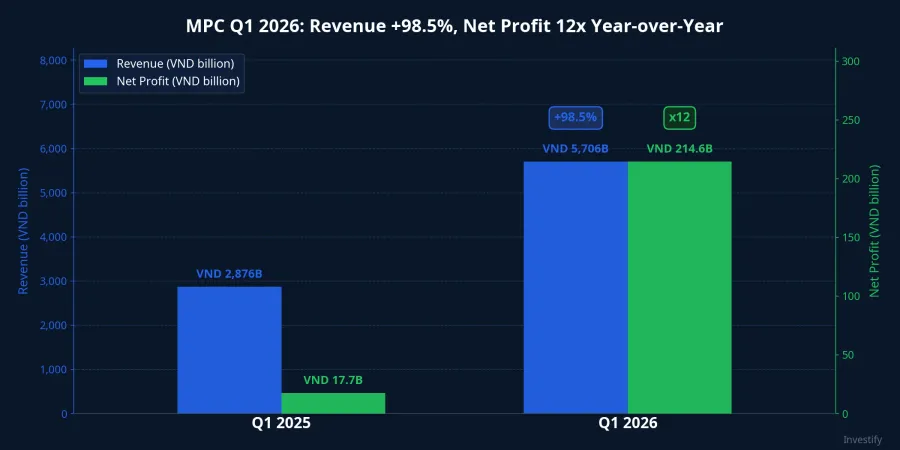

Minh Phu Seafood Group (HOSE: MPC) released its Q1 2026 financial results with two figures that demand a second look. Revenue came in at VND 5,706 billion, up 98.5% year-over-year. Net profit after tax reached VND 214.6 billion, a 12-fold increase from the same period last year.Tin Nhanh Chung Khoan

Revenue doubled, profit multiplied by twelve. That 6x gap between the two growth rates is not a reporting error. It is the product of three mechanisms working in concert: operating leverage in the shrimp processing industry, a near-zero base from two consecutive loss-making years, and a product mix shift toward higher-margin value-added goods. This article unpacks each mechanism and then turns to the VND 5,500 billion inventory sitting on the balance sheet, asking what it means for the rest of 2026.

MPC closed at VND 16,200 per share on May 11, with a market capitalization of approximately VND 6,500 billion.

Three Mechanisms Behind the 12x Number

Mechanism 1: Operating Leverage on a Thin-Margin Structure

Shrimp processing has a defining structural characteristic: cost of goods sold accounts for the vast majority of revenue. In Q1 2025, MPC's COGS consumed roughly 90.85% of revenue, leaving a gross margin of just 8.83%.Tin Nhanh Chung Khoan Within that dense cost structure, some expenses are variable — raw shrimp, packaging, logistics — but a significant portion are fixed costs spread across capacity: plant depreciation, base salaries, and cold-chain maintenance.

When revenue doubles, fixed costs do not double with it. They are spread over a larger revenue base, widening gross margin meaningfully. MPC's net margin stood at roughly 0.62% in Q1 2025; by Q1 2026 it had expanded to approximately 3.76%, a 6-fold increase. That 6x margin expansion multiplied by roughly 2x revenue growth is precisely what produces the 12x profit figure.

This is the essence of operating leverage: when gross margin is thin, a company sits very close to its breakeven point. Each incremental unit of revenue above breakeven drops nearly entirely to the bottom line. The same mechanism works in reverse: when revenue falls, profits decline far faster.

