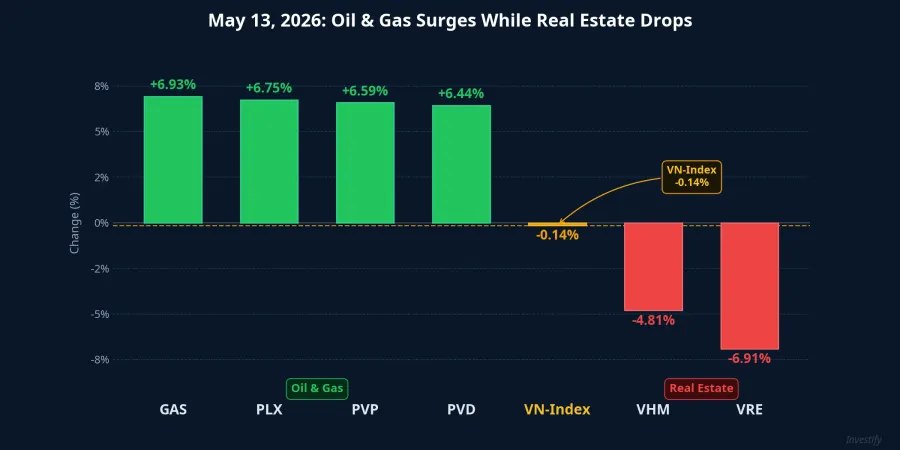

The trading session on May 13, 2026 ended with 176 stocks closing in the red. The VN-Index slipped 0.14% to 1,898.37 points, a quiet session by index standards but one that concealed a striking internal divergence.BaoMoi

Vietnam's four largest oil and gas stocks moved sharply against the index: GAS hit its price ceiling at VND 81,800 (+6.93%), PLX gained 6.75% to VND 40,350, PVP rose 6.59% to VND 19,400, and PVD climbed 6.44% to VND 33,900. GAS alone matched 6.35 million shares — more than three times the previous session's volume — with over 624,000 shares of unmatched buy orders still queued at the ceiling price when trading closed.BaoMoi At the other end, VHM fell 4.81% and VRE dropped 6.91%, becoming the two biggest drags on the index.

The divergence — energy stocks bid up aggressively while real estate sold off — was not random. It reflects how capital is repricing energy sector margins in an environment where Brent crude has been anchored above USD 100, a situation driven by the ongoing blockade of the Strait of Hormuz.

Where Brent Stands and Why Hormuz Is the Key Variable

Brent crude closed at USD 106.62 per barrel on May 13, down a modest 1.06% from the prior session, but the trend over the past four weeks tells a more significant story. From a low of USD 90 on April 17, Brent climbed to a peak of USD 114 on May 4 before pulling back to its current level. It has held continuously above USD 100 since April 21.

The root cause is the Strait of Hormuz. Since early April 2026, the waterway — which carries roughly 20% of the world's crude oil and liquefied natural gas — has been under a two-way blockade: Iran controls the exit routes while the U.S. Navy restricts Iranian port access.VTV A ceasefire holds in name, but the flow of tankers is effectively paralyzed.

On May 11, U.S. President Donald Trump rejected Tehran's latest peace proposal, which had demanded war-cost reparations, recognition of Iranian sovereignty over Hormuz, and full sanctions relief.VietGiaiTri By May 12-13, Tehran set out preconditions before agreeing to resume any nuclear talks.VietnamPlus This is the genuine fork in the road for oil prices and, by extension, for Vietnam's oil and gas sector.

Four Stocks, Four Different Profit Channels

All four stocks moved in the same direction, but they benefit from elevated Brent through entirely different mechanisms. Understanding the distinction matters when sizing positions.

