On the morning of 14 May 2026, Vietnam's Ministry of Industry and Trade (MoIT) published the third draft of amendments to Decree 72/2025/NĐ-CP governing the mechanism for adjusting average retail electricity tariffs.Thanh Niên The headline provision proposes two options for recovering EVN's accumulated VND 44,792 billion loss through phased tariff adjustments over future rate-setting periods, avoiding a single large price shock.VnExpress This remains a draft under public consultation, not yet an enacted decree. Even so, it is specific enough for investors to review their exposure across the three most electricity-intensive listed sectors: chemicals, cement, and steel.

Two Options That Differ in Scope, Not Speed

The easiest misreading of this draft is to assume the two options simply differ in how quickly losses are passed through. A closer reading shows the real distinction lies in the scope of future applicability.

Option 1 allows cost recovery for the portion of 2022 and 2023 production and distribution costs not yet reflected in average retail tariffs, and continues applying the mechanism in subsequent years if EVN incurs similar losses again.Thanh Niên This is an open-ended mechanism with no fixed end point.

Option 2 applies only to costs not yet recovered from 2022 until the date the amended decree takes effect. Beyond that point, the mechanism does not apply if new losses emerge. This is a one-time, closed mechanism.Thanh Niên

Both options require that loss recovery be spread across multiple tariff adjustment cycles, in small increments to limit the impact on consumers and businesses. The substantive policy question is whether the government wants a standing tool for managing future EVN losses, or simply a one-off resolution for this cycle. The answer will become clear once MoIT submits a final option to the government for approval.

How the VND 44,792 Billion Loss Was Built Up

EVN's combined losses in 2022 and 2023 totalled approximately VND 50,029 billion.Thanh Niên The primary cause was a sharp spike in the cost of imported coal and natural gas following the Russia–Ukraine conflict, while retail electricity tariffs were held flat for an extended period to support post-pandemic economic recovery. The gap between input costs and revenues accumulated on EVN's balance sheet.

In 2024, EVN returned to profitability as fuel prices eased and two tariff increases were implemented. This reduced the parent company's accumulated loss to VND 44,792 billion by the end of 2024.NLĐ That remaining balance is what the current draft proposes to recover through future tariff cycles. It is worth noting this figure applies to EVN's parent entity, covering transmission and distribution operations, and excludes certain subsidiary results.

Chemicals, Cement, Steel: Three Different Stories

The impact of an electricity price increase on listed companies depends on two independent variables: electricity cost intensity as a share of total production cost, and the gross margin available to absorb the incremental cost. These two variables do not move together, which is why the same policy shock creates three different exposure profiles across three sectors.

