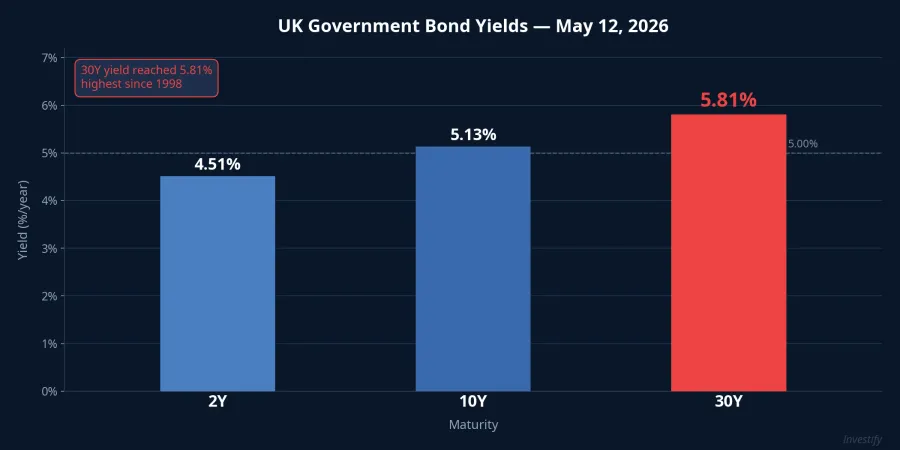

On May 12, 2026, the yield on 30-year UK government bonds (gilts) reached 5.81% per year, the highest level since May 1998.CNBC On the same session, the 10-year yield crossed 5.13%, while the 2-year yield held at roughly 4.51%. Same market, same sell-off. The stress, however, was strikingly uneven across maturities.

The more important question is not which political trigger sparked the sell-off, but why the same shock could push 30-year bonds far harder than 2-year bonds. The answer lies in a metric that many retail investors overlook: portfolio duration.

Why the Long End of the Curve Took the Hit

This week's yield surge traces back to a specific political event. In the UK's early-May local elections, Reform UK won more than 1,450 council seats nationwide.CNBC The result piled pressure on Prime Minister Keir Starmer's Labour government: more than 80 Labour MPs publicly called on him to resign.CNBC

Markets reacted to a specific worry: a new Labour leader might loosen fiscal discipline to win back voters. This matters because the UK's public sector net borrowing has stayed at roughly 5% of GDP for four consecutive years. Any signal of fiscal loosening raises a pointed question: will the next government continue issuing debt at elevated levels, and how much extra yield will long-term bond buyers demand in exchange for that risk?

By May 13, some of the pressure had eased: the 30-year yield pulled back to around 5.74%, the 10-year to 5.07%, and the 2-year remained steady near 4.51%. But the gap between the 30-year and 10-year yields still held around 67 basis points, while the 10-year versus 2-year spread narrowed to 56 basis points. The long end of the curve was clearly repriced more aggressively than the short end. This pattern is no accident.

Duration: The Number That Translates Rate Moves Into Price Changes

Think of duration this way: when you buy a bond, you are lending money and will receive it back in installments — annual coupon payments plus the principal at maturity. Duration measures the weighted-average time until you receive all of those cash flows. Bonds with longer duration are more sensitive to interest rate changes because most of their cash flows sit far in the future. When market rates rise, those distant cash flows are discounted more heavily, pulling the bond's price down more.

The quick estimation rule every investor should know:

%ΔP ≈ −D × Δy

Where D is duration (in years) and Δy is the change in yield (in percentage points). For conventional coupon bonds, the approximate values are:

- 2-year bond: duration roughly 1.9 years.

- 10-year bond: duration roughly 8–9 years.

- 30-year bond: duration roughly 16–18 years, depending on coupon rate and yield level.

Apply that to a 0.5 percentage point yield increase, and the estimated price losses are:

- 2-year bond: falls about 1%.

- 10-year bond: falls about 4–4.5%.

- 30-year bond: falls about 8–9%.

This is why the gilt market's reaction was so clearly tiered by maturity. It is not that investors are worried about fiscal risk in proportion to each bond's tenor. It is that identical yield moves produce vastly different price losses at each point on the curve. A 30-year bond is not "worse" than a 2-year bond; it is simply more sensitive, in the precise mathematical sense.

A necessary caveat: actual duration depends on a bond's coupon rate, market price, and specific cash-flow structure. A zero-coupon 30-year bond has a duration of exactly 30 years; a high-coupon bond has a duration lower than its stated maturity. The approximation above is useful for gauging sensitivity, not for precise pricing.

