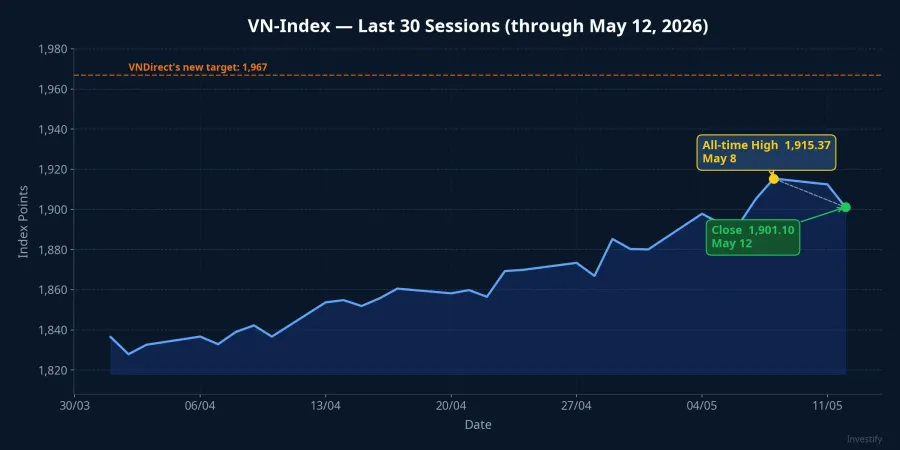

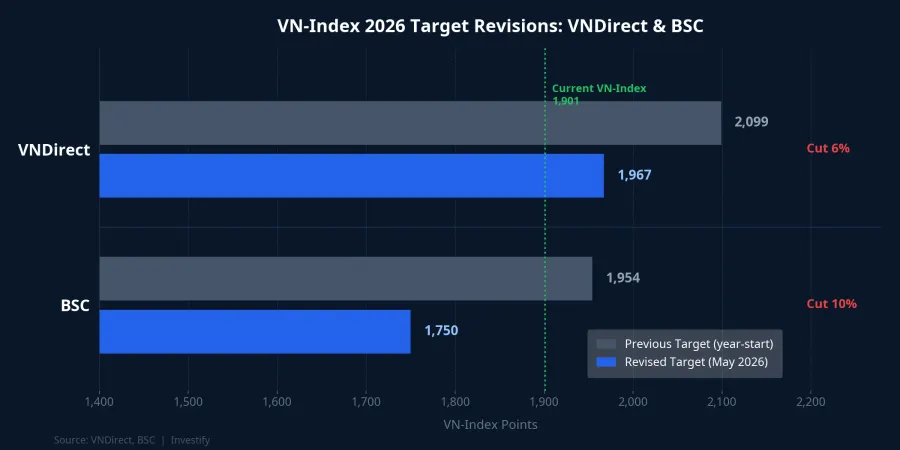

On May 8, the VN-Index reached a new all-time high of 1,915.37 points. Four sessions later it settled at 1,901.10, and on that same day VNDirect released a strategy update: its 2026 year-end target was lowered from 2,099 to approximately 1,967 points, a cut of 132 points from the firm's start-of-year forecast.VnEconomy The gap between the current price and the new target is roughly 3.5% for the seven months remaining in the year.

This is the kind of move that confuses many investors. Strategy reports typically get upgraded when markets rally, not downgraded. What drove the revision, and what does the market's current level tell us that the 1,967 figure does not fully capture?

Why VNDirect cut its midyear target

Looking at the numbers, 1,967 still implies 10.2% growth from end-2025, a double-digit full-year return.VnEconomy The issue is that most of that upside has already been realized: the VN-Index climbed from around 1,670 in early April to 1,915 in approximately five weeks, a gain of nearly 14.7%.

VNDirect cited two drivers for the revision. First, global interest rates have remained higher than expected at the start of the year, raising the cost of capital and compressing equity valuations. Second, the firm lowered its forecast for listed-company net profit growth to approximately 14% for full-year 2026, down from 18% projected earlier.

The revision is not an isolated view. BSC made an even deeper cut, dropping its target from 1,954 to 1,750 points, a reduction of nearly 11%.VnEconomy The consensus among analysts is consistent: earnings expectations are being recalibrated after a strong rally.

Scenario A: 1,967 is the ceiling

The first scenario argues that most of 2026's positive story has already been priced in. Q1 profit for 803 listed companies grew 38.2% year-on-year, a strong result but one already published before the May 12 session, giving the market time to digest it.VnEconomy The nearly 14.7% rally from the early-April low to the May 8 peak has absorbed a large share of near-term optimism.

