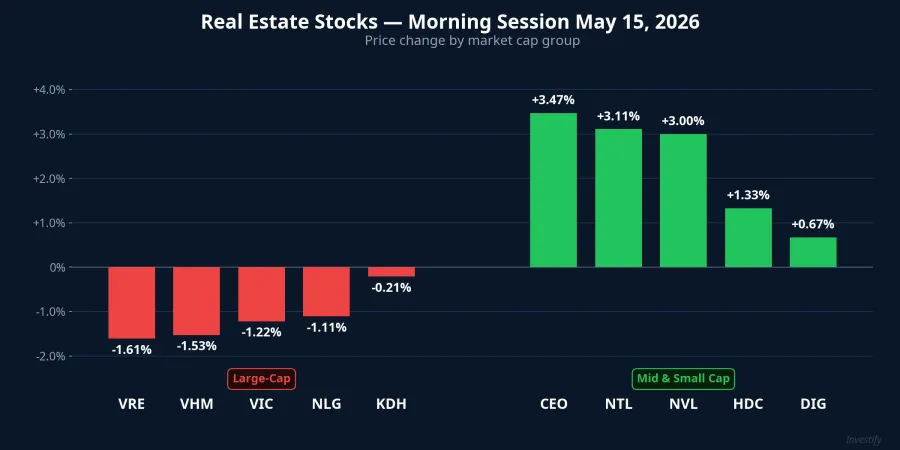

In the morning session of May 15, VN-Index stood at 1,921.98 points — just 3.48 points below the all-time high of 1,925.46 set the previous day. The headline index looked calm. Beneath the surface, the real estate sector split into two opposing streams: VHM dropped 1.53%, VRE fell 1.61%, and VIC slipped 1.22%, while CEO gained 3.47%, NTL rose 3.11%, and NVL added 3.00%. Same sector, same morning, two completely different stories.

The large-cap declines are textbook profit-taking after a strong prior session: VHM had surged 2.95% on May 14, VIC had rallied 3.98%. A segment of retail investors cashed out. The mid and small-cap names are a different story entirely. CEO, NTL, NVL, HDC, and DIG were climbing while the broader market held steady. What separates the two groups is not sector sentiment. It is a very specific question: where exactly is each company's land bank on HCMC's infrastructure map?

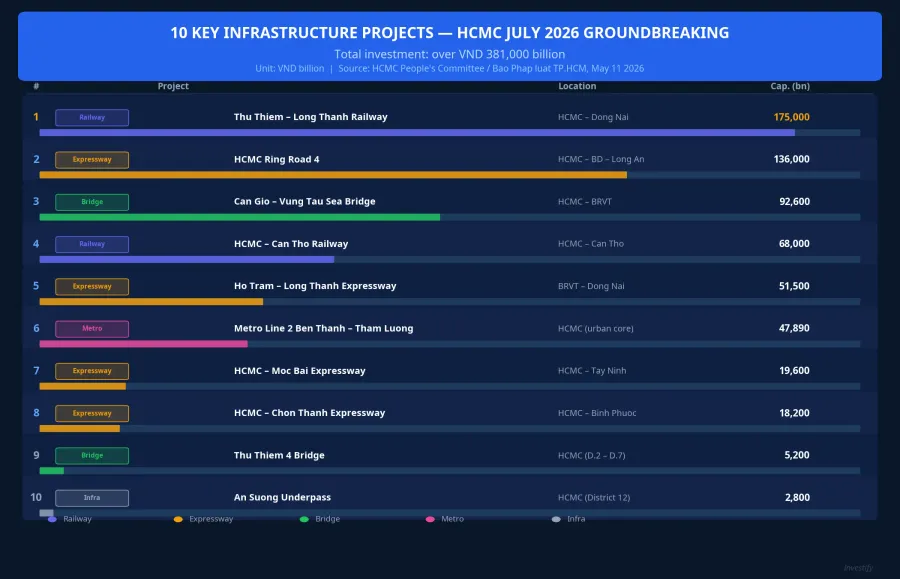

The VND 381,000bn Pipeline and Its Seven-Week Deadline

On May 11, Báo Pháp luật TP.HCM published a list of 10 priority projects for HCMC to break ground in July 2026, with total investment exceeding VND 381,000 billion.Pháp luật TP.HCM Trần Lưu Quang, Secretary of the Ho Chi Minh City Party Committee, had previously stated that the city would launch a series of projects worth over USD 10 billion in July 2026.Báo Mới