Vietnam Government Bonds: Same Mechanics, Smaller Swings

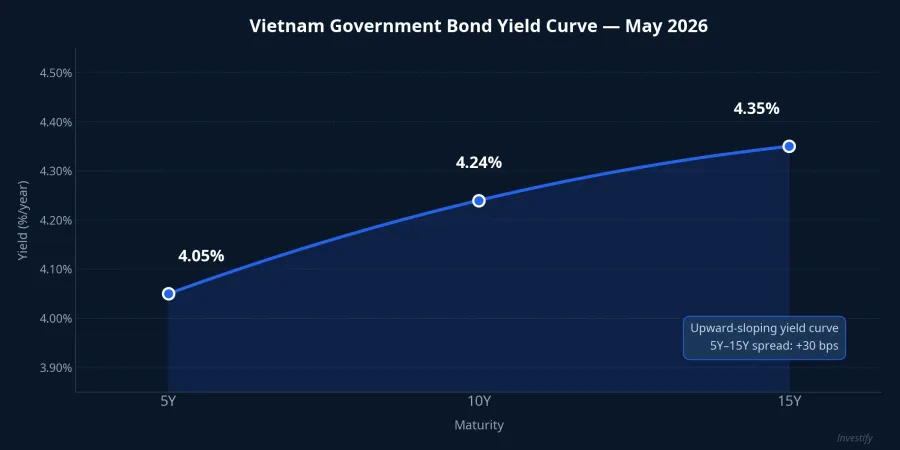

Vietnam's government bond (TPCP) market in May 2026 follows the same pattern, though with much smaller swings in yield. Current secondary-market yields: the 5-year sits around 4.05%, the 10-year around 4.24%, and the 15-year around 4.35%. Compared to late-April auction rates (5-year 3.86%, 10-year 4.16%, 15-year 4.25%), all three tenors have edged higher in May. This is playing out against a backdrop of the State Bank of Vietnam holding its policy rate at 4.5% since March 2026, with March CPI at 4.65% year-on-year.

Vietnam's yield curve slopes upward, with the spread from 5-year to 15-year at roughly 30 basis points. That is far narrower than the 130-basis-point gap across the UK gilt curve (from 2-year to 30-year), reflecting a market with a different risk appetite and fiscal outlook.

The First Question to Ask Before Buying a Bond Fund

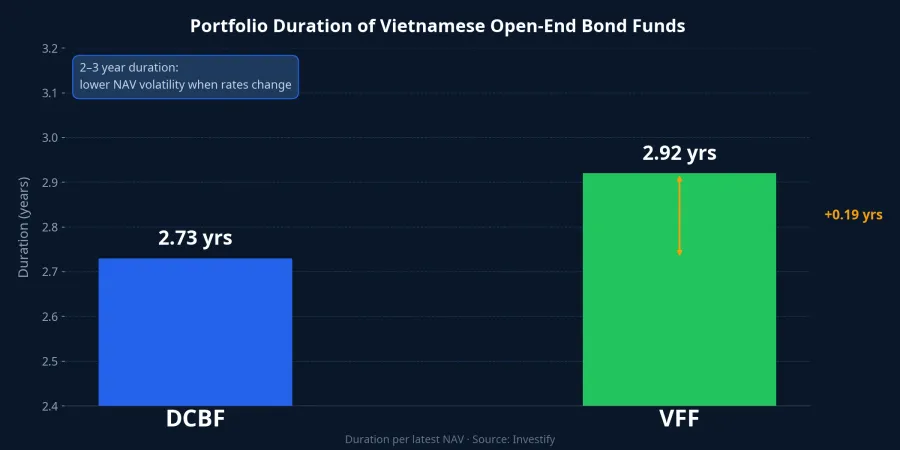

Most Vietnamese retail investors access government bonds through open-end funds rather than direct purchases. That is exactly where portfolio duration becomes highly practical. Based on available portfolio data, the estimated duration of two Vietnamese open-end bond funds is:

- DCBF: approximately 2.73 years.

- VFF: approximately 2.92 years.

A duration of 2–3 years sits in the low-duration range. Applying the estimation rule: if yields rise 0.5 percentage points across the entire curve, these funds' NAVs would move approximately 1.3–1.5%. That is much smaller than a portfolio concentrated in long-duration bonds, and it reflects a deliberate design choice: low duration keeps NAV stable, which suits investors who use bond funds as a capital-preservation layer.

When you read a bond fund's prospectus or a fixed-income product sheet, the average coupon or expected yield is usually the headline figure. That number measures income: it tells you how much you earn. Portfolio duration measures price-change risk: it tells you how much your NAV could fluctuate if rates move. Two very different questions. The second one is almost always skipped.

A practical framework when evaluating bond funds:

- Duration under 3 years: defensive portfolio. NAV fluctuates little when rates change. Best suited to investors who may need to redeem within 12–24 months or who prioritize capital stability.

- Duration 3–7 years: balanced portfolio. Moderate NAV volatility through rate cycles. Appropriate for a 2–4 year horizon with tolerance for some price swings.

- Duration over 7 years: long-duration portfolio. NAV is highly sensitive to rate changes. Offers price appreciation potential when rates fall, but meaningful downside risk when rates rise, exactly as the UK gilt curve illustrated this week.

The UK Lesson, Applied at Home

The May 12 gilt event is not just distant political news. It is a real-world, live-data demonstration of how duration works: the same fiscal-expectation shock left 2-year bonds down less than 1%, while 30-year bonds faced an 8–9% price loss. This mechanism is not unique to the UK. It is the mathematics of bond pricing, and it applies to every portfolio in every market, including Vietnam.

The practical question before buying a bond fund is not "what is the expected yield" but rather "what is the portfolio's duration, and does that match my investment horizon and risk tolerance." For funds such as DCBF and VFF, a duration of 2–3 years signals a design oriented toward NAV stability. What matters is that investors understand what that choice means — not just the yield figure on the cover page.

Key signals to monitor: the direction of UK Labour Party leadership and any resulting fiscal policy shift (which would continue to affect long-dated gilts), Vietnam's own rate cycle and CPI trajectory, and any changes in the portfolio duration of bond funds you currently hold.