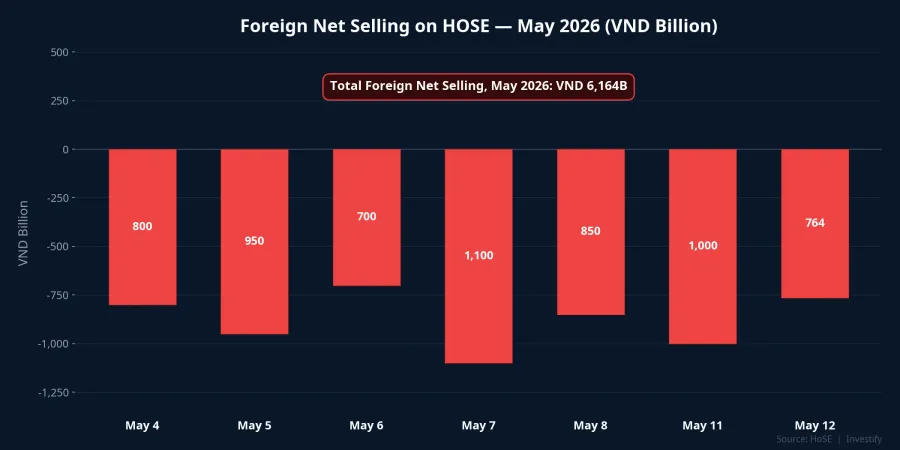

The current foreign-flow data supports this reading. Between May 4 and May 12, foreign investors sold a net approximately VND 6,164 billion on HOSE across seven consecutive sessions, with selling concentrated in market leaders including FPT, VCB, HPG, and ACB. There is no sign yet of a reversal.

If the Fed holds rates elevated through the summer and Q2 margins disappoint against a higher prior-year base, a correction from the 1,900 zone is analytically reasonable. Under Scenario A, 1,967 is the year-end resistance ceiling, and investors expecting another 10–15% from here are likely to be disappointed.

Scenario B: 1,967 is the floor

The second scenario argues that at least three forward catalysts have not been fully reflected in prices yet.

The clearest is the FTSE upgrade in September 2026. FTSE Russell confirmed Vietnam meets the criteria for elevation from Frontier to Secondary Emerging Market status, with Vietnamese shares entering global FTSE indices beginning September 21, 2026, and continuing into 2027.Vietnam Briefing FTSE Russell estimates approximately USD 6 billion in passive inflows from index-tracking funds.LSEG This is mechanical capital: passive funds are required to buy when a stock enters the index, regardless of the valuation at that time.

The second catalyst is the earnings base effect. Mid-2025 quarters showed relatively low profit bases across retail, materials, and banking, meaning Q2 and Q3 2026 growth rates may stay elevated. VNDirect's 14% full-year forecast could prove conservative if H2 surprises to the upside.

The third is historical precedent. In Pakistan (2017) and Saudi Arabia (2019), active capital began flowing into markets two to three months before the FTSE effective date, positioning ahead of the mandatory passive inflows rather than waiting for index inclusion. If Vietnam follows the same pattern, foreign flows could reverse as early as June or July, pushing the VN-Index through 1,967 before the FTSE rebalance officially occurs.

Two signals that will determine the outcome

Both scenarios rest on real evidence. Strong Q1 earnings support the "already priced in" argument; the still-pending FTSE rebalance supports the "more room to run" argument. The difference comes down to the sequence and timing of signals over the next four to five months.

The first signal is foreign-flow direction. If the May selling streak ends in June and at least five consecutive net-buying sessions emerge in key market leaders, that is an early indication that active money is positioning ahead of the FTSE inclusion. If selling continues through July and August without interruption, Scenario A is gaining ground.

The second signal is Q2 earnings quality for the index heavyweights. Reports from the banking names (VCB, ACB, TCB), retail (MWG, FRT), and materials (HPG) are the real-world test for VNDirect's 14% full-year growth call. If Q2 market-wide profit growth exceeds 25% year-on-year, Scenario B has firmer footing. If it comes in below 15%, VNDirect's revised target holds more weight.

Portfolio positioning when upside narrows

The most important shift is in the risk-to-reward profile. With the current price roughly 3.5% below the revised target and a potential technical correction of 8–12% if sentiment turns, standard portfolio management practice favors reducing margin exposure and maintaining a 15–25% cash buffer at levels where the index approaches a consensus resistance zone.

Investors may consider: Those who are sitting on gains of 20–30% from the early-April low can reduce 25–30% of their position in stocks that have already run their course. The remaining position captures Scenario B if foreign flows reverse and Q2 earnings surprise positively. This is not a signal to exit entirely; it is an adjustment to reflect the current risk-reward reality.

Brokerage target cuts in the middle of a year are not sell signals. They are acknowledgments that the easy part of 2026 is over. What comes next depends on three observable variables: foreign-flow direction, Q2 earnings quality, and the FTSE calendar. Tracking these three metrics with discipline matters far more than anchoring to any single analyst's price target.