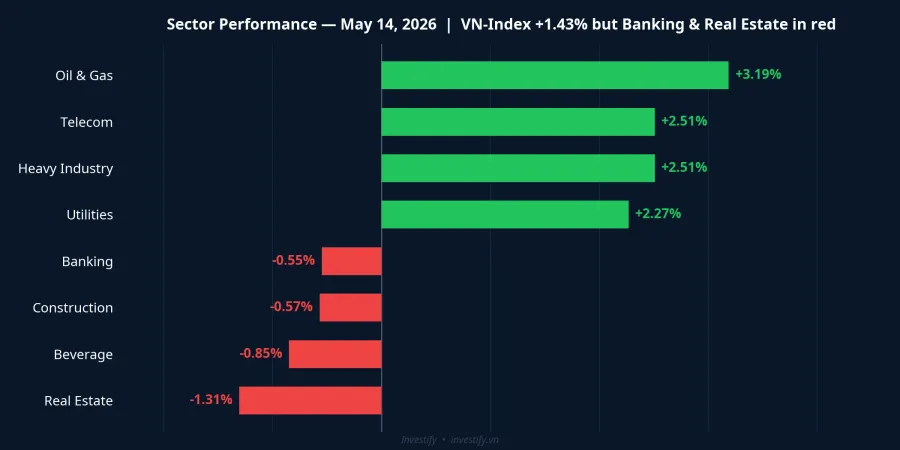

On May 14, 2026, VN-Index closed at 1,925.46 points, up 27.09 points (+1.43%), setting a new all-time high above the previous record of 1,915.37 set on May 8.Báo Mới But the most telling number was not the index itself, it was the internal structure: 134 stocks fell against 166 that rose, and the two sectors with the largest weighting in most retail portfolios, banking (-0.55%) and real estate (-1.31%), both closed in the red. Foreign investors net-sold over VND 410 billion in the very session that set the record.VnEconomy The big picture shows this was a narrow peak pulled up by a small group, not a broad-based rally.

Oil Surged on Brent, Not on Domestic Fundamentals

The oil and gas sector rose 3.19%, leading all sectors on May 14, pulling heavy industry, telecoms, and utilities along with it. To understand this move, you have to look beyond Vietnam's borders.

Brent crude closed at USD 105.97 per barrel on May 14. Compared with USD 100.06 on May 7, the weekly gain was 5.9%. Compared with the roughly USD 95 level at the start of April, Brent had climbed more than 11% in less than six weeks. The key driver was the escalation at the Strait of Hormuz: Iran deployed hundreds of attack boats to the area, and the United States launched a commercial vessel escort operation called "Operation Project Freedom" starting May 4.Al Jazeera With a large share of global oil flows passing through the strait placed under threat, markets responded by pricing in a geopolitical risk premium immediately.

Brent in the USD 100–110 range feeds into Vietnamese oil company earnings through three distinct channels. The first is upstream: GAS's natural gas revenues are directly benchmarked to world oil prices via the formula for sales to EVN and thermal power plants; PVS benefits from a higher-oil-price environment that pushes PetroVietnam to increase exploration budgets and advance new field developments like Block B and Lac Da Vang. PVD is more insulated because drilling contracts are typically fixed 6–12 months ahead, so cash flow benefits come with a lag. The second channel is refining: BSR's refining margins expand when refined product prices rise faster than crude input costs. BSR's market capitalization grew from approximately VND 129,900 billion on May 8 to VND 151,700 billion on May 14, a gain of 16.8% in just five sessions.Vietstock The third channel is geopolitical hedging: when Hormuz heats up, part of the market rotates into assets causally linked to oil prices as a way to protect the rest of a portfolio from energy-cost volatility.

That said, flows were not uniform within the sector. On May 14, GAS rose 3.06% to VND 84,300, while PVD fell 2.95% to VND 32,900 and PVS dropped 1.22% to VND 40,500. Both PVD and PVS had already surged the session before: PVD +6.44%, PVS +2.50%. The money in oil on the peak session concentrated in GAS and BSR, not across the whole group. This is a caution signal for investors considering a late entry into the sector after the run-up.