Mechanism 2: A Base Set at the Bottom of the Cycle

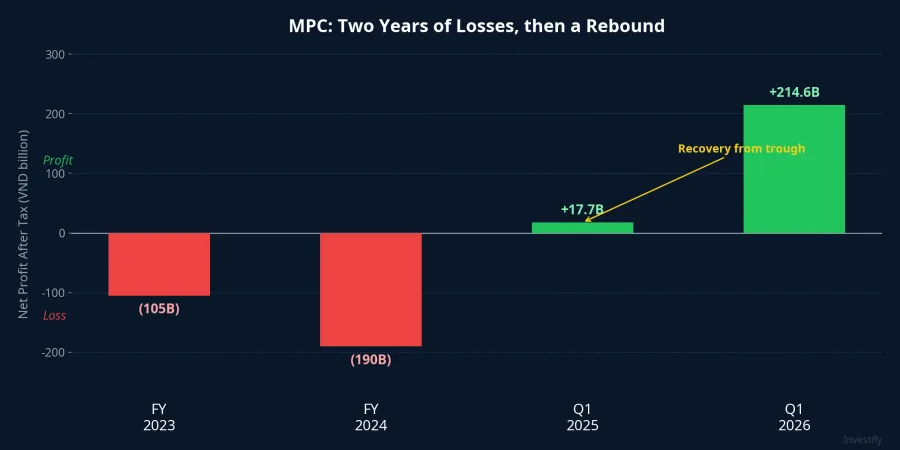

The "12-fold" headline also reflects a context that tends to get overlooked: MPC had just endured two consecutive years of losses. The company lost VND 105 billion in 2023, then lost an additional VND 190 billion in 2024. Q1 2025 registered VND 17.7 billion in net profit, a number so small it merely signaled that the business had stopped bleeding, not that it had fully recovered.Tin Nhanh Chung Khoan

When the denominator sits at trough levels, any growth ratio inflates dramatically. VND 214.6 billion on a base of VND 17.7 billion produces 12x; that same VND 214.6 billion placed next to a normal MPC quarter from 2018-2019, when average quarterly profit ran VND 200-250 billion, would read simply as "back to normal." Investors should interpret the 12x figure in its proper context: it measures the speed of recovery from a trough, not a new structural growth trajectory.

Mechanism 3: A Product Mix Shift Toward Value-Added Goods

The third mechanism lies in a change in product composition. According to MPC's own disclosures, the Q1 2026 improvement was driven by expanding output and exports in value-added and deep-processed shrimp products, a segment that carries higher margins than raw shrimp.Tin Nhanh Chung Khoan This is worth noting in context: raw shrimp prices in Ca Mau rose 30-50% year-over-year during the same period, meaning input costs rose substantially. Ordinarily that would compress gross margin. The product mix shift absorbed and overcame that cost pressure.

On the market side, China and Hong Kong drove Vietnam's shrimp exports in the first quarter, growing nearly 45% year-over-year. The US and Japan remained subdued due to cautious consumer demand. The heavy concentration of MPC's revenue in Greater China supported Q1 performance but creates a vulnerability: a policy change on Chinese imports or an unfavorable seasonal pattern could reverse momentum faster than expected.

