On May 13, 2026, Washington delivered two events within hours of each other. They were causally unrelated, but they converged on the same question every financial market is waiting to answer: where will U.S. interest rates go over the next six months?

That morning, the Senate confirmed Kevin Warsh, Chair of the Federal Reserve, with a 54-45 vote, the narrowest confirmation margin in the Fed's modern era. Senator John Fetterman (Democrat, Pennsylvania) was the sole Democratic senator to vote in favor. President Donald Trump had nominated Warsh with the expectation that the Fed would be more flexible about cutting rates than former Chair Jerome Powell.CNBC

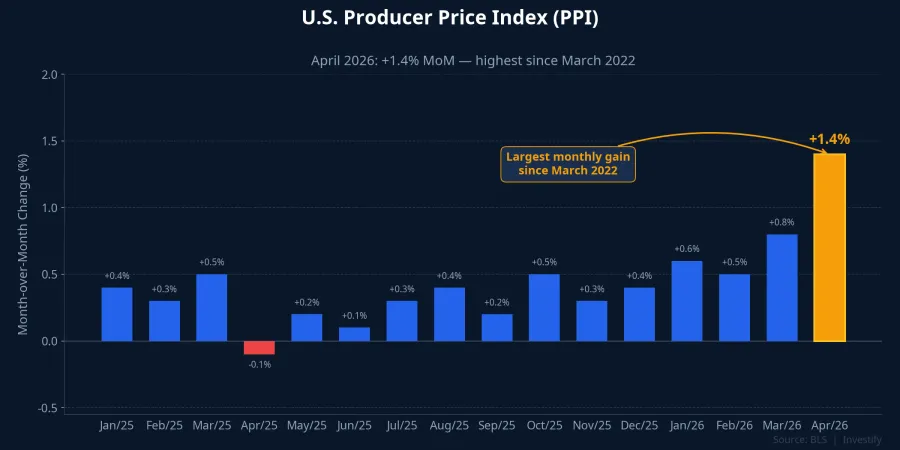

Hours later, the Bureau of Labor Statistics published the April Producer Price Index: headline PPI rose 1.4% month-over-month, nearly three times the Dow Jones consensus forecast of 0.5% and the largest monthly gain since March 2022. The 10-year U.S. Treasury yield jumped to 4.48%, its highest level since July 2025.Yahoo Finance

The bigger picture is taking shape in an uncomfortable direction: Warsh inherits a Fed where the data was already steering before he arrived. The question is not who occupies the Chair. What matters is what the numbers in the driver's seat will do next.

April PPI: An Energy Shock, Not Broad Inflation

Looking beneath the April PPI headline, this was not inflation spreading across all sectors. Roughly three-quarters of the goods price increase came from energy, with energy prices up 7.8% and wholesale gasoline surging 15.6%. Iran-related tensions pushed supply chain stress into the oil complex, lifting pump prices at U.S. gas stations above USD 4 per gallon.CNBC

In standard monetary theory, an energy supply shock is typically viewed as "transitory," meaning it does not require a sharp policy response. That framing would allow the Fed to look through a single hot PPI print without adjusting rates. But core PPI (excluding food and energy) also beat expectations in April, and this marks the second consecutive month in which both CPI and PPI have surprised to the upside. When headline and core measures from consecutive months all exceed forecasts, the "transitory" narrative becomes harder to defend.

That is the central dilemma Warsh faces from his very first FOMC meeting: frame the energy shock as temporary and preserve room for rate cuts, or acknowledge that inflation is re-forming and protect long-run credibility.

Kevin Warsh: More Complicated Than a Simple Hawk Label

Classifying Warsh as simply hawkish or dovish yields no clean answer. During his first term on the Fed's Board of Governors (2006–2011), he was considered a policy hawk who prioritized inflation control and leaned toward tighter monetary conditions relative to his peers.Motley Fool

In more recent comments, Warsh has argued that AI-driven productivity gains can structurally restrain price pressures, providing a theoretical framework for lower interest rates. His confirmation hearing revealed an approach to inflation that acknowledges three competing forces acting simultaneously: AI productivity gains, tariff pressure, and energy price shocks.Council on Foreign Relations

Deutsche Bank noted: "While Warsh has made the case for lower rates, we do not consider him a structural dove. His orientation remains hawkish relative to the broader FOMC." The gap between President Trump's expectations and Warsh's professional track record is precisely the gap that the June 16–17 FOMC meeting will begin to close.

