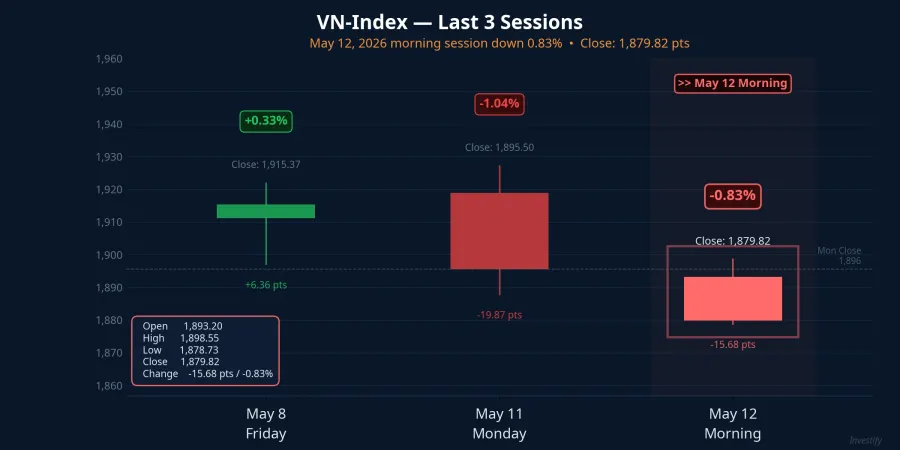

The VN-Index shed 15.68 points in the morning session on May 12, settling at 1,879.82, down 0.83%. Headlines reading "U.S. places Vietnam on highest-level trade watch" spread quickly, and many investors made an intuitive leap toward Section 301 punitive tariffs of the kind imposed on China in 2018. That instinct is not entirely unfounded: Section 301 has a long track record of triggering large-scale trade action. But the technical picture of the 2026 Special 301 Report is very different from that scenario, and conflating three distinct mechanisms is leading investors to position defensively against risks that don't yet exist.

On April 30, 2026, the U.S. Trade Representative (USTR) published the 2026 Special 301 Report, designating Vietnam as a Priority Foreign Country (PFC), the highest alert level in USTR's annual review of intellectual property protection.USTR This is the first PFC designation in 13 years (the last was Ukraine in 2013). Vietnam was mentioned 75 times in the report and is the only country at the PFC level this year.Vietcetera

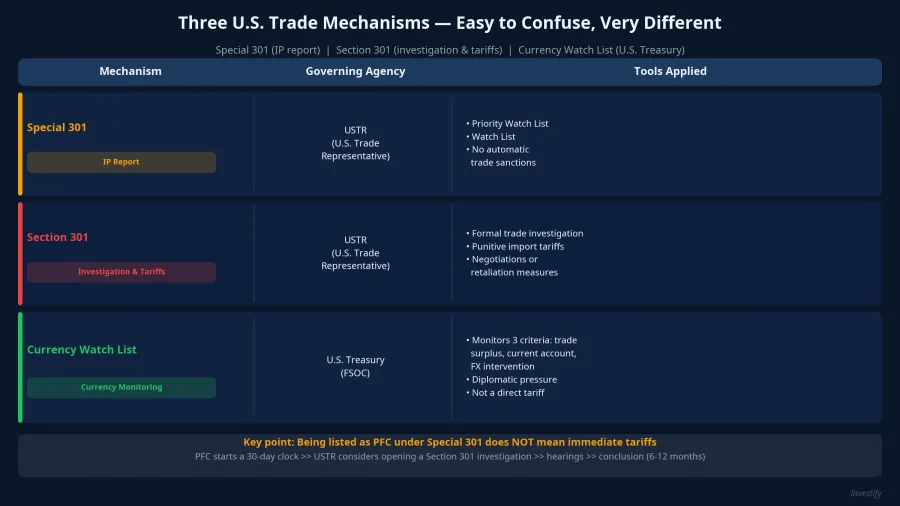

Three Mechanisms Being Treated as One

The critical distinction that the headlines are missing is the difference between three mechanisms that sound similar but operate very differently.

Special 301 is an annual USTR report assessing IP protection practices at U.S. trading partners. It does not automatically trigger tariffs or sanctions. The PFC designation — the highest tier in the report — is a strong signal that USTR may consider further action, but it is not an action in itself.

Section 301 is the investigation and trade remedy tool. This is the legal basis under which the U.S. can impose additional import duties, as it did during the China trade war starting in 2018. A Section 301 action requires a separate investigation with its own public comment process, hearings, and findings.

The Currency Monitoring List is operated by the U.S. Treasury, entirely separate from USTR. It tracks three criteria: bilateral trade surplus, current account surplus, and foreign exchange intervention. The 2026 Special 301 Report has nothing to do with Vietnam's exchange rate policy.

All three mechanisms are sometimes administered by overlapping agencies, which contributes to the confusion. But their objectives and tools are entirely different. When the market sells off across the board as if all three were simultaneously activated, that is a sentiment-driven reaction, not a mechanism-based one.

PFC Is Not a Tariff Order: It Starts a 30-Day Clock

According to USTR's announcement, designating a country as PFC starts a 30-day period during which USTR must decide whether to open a Section 301 investigation specifically related to IP enforcement.USTR This is the point that much of the initial coverage glossed over: PFC is the input to a process, not the output.

If USTR decides to open an investigation within the 30 days from April 30 — meaning by around end of May 2026 — the case enters a phase of bilateral consultations, public comments, and hearings. A full Section 301 investigation typically takes 6 to 12 months to conclude, followed by an additional 30 to 60 days if measures are proposed and implemented.

