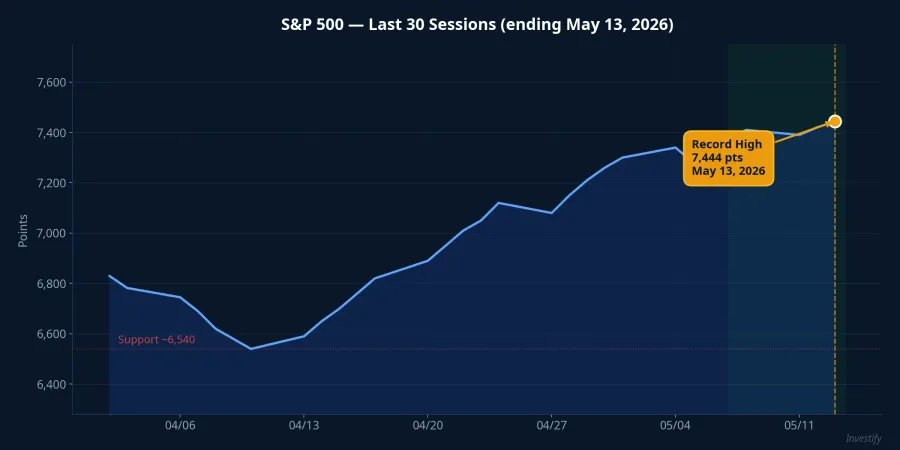

On the evening of May 13, 2026, the S&P 500 closed at 7,444.25 points, setting a new all-time high.Sherwood News That same evening, U.S. President Donald Trump landed in Beijing with a heavyweight business delegation: Jensen Huang, CEO of Nvidia Corporation; Tim Cook, CEO of Apple Inc.; Elon Musk, CEO of Tesla Inc.; and Kelly Ortberg, CEO of Boeing.EconCurrents Wall Street celebrated for an obvious reason: if the U.S. and China can ease tensions over AI chips and market access, revenue at the largest S&P 500 companies could unlock a door that has been shut since 2023.

The natural inference from here: Wall Street rallies, risk appetite rises, Vietnamese export stocks are worth buying. That logic holds at one level. The problem is that it conflates two export groups with fundamentally opposite benefit mechanisms. The larger picture is worth understanding clearly before placing orders.

Group 1: Direct Exporters to the U.S.

Seafood, textiles, and wood products are the group that sells consumer goods directly to American buyers. They are the most directly affected by U.S. tariff policy. Since August 2025, Vietnamese goods entering the U.S. have been subject to a 20% tariff under a bilateral trade framework.TLD Apparel Though the legal basis of these tariffs has continued to evolve following the U.S. Supreme Court's February 2026 ruling, the textile and seafood sectors still face tariff pressure and ongoing Section 301 investigations.

The scale of market dependence is substantial. Vietnamese textiles exported USD 17.6 billion to the U.S. in 2024, representing approximately 40% of total national textile exports.TLD Apparel The U.S. is the single largest market for many of Vietnam's key export categories. Any shift in the tariff structure will transmit directly to corporate margins.

Vinh Hoan (VHC) is the clearest example. The stock closed the May 13 session at VND 61,200 per share, with 2024 revenue reaching VND 12,510 billion, up 24.72% year-over-year, and holding approximately 14% of national pangasius export market share.LinkedIn The U.S. is VHC's largest market. Also on May 13: Minh Phu (MPC) closed at VND 16,100, down 2.42%; Song Hong Garment (MSH) held flat at VND 36,100; TNG rose 2.59% to VND 19,800.

The benefit mechanism for this group depends on the relative tariff differential between Vietnamese and Chinese goods in the U.S. market. Chinese goods currently face significantly higher tariffs in the U.S. than Vietnamese goods across many product categories. That differential is the core reason American buyers have been shifting orders from China to Vietnam in recent years. If the Trump-Xi talks lead to the U.S. reducing tariffs on Chinese goods while keeping current rates on Vietnam, the relative gap narrows and Vietnam's competitive advantage erodes. If both are cut by the same proportion, Vietnam retains its absolute advantage but must compete for market share with China again.

Group 2: FDI Electronics Assembly

Trump's delegation did not fly to Beijing to negotiate over shrimp or garments. They came for AI chips, iPhones, and electric vehicles. This is the key point that investors risk overlooking.

Jensen Huang wants to expand the list of approved Chinese customers for the H200, following U.S. policy that already permitted H200 sales to vetted Chinese buyers with a 25% import tariff attached.CNBC Tim Cook wants to stabilize access to the Chinese market and component supply chains for assembly operations based in Vietnam and India. Elon Musk has the Gigafactory in Shanghai and depends on Chinese EV market access.

The core issue lies in the structure of the electronics supply chain in Vietnam. Samsung places over 50% of its global smartphone output at factories in Bac Ninh and Thai Nguyen, with Foxconn-Apple following the same trajectory.Vietnam Briefing Yet the actual localization rate remains low: only 35 to 39 Vietnamese firms are Tier 1 suppliers to Samsung out of approximately 340 suppliers in the chain, and most provide consumables, packaging, and printing services. Vietnam's electronics chain is essentially a final-assembly chain, not a high-value-added manufacturing chain.

The consequence is this: if the U.S. allows Apple and Nvidia to return to China more freely — AI chips selling, components moving again — the economic rationale for maintaining or expanding assembly operations in Vietnam weakens. Capital flows have shifted because of U.S.-China geopolitical pressure. If that pressure eases, part of those flows could reverse. This is not a prediction — it is a mechanism documented in supply chain structure reports.

What the 2020 Phase 1 Deal Tells Us

In January 2020, President Trump and then-Vice Premier of China Liu He signed the Phase 1 Trade Agreement, under which China committed to purchase an additional USD 200 billion of U.S. goods over two years.CSIS The outcome: China fulfilled only approximately 40% of its commitment, partly due to Covid. More importantly for Vietnam, that agreement did not reduce Section 301 tariffs on Chinese goods. The economic rationale for shifting production to Vietnam remained intact. Vietnam's share of global consumer electronics exports rose from 8.3% in 2017 to 10.4% in 2023 in that context.Rhodium Group

The current round of talks differs in a critical way: the focus is AI chips and technology market access, not agricultural or consumer goods purchases. If the U.S. eases technology controls on China and China opens its consumer market to Apple and Tesla, the first beneficiaries will be S&P 500 companies, not Vietnam-based assembly chains. That is why a Wall Street record high and structural pressure on FDI electronics stocks can coexist, even as consumer export stocks receive short-term sentiment support.

Signals to Watch Over the Coming Days

The more accurate picture for Vietnamese investors is not "trade war cooling = buy export stocks." Distinguishing by supply chain position is the right framework.

Direct exporters to the U.S. are receiving short-term sentiment support, but their long-term trajectory depends on the relative tariff differential between the U.S. and China. FDI electronics assemblers are absorbing structural uncertainty: even if share prices rise during a risk-on session, the foundation of their supply chain advantage may be eroded by the very negotiations taking place.

Two concrete signals deserve monitoring over the next 24 to 72 hours: first, any official announcement expanding the list of approved Chinese customers for Nvidia's H200; and second, any movement on the tariff structure for Vietnamese goods within the bilateral negotiation framework. Both could shift market direction within this week.

The VN-Index closed the May 13 session at 1,898.37 points. A Wall Street record is good news for market sentiment. But sentiment is one layer, and supply chain mechanics is another. Those two layers are currently pointing in different directions depending on which group of stocks you hold.