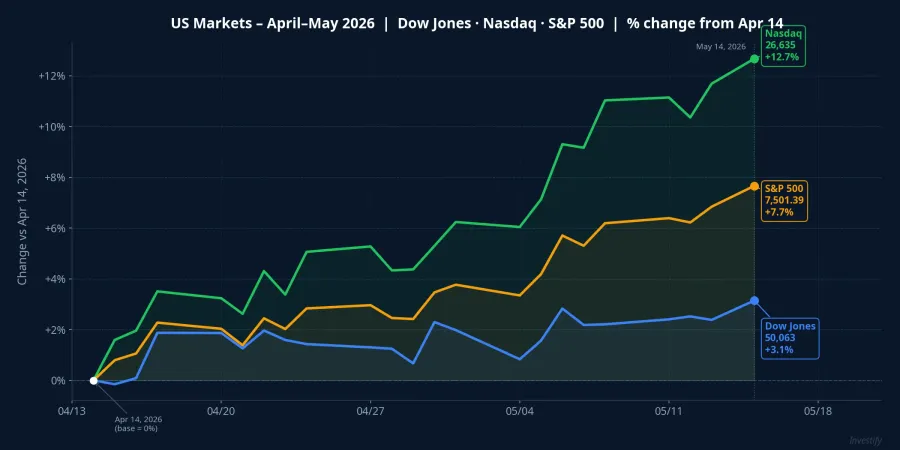

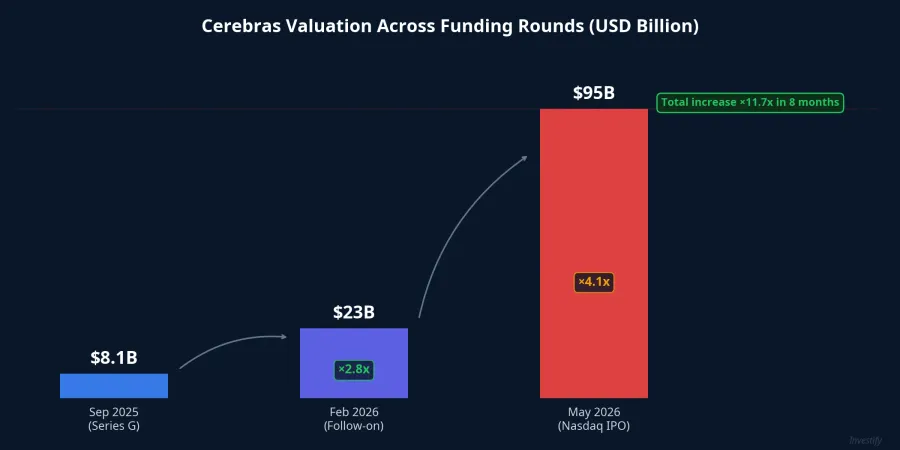

On the night of May 14, 2026, an old milestone and a new entrant appeared together on Nasdaq. The Dow Jones closed at 50,063.46, marking its first return to 50,000 territory since February 2026. In the same session, Cerebras Systems began trading under the ticker CBRS, priced at $185 per share, closing at $311.07 and raising $5.55 billion at an implied valuation of roughly $95 billion.TechCrunch

These two events are not coincidental. Together they close out a three-act story in the AI chip market: a journey from Nvidia holding an almost unchallenged position to a genuinely fragmented competitive landscape. The big picture is not the story of a single trading session, but the result of 42 months of market restructuring accumulating to this moment.

Three Phases of the AI Chip Market

Phase 1: ChatGPT opens the door, Nvidia walks through alone

In November 2022, ChatGPT launched and ignited an unprecedented surge in demand for AI infrastructure. At that point, virtually every large language model was trained on a single chip type: Nvidia's H100 GPU. Demand outstripped supply almost immediately. By 2023, H100 had become scarce. Major data centers were booking compute capacity quarters in advance; AI compute rental prices climbed sharply, pushing Nvidia's data center revenue higher.

The gap in the market was unmistakable: all training and inference demand concentrated with a single supplier. Alternative solutions were almost entirely absent from the commercial market during this phase. AMD was developing its MI series but had not yet captured meaningful share. Cerebras, founded in 2015 with a distinctive wafer-scale architecture, was still primarily serving scientific research and a handful of enterprise clients.

Phase 2: Competition begins filling the gap

The supply-demand gap drew alternative solutions into the market. AMD released the MI300X in late 2023, positioning it directly against the H100 for large-model training workloads. Groq introduced its Language Processing Unit (LPU), an accelerator purpose-built for inference rather than training, targeting a segment where GPUs are not well-optimized.

Cerebras continued scaling. In September 2025, the company raised approximately $1.1 billion in its Series G at a post-money valuation of roughly $8.1 billion. In February 2026, a follow-on round raised approximately $1 billion more, lifting the valuation to roughly $23 billion. Nearly tripling in valuation over five months signaled that capital demand in the sector had shifted: no longer early-stage venture, but institutional capital positioning ahead of the public markets.