In other words, the path from April 30, 2026 to any real tariff action (if it comes at all) spans many months and multiple negotiating steps. This is not the instantaneous tariff scenario that a significant part of the market appears to be pricing in.

Investors also need to keep a parallel process separate. On March 11, 2026, USTR launched a separate Section 301 investigation against 16 trading partners including Vietnam, focused on excess export capacity and transshipment risk. That investigation is already in a more advanced stage: hearings ran from May 5-8, with a target completion date of around July 24, 2026. The two tracks have different clocks, different legal bases, and different sector exposures.

Five IP Issues Named in the Report

The 2026 Special 301 Report outlines five specific categories of concern that drove the PFC designation. First is large-scale online copyright infringement, including unlicensed streaming services and IPTV. Second is the widespread availability of counterfeit goods, particularly in fashion and pharmaceuticals. Third is weak border enforcement. Fourth is the use of unlicensed software within Vietnamese businesses. Fifth is the theft of cable and satellite television signals.

Every one of these issues sits squarely within the intellectual property domain. None of the cited concerns relate to exchange rate policy or general trade tariffs.

VN-Index: Market Mechanics or Market Psychology?

The May 12 morning session saw VN-Index decline 15.68 points. This followed an even sharper 19.87-point drop on May 11. The combined two-session sell-off reflects a broadly risk-off posture. The key observation: the selloff in export-related stocks was largely indiscriminate, with little regard for each sector's actual exposure to IP enforcement risk.

A shrimp or coffee exporter selling to the U.S. has minimal real exposure to a Special 301 IP investigation, because those products are not subject to IP-related trade disputes. But the May 12 trading session did not make that distinction.

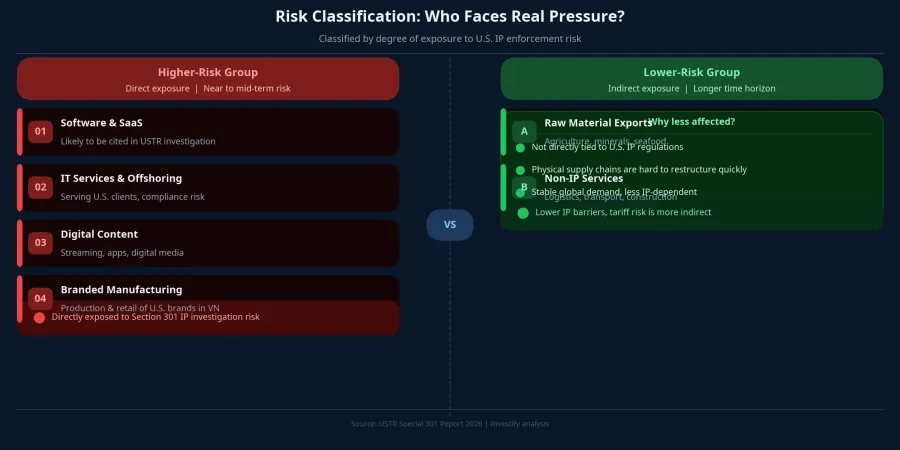

Who Actually Bears the Risk

The real risk from Special 301 and a potential Section 301 IP investigation is not distributed evenly across all export sectors. The groups with genuine near-term exposure are those with clear IP enforcement vulnerabilities and heavy reliance on the U.S. market: software and IT services, digital content platforms, and producers of U.S.-branded goods manufactured or retailed in Vietnam. These are the sectors where a USTR investigation could directly create trade restrictions or rapidly increase compliance costs.NguoiQuanSat

Conversely, raw commodity exports and services not tied to intellectual property have little direct connection to this mechanism. The broad defensive selloff across general export stocks reflects sentiment, not an accurate reading of how Special 301's risk transmission actually works.

The real risk is concentrated in: software companies with U.S. clients, IT outsourcing firms, digital content platforms, and manufacturers operating U.S. brand licenses in Vietnam. For those specific businesses, monitoring USTR's end-of-May decision is the top priority in the near term.

What VCCI Is Recommending

The Vietnam Chamber of Commerce and Industry (VCCI) has recommended that businesses proactively review three areas of compliance, even before USTR decides whether to open a formal investigation.VnEconomy

The first is the legal status of software currently in use internally. The second covers the use of images, trademarks, packaging, and promotional content. The third is the provenance and usage rights for data, designs, and digital works. For digital platforms, e-commerce operators, and social media-reliant businesses, VCCI is urging stronger content moderation processes and faster handling of IP infringement reports.

This is prudent compliance hygiene. Whether or not USTR opens a formal investigation, cleaning up IP practices now reduces the likelihood of a business becoming a named example in any future investigation file.

Two Milestones to Watch in May

The most important near-term trigger is the USTR decision around end of May 2026, once the 30-day clock from April 30 expires. If USTR opens a Section 301 IP investigation, companies in the high-exposure group (software, IT services, digital content) enter a consultation and hearing phase lasting 6 to 12 months. If USTR decides not to open an investigation or defers the decision, the near-term risk from the Special 301 IP track cools substantially.

The second milestone is the conclusion of the separate Section 301 excess capacity investigation: hearings just ended on May 8, and the target conclusion is around July 24, 2026. That is a different risk track, with a different timeline and different sector exposure.

Today's broad-based selloff reflects a market that merged several distinct risk mechanisms into one undifferentiated story. Once the mechanisms are separated, portfolios have a clearer basis for reassessing each sector group according to its actual IP enforcement exposure, rather than adjusting uniformly to an initial news cycle.