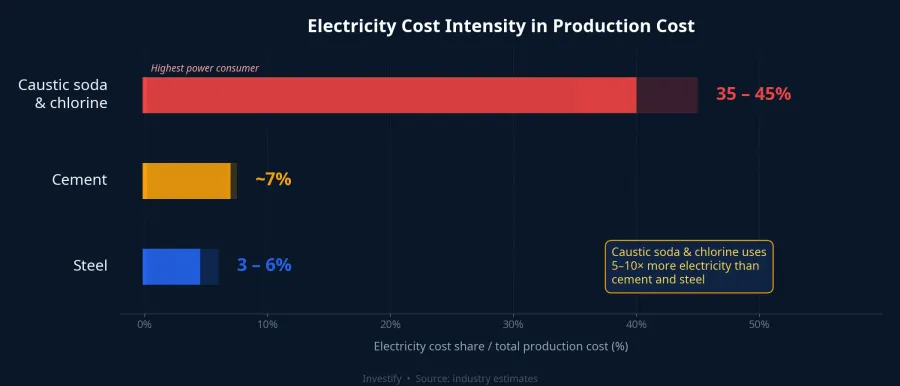

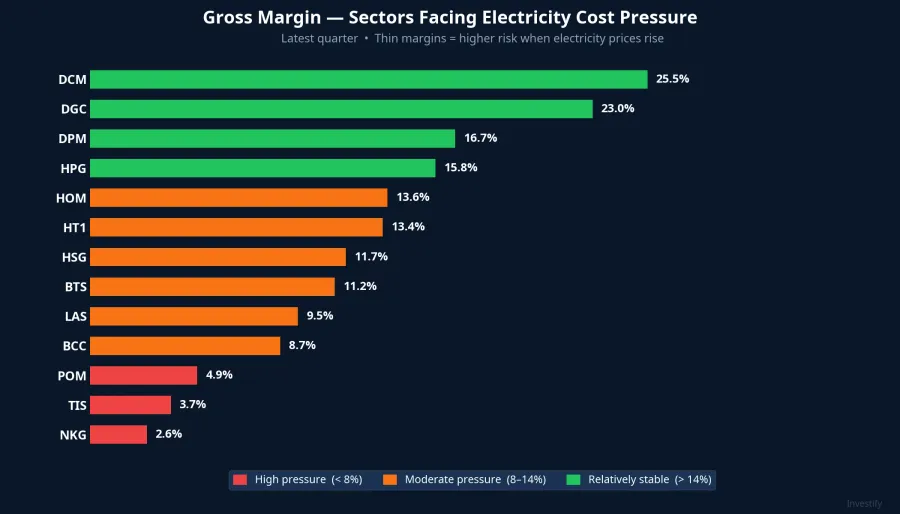

Chemicals, particularly the caustic soda and chlorine segment, carry the highest electricity cost intensity: approximately 35 to 45% of production cost for electrolytic producers.VnExpress This is five to ten times higher than cement. DGC trades around VND 50,800 with a gross margin of approximately 23%; DCM is at VND 43,850 with a margin of 25.5%; DPM at VND 27,200 with a margin of 16.7%. LAS has a thinner margin of around 9.5%. The relatively wide margins in this group provide a buffer, but the high starting exposure means that even a modest tariff increase translates into a meaningful absolute hit to earnings.

Cement carries far lower electricity cost intensity: approximately 7% of production cost by industry estimates.VnExpress The problem lies in margin structure. The sector has been operating under intense price competition and oversupply, keeping gross margins thin across most listed names. HT1 sits at 13.4%, HOM at 13.6%, BTS at 11.2%, BCC at just 8.7%. With margins this slim, even a small percentage increase in electricity costs leaves a visible mark on quarterly results.

Steel is the most differentiated of the three groups. HPG self-generates approximately 90% of the electricity consumed at its Dung Quat integrated complex, meaning direct exposure to commercial grid price increases is minimal. HPG trades around VND 27,200 with a gross margin of 15.8%, placing it comfortably in the buffer zone. In contrast, steel roofing and construction steel companies without captive power — HSG (11.7%), NKG (2.6%), POM (4.9%), TIS (3.7%) — operate on very thin margins. Any increase in input costs, however small, risks pushing results to breakeven or loss territory.

The summary picture: chemicals face the highest intensity shock but carry margin to absorb it; cement faces a smaller intensity shock but has almost no margin cushion; steel is sharply bifurcated between self-generating producers and grid-dependent ones.

Market Reaction in the Session of the Announcement

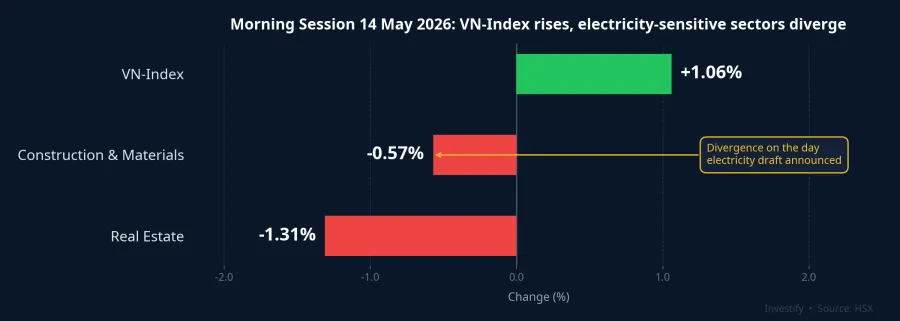

Notably, a divergence appeared in the morning session of 14 May itself. VN-Index stood at 1,918.51 points, gaining 1.06%, while the Construction & Materials sector fell 0.57% and Real Estate dropped 1.31%.HSX

Caution is warranted in interpreting this signal. A single-session divergence is not sufficient evidence that markets are repricing the electricity tariff risk embedded in this draft. Real estate and construction materials are subject to many other short-term influences. Still, the fact that the divergence appeared on the same day as the policy announcement is a data point worth noting in context.

Three Milestones Worth Monitoring

The third draft is currently in its public consultation phase before MoIT submits it to the government. Three policy milestones are worth tracking in sequence:

Milestone 1: MoIT concludes the consultation period and submits a final option — Option 1 or Option 2 — to the government. This choice determines whether the loss-recovery mechanism becomes a recurring tool or a one-time fix.

Milestone 2: The government signs and issues the amended decree, and the date it takes effect. The interval between issuance and effective date directly affects which tariff adjustment cycle first applies the new mechanism.

Milestone 3: The magnitude of the increase in the first average retail electricity tariff adjustment after the decree takes effect. This figure reveals how much of the VND 44,792 billion EVN and MoIT elect to recover in a single cycle, allowing investors to estimate how many cycles the full recovery will require.

What the Numbers Point To

The analytical framework for screening portfolios at this stage is straightforward: check electricity cost intensity against production cost, then check whether the current gross margin is adequate to absorb the incremental exposure.

The highest-risk cohort once the decree is enacted will be names with both thin gross margins and full dependence on the commercial grid. By this framework, NKG (2.6%), TIS (3.7%), and POM (4.9%) in steel are the names deserving the closest watch in coming quarterly results. BCC (8.7%) and LAS (9.5%) in cement and chemicals also sit in the thin-margin category. For these companies, any increase in input costs, however small, has a direct path to earnings.

At the other end, names with wide margins and high captive power generation, such as HPG and DCM, carry meaningful buffers. The risk exists, but it is accompanied by a clear cushion.

The three policy milestones above will progressively clarify the magnitude and pace of tariff increases. That is more actionable information than any forecast made while the draft is still under consultation.