Banks Fell on Funding Costs, Not Asset Quality

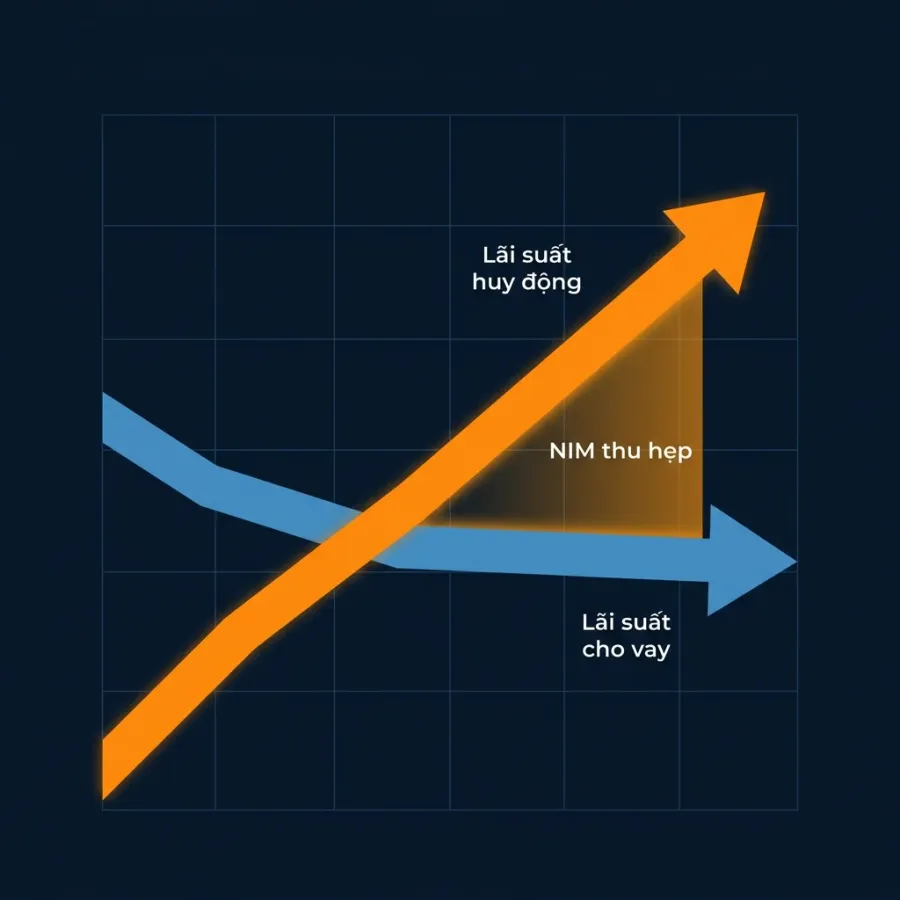

Banking declined 0.55% on May 14. A modest move in isolation, but notable when placed alongside an index at an all-time high. The pressure comes from a funding-cost problem, not from concerns about non-performing loans or liquidity risk.

Loan growth is running faster than deposit growth, creating direct downward pressure on net interest margins (NIM) across the system.SSI Research The mechanism operates through three consecutive layers. The first: starting in 2026, Treasury deposits are no longer counted in the denominator when calculating the loan-to-deposit ratio (LDR).Nguoi Quan Sat State-owned banks Vietcombank, BIDV, and VietinBank are hit hardest because they have historically held the largest Treasury deposit balances; to keep LDR below the 85% cap, they are now compelled to raise term deposit rates to attract retail savings, pushing up funding costs in the process.

The second layer: when loan growth outpaces deposit growth for several months, banks must plug the gap by issuing debt instruments or borrowing in the interbank market. Both are more expensive than low-cost retail demand deposits, pulling average funding costs higher. The third layer: lending rates are very hard to raise at the same speed. Corporates are in the early stages of recovery with limited tolerance for higher borrowing costs, so banks cannot simply pass the expense through to borrowers. The gap between rising funding costs and sticky lending rates is precisely the NIM compression the market is pricing in now, ahead of the Q2 results season.

Real Estate Faces a Double Squeeze on Credit and Mortgage Rates

Real estate fell 1.31% on May 14, the steepest decline among all 18 tracked sectors. Three independent sources of pressure converged on the group simultaneously.

The first is a structural shift in credit allocation. Q1 2026 data shows construction and project-deployment credit grew 67% year-over-year, while credit to property developers rose only 21%.StockBiz Bank money is flowing to contractors, not to the developers who own listed shares. The direct consequence is that revenues and cash flows at listed developers are growing more slowly than aggregate sector credit data would suggest, blurring the recovery narrative.

The second pressure point is mortgage rates remaining elevated. With bank funding costs rising as described above, preferential home-loan packages have little room to drop further. Slow housing demand recovery becomes a direct drag on developer revenues and profits. The third factor is profit-taking after a strong run. When VN-Index reaches an all-time high, rotation out of high-performing positions is a natural response; many listed real estate stocks have gained 30–40% since the start of the year, making them primary targets for profit-taking when the index touches technical peak territory.

Three Signals to Watch Over the Coming Week

Whether the May 14 sector divergence is temporary or structural will become clear from three indicators in the next one to two weeks.

The first is Brent. If oil stays above USD 100 over the coming week, the oil sector's rally has a solid support floor. The decisive variable remains the Hormuz situation. Any constructive signal from US-Iran negotiations could pull Brent back below USD 100 quickly, extinguishing the sector's tailwind.

The second is the 12-month term deposit rate at the Big 4 state banks. If state-owned banks continue raising deposit rates in May, NIM compression will extend at minimum through Q3. Investors holding banking stocks should consider waiting for Q2 results before making further moves.

The third is foreign investor flow. Net sales of over VND 410 billion on the peak session itself are a clear caution signal. If sustained net selling continues over the next several sessions, VN-Index will struggle to hold above 1,920 points. Sectors with the highest foreign ownership concentration, primarily banking and listed real estate, are historically where selling pressure surfaces first when foreign investors reduce exposure.

May 14 shows two markets running in parallel inside the same index: an oil sector gaining from global geopolitics, and a large-cap base of banking and real estate stocks under structural pressure from funding costs and credit allocation shifts. An index all-time high is not necessarily a portfolio all-time high. The right question to ask is not where the index goes next, but which side of this divergence your current holdings sit on.