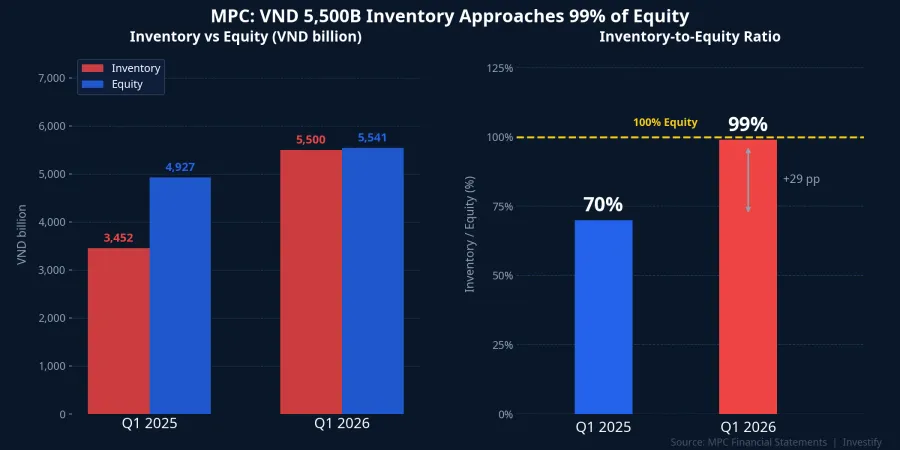

VND 5,500B Inventory: Two Sides of a Strategic Bet

As of end-Q1 2026, MPC's inventory stood at VND 5,500 billion, nearly matching total equity of VND 5,541 billion and up roughly VND 500 billion from the start of the quarter.Tin Nhanh Chung Khoan In Q1 2025, inventory was VND 3,452 billion, roughly 70% of equity at that time. The inventory-to-equity ratio has climbed from about 70% to approximately 99% in a single year.

High inventory in shrimp processing cuts both ways. On the positive side: the company has locked in raw material supply during peak harvest season, secured the sourcing pipeline for large export contracts, and can fix input costs before prices rise further. With Ca Mau shrimp prices up 30-50% year-over-year, the "strategic stockpiling" argument has genuine merit.

The risk side is equally real: large inventory ties up cash flow, drives up storage and cold-chain maintenance costs, and can rapidly become a liability if the shrimp price cycle turns. When input prices correct downward after a run-up, the high-cost inventory purchased earlier flows into cost of goods sold in subsequent quarters, squeezing gross margin in the opposite direction. This is precisely the mechanism that drove MPC's losses through 2023-2024.

The key question is not "is high inventory good or bad" but rather "can MPC liquidate at prices that validate the accumulation?" Q2 and Q3 inventory turnover and gross margin will answer that question.

The 2026 Plan and the Pressure on the Remaining Three Quarters

At MPC's 2026 annual shareholder meeting, management set targets of VND 23,000 billion in revenue and VND 1,100 billion in net profit after tax, the highest revenue target in the company's history. After Q1, MPC has completed approximately 25% of its revenue target and 20% of its profit target for the year.Tin Nhanh Chung Khoan

The profit pace running behind revenue pace is worth flagging. Revenue in Q1 ran at exactly one-quarter of the full-year plan. Profit only reached 20%, meaning the remaining three quarters need to deliver an average of roughly VND 295 billion each, roughly 37% more than Q1's VND 214.6 billion. To get there, either net margin must expand further from the current 3.76%, or volume must accelerate.

Two variables will determine whether that 37% gap can be bridged: whether raw shrimp prices continue rising and compress gross margin, and whether the VND 5,500 billion inventory can be sold at prices that match or exceed the accumulation cost, rather than being offloaded at a discount.

Reading "N-Fold" Headlines: A Framework That Applies Beyond MPC

MPC's Q1 story is a clean lesson in operating leverage within a thin-margin industry. Each percentage point of incremental revenue amplifies many times over at the profit line when a company sits near breakeven. The same mechanism works symmetrically on the downside. Investors encountering "profits multiplied N-fold" headlines at catfish processors, rice millers, or cashew exporters should apply the same framework: a large N does not necessarily indicate structural strength. It may simply indicate a position close to the breakeven line.

For MPC specifically, the Q1 recovery is genuine and grounded in verifiable drivers. But it is a recovery from a trough amplified by operating leverage, not a growth rate that can be extrapolated forward for the remainder of 2026. Three signals are worth tracking:

First, Q2 gross margin: if it holds above 11-12%, the value-added product mix is operating reliably; if it drops below 10%, input cost pressure has begun eroding margins.

Second, inventory turnover: if inventory declines steadily as revenue remains strong, the company is liquidating at favorable prices; if inventory keeps building, cash flow pressure becomes a risk that needs to be quantified.

Third, market concentration: how large is China and Hong Kong's share of MPC's export revenue, and how much ground is the US segment recovering? This variable determines whether the company can diversify its geographic concentration risk.

The Q2 2026 report will be the first data point to test whether the recovery momentum holds and how the VND 5,500 billion inventory position is being managed.