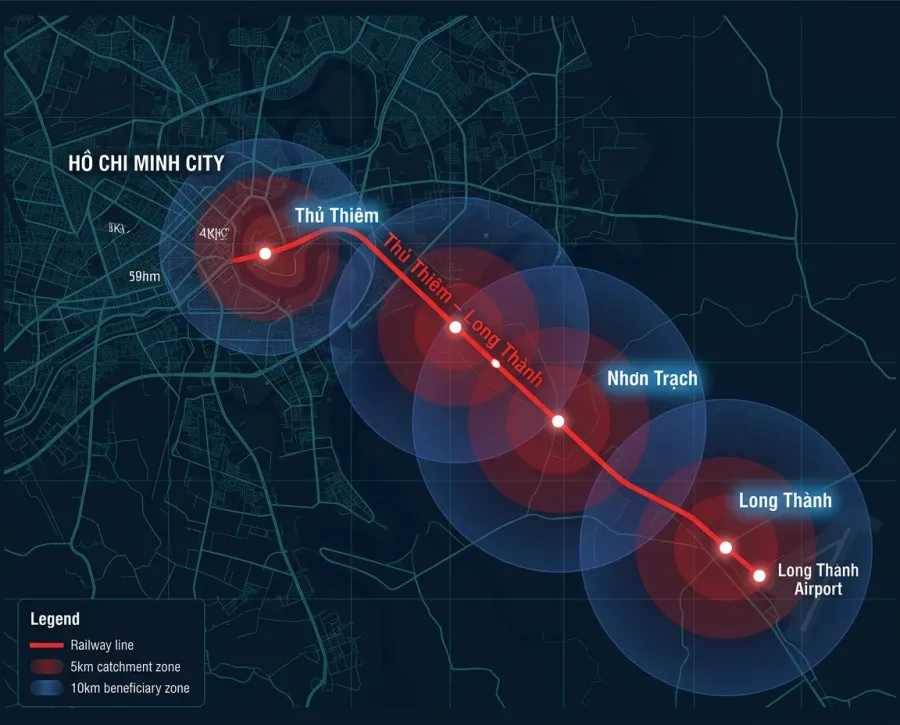

Three of the largest projects sit along the city's southeastern corridor. The Thu Thiem – Long Thanh railway spans approximately 47.7km with around 19 stations, with total investment estimated at over VND 175,000 billion; the HCMC People's Committee has required groundbreaking before July 2, 2026 under a PPP-BT arrangement.VietnamPlus The Can Gio – Ba Ria – Vung Tau sea crossing bridge, over 14km long, carries a price tag of more than VND 92,600 billion under the same PPP-BT model. The Ho Tram – Long Thanh urban expressway, 42km with six lanes, is budgeted at over VND 51,500 billion.

What distinguishes this announcement from previous infrastructure news cycles is not scale. It is the hard legal deadline. "Before July 2, 2026" means roughly seven weeks away. When the groundbreaking date is locked in by a specific government directive, institutional money has a concrete basis to start repricing land bank values based on proximity to each line, rather than simply waiting and watching.

The Mechanism: Why Infrastructure News Moves Stocks Immediately

The actual revenue from a real estate project along a new infrastructure corridor typically takes 3 to 5 years from groundbreaking to appear in financial statements. Yet stock prices react on the same day. Why?

The first mechanism is NAV-based expectation pricing. Land without infrastructure access is valued at agricultural or low-grade urban land prices. Once a railway or expressway groundbreaking is confirmed, land values within the affected radius are revised upward to reflect a new urban baseline — sometimes by a multiple. That upward revision flows directly into the estimated NAV of companies holding the land, driving the target P/B ratio the market assigns.