GAS is linked to Brent indirectly through its gas pricing formula. The sale price of gas delivered to power plants and industrial customers is pegged as a percentage of fuel-oil prices, or references the regional LNG benchmark JKM. There is a lag built into the contract cycle, but when Brent stays high long enough, GAS's margins widen meaningfully. After the May 13 session, GAS's market capitalization stood at approximately VND 197,400 billion, making it the largest listed oil and gas stock in Vietnam.

PLX operates on an "inventory profit" model. Domestic retail fuel prices are adjusted periodically based on import costs and a price stabilization fund. When Brent rises over a sustained period, the company earns a margin between lower-cost existing inventory and the higher prevailing sale price. This effect reverses quickly when Brent drops sharply. The 6.75% gain on May 13 with nearly 11 million shares traded suggests capital is pricing in the next retail price adjustment in PLX's favor.

PVD and PVP benefit through an operational channel with no direct link to daily price swings. When Brent is sustained at high levels, regional field operators increase drilling exploration budgets, pushing rig day rates and utilization higher: this is the core driver for PVD. PVP benefits when oil freight rates rise in an environment where shipping routes lengthen or cargo flows shift. Both structures require Brent to hold elevated for multiple quarters, not a few weeks, before the effect feeds into new contracts.

Three Scenarios from the Iran Uncertainty

From this point, three paths could shape the oil and gas sector heading into next week.

Scenario 1: Prolonged deadlock, Brent holds at USD 100-115. This is the current baseline and the direct context for today's session. If the U.S. continues to reject Iran's terms and the Hormuz blockade extends for more weeks, GAS and PLX retain room to benefit from the price transmission lag. For PVD and PVP, the market may price in expectations of a new drilling cycle ahead of the contract data, but confirmation requires more time. Key signals to watch: any official statement from either party about negotiating conditions, and the weekly U.S. crude inventory report.

Scenario 2: Talks resume, Brent retreats to USD 90-100. If Iran signals concessions or the U.S. accepts a revised negotiating framework — Pakistan is playing a mediating role — expectations of supply recovery would pull Brent lower. The important detail: oil and gas stocks typically correct before the actual oil price decline arrives. This pattern played out in 2022, when PLX and PVD fell significantly even while Brent remained elevated for much of the year. Key signals to watch: any announcement of a concrete meeting schedule or a partial lifting of the Hormuz blockade.

Scenario 3: Full Hormuz blockade, renewed hostilities, Brent above USD 120. Goldman Sachs has warned that Brent could average above USD 120 in the third quarter if Hormuz remains effectively closed for another month.OilPrice In this scenario, input cost pressures would ripple through Vietnam's entire manufacturing sector: transport, fertilizers, plastics, and power. Oil and gas stocks would serve as a relative safe haven, not an outright winner, because the whole market would be bearing higher energy costs. Key signals to watch: any military escalation in the Persian Gulf and global energy market reactions.

What to Watch in the Days Ahead

Developments since early May lean toward Scenario 1. Deadlock is the baseline, and each time the U.S. rejects an Iranian proposal, Brent has added another USD 2-3 in the following session. GAS hitting its price ceiling on May 13 is a direct response to that cycle, not momentum-chasing or broad market enthusiasm.

Scenario 2 (talks resumed) could materialize any week if Pakistan achieves a breakthrough in its mediating role. Scenario 3 (escalation) depends on Tehran's strategic calculation about how far it is willing to push, and its probability remains lower than the other two. Neither can be ruled out entirely.

The bigger picture is that Vietnam's oil and gas sector is benefiting from a genuinely physical disruption to global supply chains, not merely a sentiment-driven rally. Unlike previous oil price cycles, the current one involves an actual break in the delivery route, not just concern about one. That provides a more durable floor for elevated Brent as long as the impasse persists.

The signals that will resolve the scenario over the next five to ten sessions: official statements from both sides on Hormuz, progress through the Pakistan mediation channel, and the weekly U.S. crude inventory release. Those are the data points that will shape the sector's trajectory over the medium term — far more than any single session's price movement.