The Last Legal Anchor Is Gone

On the morning of May 12, 2026, a routine update to Novaland's business registration removed Bui Thanh Nhon from the line that reads "legal representative."NguoiQuanSat His replacement is Duong Van Bac, who now serves as both CEO and legal representative of the company. On paper, it is a procedural update.

But placed against the timeline of the past nine weeks, this update closes a chapter. On April 16, 2026, Nhon stepped down as chairman of NovaGroup, the parent company, in favor of his son. Seven days later, at the April 23 Annual General Meeting in Ho Chi Minh City, Bui Cao Nhat Quan was elected Chairman of Novaland's Board of Directors for the 2026–2031 term.BaoPL Today's change completes the handover. After 21 years as the company's founder, Nhon now stands outside all three layers: the board, the management team, and legal representation.

The leadership transition coincides with the most financially stressed period in the company's recent history. Rather than focusing on the personnel change itself, this post examines what the new leadership is actually inheriting.

The Successor: Back After Nine Years Away

Bui Cao Nhat Quan, Chairman of the Board of Directors of Novaland, was born in 1982 and holds a Bachelor's degree in Business Administration from Western Washington University (USA). He is not new to the Novaland ecosystem. From 2007 to 2017, he served in multiple roles: board member, Vice Chairman, and Deputy CEO.CafeF In 2017, he resigned from all positions and largely disappeared from the business press for nearly a decade.

His return came on March 16, 2026, at a strategic cooperation signing between LPBank and Novaland, where he was introduced as Chairman of Novaland's Executive Council.DanTri Within two months, both the NovaGroup and the listed Novaland chairmanships were transferred to him within the same week. His personal ownership stake in NVL currently stands at 3.37% of total capital.

The governance structure accompanying this change follows the Enterprise Law: Duong Van Bac retains his role as CEO and legal representative. The board chairman sets strategic direction; the CEO manages operations and signs off on specific legal transactions. The two roles are clearly separated per standard governance design.

Liabilities and Assets: Numbers That Cannot Be Ignored

This is more important than any personnel announcement. Per CafeF's compilation from Novaland's financial statements, the company's total liabilities exceed VND 186,000 billion.CafeF As of May 12, NVL's market capitalization stands at VND 36,600 billion. The debt-to-market cap ratio is approximately 5x, a figure every investor in this stock needs to understand before making any decision.

Three debt restructuring tracks are now running concurrently following the AGM.

Track 1: USD 300 million international bond. Issued on July 16, 2021, at 5.25% per annum, originally due June 30, 2027. The AGM extended the maturity to July 16, 2028. The key detail: interest is not being paid in cash but is being capitalized into the principal. The outstanding debt continues to grow, and the obligation is simply deferred to the new maturity date.

Track 2: Domestic bond-to-equity swaps. The AGM approved two mechanisms: swapping 320 million shares for VND 8,719 billion in debt, and swapping 151.8 million shares at a fixed price of VND 40,000 per share for VND 6,074 billion in debt from 13 bond series issued in 2021–2022. With NVL closing at VND 16,400 on May 12, the swap price of VND 40,000 is 2.4x the current market price. Bondholders are accepting equity at a significant premium to the listed price. Additionally, 164 million shares have already been issued to retire VND 2,577 billion in internal debt owed to NovaGroup and Diamond Properties,VnExpress and 2.47 million convertible shares were issued to BNP Paribas Financial Markets on March 31, 2026.CafeF

Track 3: New private placement of 350–800 million shares, subject to market conditions. This is separate from the debt swap shares and represents additional potential dilution.

The bottom line: through the end of 2026, Novaland does not have the cash flow to repay debts in cash.NguoiQuanSat The overwhelming majority of debt pressure is being addressed through equity dilution and maturity extensions, not operational cash generation. The realistic timeline for meaningful cash repayment does not begin until late 2026 at the earliest, with the bulk shifted to 2027.

The Stock and the Dilution Math

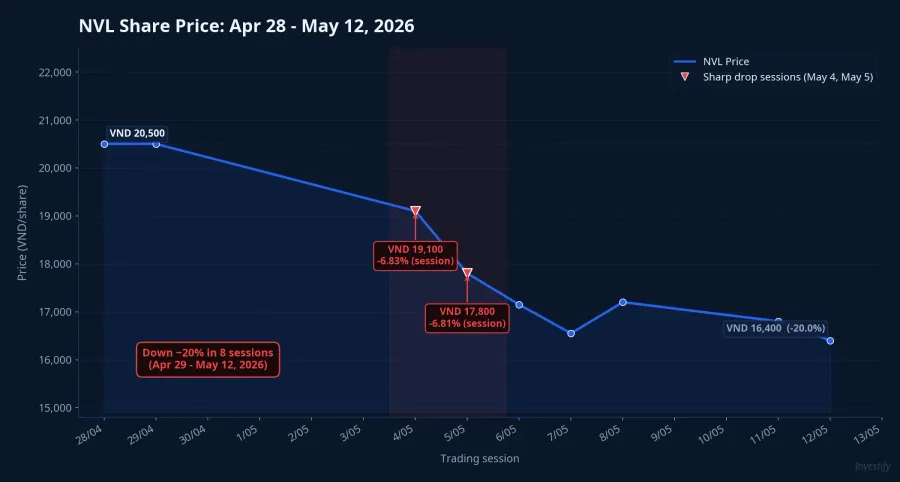

Since the AGM, NVL shares have declined roughly 20% over 8 sessions. From VND 20,500 on April 29, 2026, the stock fell to VND 16,400 by May 12. The steepest drops were concentrated in two consecutive sessions: May 4 fell 6.83% and May 5 fell a further 6.81%, both on elevated volume of 35–46 million shares traded.

The decline coincides in timing with two specific pieces of information becoming visible to the market: the bond-to-equity swap involving hundreds of millions of new shares, and the private placement plan for an additional 350–800 million shares. To be precise: this is a correlation in timing, not a proven single-cause relationship. However, the dilution arithmetic is real and cannot be dismissed.

Running the cumulative numbers: 320 million approved swap shares, plus 151.8 million, plus 164 million already issued, totals approximately 636 million new shares. The pending 350–800 million private placement is on top of that. Total potential new shares in circulation could exceed 1 billion units. At that scale, the value of each NVL share depends far more on the total enterprise value the company achieves after restructuring than on last quarter's EPS.

Changing the Chairman Does Not Change the Maturity Schedule

The real risks lie in two operational variables that have nothing to do with who sits in the chairman's seat. The first is legal progress on core Ho Chi Minh City projects: the actual number of land certificates issued and units delivered, which determine incoming cash flows. The second is executing the private placement at a price high enough to meaningfully reduce debt. If the market price stays depressed, new shares dilute existing holders without raising enough capital to matter.

Novaland's 2026 profit plan targets VND 1,852 billion, with operational goals of delivering more than 2,600 units and issuing over 4,300 land certificates for its central Ho Chi Minh City projects. These two metrics are the most concrete indicators of how the restructuring is actually progressing, because they directly reflect the company's capacity to generate revenue.

Key signals to watch over the coming months: the Q3 2026 product delivery progress report; the first private placement under the new board and its actual pricing; and the international debt repayment schedule for 2027–2028, when capitalized interest will have compounded through 2026. A leadership transition is an observable governance milestone. The maturity calendar, however, does not adjust for it.