Markets Repriced Before the FOMC Even Met

No one needed to wait for the FOMC. Derivatives markets acted the same day. Per CME FedWatch data, the implied probability of the Fed hiking rates at least once by December 2026 jumped to approximately 36%, up from 16% a week earlier and just 2% a month prior. An 18-fold rise in one month reflects a significant shift in rate expectations.CNBC

The scenario of rate cuts in the first half of 2026 — which President Trump had been counting on — is no longer the base case in futures pricing. The market question has shifted from "how many cuts will the Fed deliver?" to "does the Fed need to hike in 2026?" That is a meaningful rotation in consensus, occurring within a single month.

Three Transmission Channels Into Vietnam's Market

If the Fed is forced to keep rates elevated longer, three transmission channels into Vietnam were already visible in the May 13 session.

Exchange rate. The USD/VND central rate stood at VND 25,123 on May 13, while the commercial bank selling rate was VND 26,379, approaching the ±5% intervention band ceiling.GiaVang.net U.S. 10-year yields at 4.48% widen the USD-VND interest rate differential, reinforcing sustained upward pressure on the dollar in the second half of the year. With the rate already approaching the ceiling, the buffer available to absorb further external shocks is shrinking.

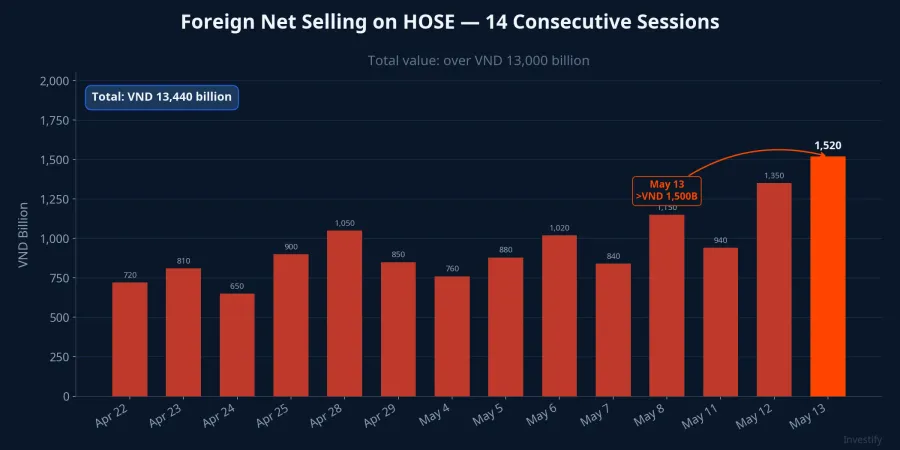

Foreign capital flows. Foreign investors sold net for the 14th consecutive session on HOSE, with total net outflows exceeding VND 13,000 billion.CafeF On May 13 alone, net selling exceeded VND 1,500 billion, concentrated in FPT (VND 380 billion), ACB (VND 260 billion), VHM (VND 243 billion), and STB (VND 193 billion). One notable counterpoint: foreign investors simultaneously bought net VND 545 billion in MSB, suggesting capital is reallocating selectively by stock-specific thesis rather than making a blanket exit from Vietnam.CafeF

Domestic interest rates. The VN-Index closed May 13 at 1,898.37 points, down 2.73 points and slipping below the 1,900 level. With U.S. yields near 4.48% and the dong exchange rate pressing against its ceiling, the State Bank of Vietnam's room to cut its policy rate further is meaningfully constrained. Additional rate cuts at this juncture would widen the USD-VND yield differential further, directly amplifying the pressure for foreign capital outflows.

Three Questions the June 16–17 FOMC Will Answer

The June 16–17 FOMC meeting is Warsh's inaugural session as Chair, and markets will parse every word of the statement and press conference. Three concrete questions are worth tracking: whether the statement language still leaves open the possibility of second-half rate cuts, or pivots to fully neutral; whether FOMC members' rate forecasts (the dot plot) shift upward following two months of above-estimate CPI and PPI; and how Warsh frames the energy shock in the press conference, whether as transitory to preserve policy flexibility or as evidence of re-forming inflation to protect long-run credibility.

For Vietnamese investors, three signals to monitor over the next four weeks are: whether the U.S. 10-year yield holds above 4.4%, whether the central USD/VND rate breaks above VND 25,150, and whether the foreign net-selling streak extends past 15 consecutive sessions. If all three signals deteriorate together, the second-half capital flow scenario needs to be revised. If all three improve, the narrative of a more accommodative Fed under Warsh remains alive.

The bigger picture: when the PPI hits a four-year high on the exact day a new Fed Chair is confirmed, the expectation that "Warsh will cut rates early" needs to be weighed against the reality that incoming data is rewriting the script faster than any individual in the room.