026 is Brent: does it retreat below USD 90 per barrel, or does it hold above USD 100? Whichever path it takes will determine whether VNA's year-end accumulated losses settle at the low end — around VND 22,000 billion — or the high end, near VND 30,000 billion.

The Q2 report, expected in late July, will be the first hard confirmation of which scenario has played out. But the leading signals — Hormuz developments, the summer flight schedule, and Brent's behavior around the USD 100 threshold — are already observable, and they will begin resolving the uncertainty well before VNA publishes its next earnings.