At the same time, US export policy on chips to China continued tightening. From 2022, the US restricted high-performance GPUs including the H100. In 2024, Nvidia developed the lower-spec H20 to maintain some access. By April 2025, the H20 also required a license. That sustained pressure effectively pushed China to develop domestic alternatives, fragmenting AI chip architectures on a global scale.

Phase 3: Multi-competitor landscape and selective reopening

By early 2026, the AI chip market had at least four genuinely competing branches: Nvidia and AMD's traditional GPU lines, Cerebras's wafer-scale architecture, Groq's LPU, and custom accelerators built in-house by major tech companies such as Google's TPU. The critical distinction is that each branch is optimized for a different type of workload. This is not a market where one challenger replaces Nvidia outright; it is a market where each challenger captures a distinct segment.

On the same night of May 14, the US announced it would allow H200 exports to China to resume, but still on a case-by-case licensing basis. This is not a broad relaxation; it reverses the continuous tightening trend that ran from 2022. The practical logic: if the US refuses to sell, China already has domestic alternatives in development, and the US loses revenue without achieving its technology-control objective. Three events on the same evening, the Dow returning to 50,000, the Cerebras IPO gaining 68.3%, and the H200 license reopening, collectively describe the same shift: the AI chip market has moved from dependence on one supplier to a genuinely fragmented multi-competitor structure.

Nasdaq Rally: Genuine Foundation or Late-Cycle Acceleration?

Nasdaq closed May 14 at 26,635.22, up 12.7% over one month. The S&P 500 reached a new high at 7,501.39. A 12.7% move in a broad index over 30 days is a wide swing, wide enough to ask whether this reflects a structurally supported rally or a late-cycle acceleration.

The case for structural support has real evidence. AI-segment revenue at Nvidia, Microsoft, Alphabet, and Meta has grown sequentially. Cerebras's IPO is not pure speculation: it is a company with real revenue, established enterprise clients, and long-term contracts. AMD and Groq both expanding confirms that AI infrastructure demand is diversifying, not concentrated in a single name.

The cautionary case also has evidence. Cerebras's implied valuation of roughly $95 billion is approximately 90 times its most recent annual revenue, high by any measure, even against fast-growing technology benchmarks. A 68.3% first-day pop signals the market is willing to pay a premium for anything carrying the "AI chip" label. That kind of enthusiasm has appeared in previous bubble phases: dot-com in 1999 to 2000, crypto in 2021.

The more defensible framing is that both states coexist. The rally has real earnings support at the leading companies, but valuations at several names have run ahead of that foundation. History shows that even fundamentally-supported rallies can correct sharply when sentiment turns, even if the long-term thesis remains intact.

Vietnamese Investors and the Global AI Chip Story

In practical terms, access to the Nasdaq rally from a locally-opened brokerage account is very limited. Vietnam's major domestic funds — Dragon Capital and VinaCapital — focus primarily on Vietnamese equities. There is currently no domestic open-end fund or ETF that directly tracks the Nasdaq index or a basket of US technology stocks.

Opening an account with an international broker allows direct purchase of US-listed stocks including CBRS, NVDA, and AMD, but retail investors must navigate foreign exchange control regulations, which do not freely permit individuals to move capital offshore for foreign securities investment. Some specialized foreign funds are open to qualifying professional investors, but entry thresholds are high and liquidity is limited.

The practical gap between the global AI chip story and a Vietnamese retail investor's portfolio sits here: the narrative is followable and the analysis is applicable, but there is no domestic product to act on. The lessons from the three-phase journey still apply to reading the domestic market. Vietnamese technology stocks such as FPT and CMG are not AI chip companies, but they do carry sentiment exposure to global technology trends. Expectations for those names warrant the same discipline: evaluate against actual revenue data, not against the momentum arriving from US markets.

Three Signals Worth Watching

Capital is moving within the AI chip market, but three signals will determine whether this rally has a durable foundation or is entering a late-cycle acceleration phase.

First, whether AI-segment revenue at leading companies maintains its growth rate in the next quarterly earnings cycle, or begins to slow. This is the most decisive indicator.

Second, whether subsequent AI chip IPOs sustain first-day gains. Cerebras's 68.3% debut represents the current ceiling of expectations; future listings will find that level difficult to match. If the next wave disappoints, market sentiment will recalibrate.

Third, how the case-by-case H200 licensing process for China actually functions in practice. If approvals flow smoothly, it is a constructive signal for Nvidia and the broader sector. If disputes arise or the process tightens again, the reopening trend can reverse.

When these three signals align positively, the case for a fundamentally supported rally holds. When at least two turn, a meaningful correction becomes a scenario worth pricing in — even though the long-term thesis of a multi-competitor AI chip market remains structurally intact.