The second mechanism is cost of capital. Companies with projects near new infrastructure corridors can raise bonds and bank loans on better terms, because the collateral is revalued upward. DIC Corp, for example, holds the 332-hectare Long Tan project in Nhon Trac. With the railway line through Nhon Trac confirmed, the collateral value of the entire project rises, expanding the company's financing headroom.

Real Divergence: Two Filters That Determine Actual Benefit

Not all real estate stocks benefit equally. Two filters determine actual exposure.

The geographic filter. The Thu Thiem – Long Thanh railway corridor runs through eastern HCMC (Thu Duc City, the Binh Trung – Cat Lai area) and the Long Thanh – Nhon Trac zone in Dong Nai. Three developer groups have land banks with direct exposure to this corridor: KDH, NLG, and DIG.

Khang Dien (KDH) holds approximately 40 hectares in the Binh Trung – Cat Lai area and over 500–600 hectares of land bank across Thu Duc, Binh Tan, and Binh Chanh,TechProfit much of it within proximity of the railway alignment. Nam Long (NLG) has the 45-hectare Nam Long Dai Phuoc project in Nhon Trac and the approximately 170-hectare Nam Long Waterfront in Dong Nai.Nam Long DIC Corp (DIG) holds the 332-hectare Long Tan site in Nhon Trac. These three have geographically direct positions along the new corridor.

Companies whose land banks sit primarily in the western or southern parts of the city do not receive direct benefit from the eastern corridor. Price moves in those stocks during this session reflect sector-wide sentiment, not any grounded expectation repricing.

The legal readiness filter. A land bank only converts to revenue once it clears all permitting hurdles: investment approval, detailed 1/500 planning, construction permits, and the right to raise capital from buyers. Developers with clean legal documentation can launch sales as soon as infrastructure rolls out. Developers still working through permitting will see their land values rise on paper, but that increase will not translate into cash flow within the next one to two years. This is the dividing line between "real beneficiary" and "beneficiary on paper."

The Expectation Trap: Infrastructure Arrives First, Revenue Comes Years Later

Today's price moves represent expectation pricing, not realized profit. The gap from groundbreaking to revenue recognition in real estate financial statements typically spans 3 to 5 years: approximately 12 to 18 months for land clearance along the relevant segment, another 12 to 24 months to secure all permits for the adjacent residential or commercial sub-projects, and a further 6 to 12 months from launch to conditions enabling handover and recognition.

Each delay in that window — slow PPP disbursement, compensation disputes, changes to investment policy — can push the timeline back by another 6 to 12 months. The metro line from Ben Thanh to Suoi Tien is the longest-running illustration: groundbreaking in 2012, commercial operations beginning late 2024, more than 12 years from the first shovel.

The Thu Thiem – Long Thanh railway has a groundbreaking deadline, not an operations deadline. Today's expectation is being priced in; the actual revenue will arrive toward the end of this decade, assuming no major schedule slippage.

Four Questions Before Taking a Position

The divergence in the real estate basket this morning reflects the market reading each name individually rather than buying the whole sector on the news. Four questions help assess how much a specific company actually benefits:

First, does the company's land bank sit within 5 to 10 kilometers of a specific railway station or expressway interchange? A province name is not precise enough for valuation; the detailed planning map with specific coordinates is what matters.

Second, how far along is the permitting process for that land? Construction permits issued and conditions met for raising capital from buyers, or still at the investment approval stage?

Third, where is the company in its debt cycle? Large bond maturities in the next 6 to 12 months could force asset sales before the land bank has time to be revalued at the new infrastructure baseline.

Fourth, how much of the infrastructure expectation is already in the price? A P/B ratio above 2x at groundbreaking time typically has most of the upside priced in. A P/B below 1x on a project with clean permits still offers meaningful room for revaluation.

Key signals to watch in the coming week: HCMC authorities releasing specific progress timelines for each project, any PPP tender outcomes, and whether capital flows into the mid and small-cap names with direct eastern-corridor land positions sustain beyond today's session.