This morning, the 2nd Session of the Hanoi People's Council (HĐND) convenes to consider the investment policy for the Red River Landscape Boulevard project. Among the three-member consortium proposing this project, Hoa Phat (HPG) is the only HOSE-listed company, meaning the outcome of today's session will feed directly into market sentiment when trading opens at 9 AM.Tien Phong

This post does not forecast prices. The goal is to help investors holding or tracking HPG understand three things before the session: the actual scale and capital structure of the project, why 4 of the original 7 consortium members withdrew, and — most critically — what today's decision actually means in terms of the legal approval process.

Capital Structure: VND 736,963 Billion and How the BT Mechanism Works

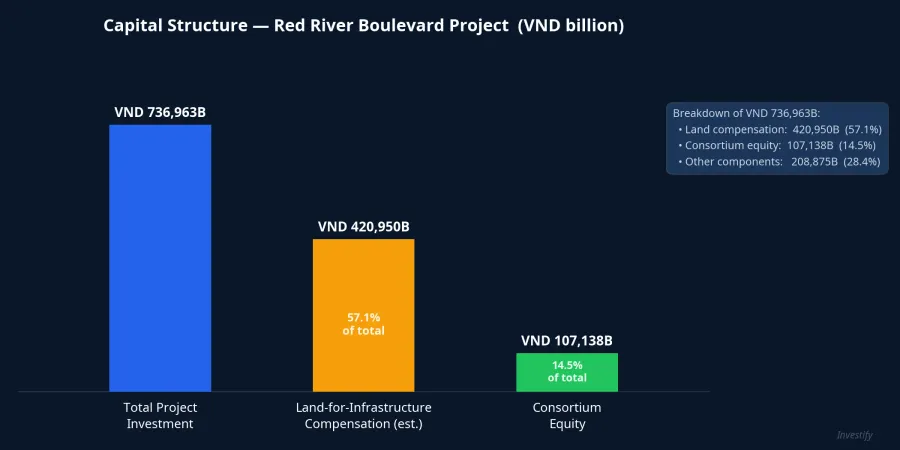

The preliminary total investment stated in the dossier submitted to the HĐND on May 11 stands at approximately VND 736,963 billion (over USD 27 billion), down nearly VND 118,000 billion from the year-end 2025 estimate.Dan Viet The project comprises 17 sub-projects scheduled to run from 2026 to 2038, spanning over 11,400 hectares across 16 wards and communes along both banks of the Red River.Nguoi Quan Sat

The financing model is BT (Build-Transfer), meaning the consortium builds public infrastructure in exchange for land. The consortium commits to contributing approximately VND 107,138 billion in equity (14.5% of total investment). The remainder is recovered through compensation land parcels estimated at approximately VND 420,950 billion, comprising 12 plots totaling over 5,000 hectares, of which around 2,800 hectares fall within the project's planned development zone.CafeBiz

Looking at the numbers more carefully: the estimated land value of VND 420,950 billion still falls roughly VND 293,000 billion short of total investment. The consortium therefore proposes an additional approximately 2,265 hectares of land outside the original development perimeter to cover the gap. The key risk in any BT structure is the time gap: the consortium spends upfront, receives land later, and land valuations at the time of transfer are reset to current appraisal tables rather than locked in at the start.

Why 4 of the Original 7 Members Withdrew

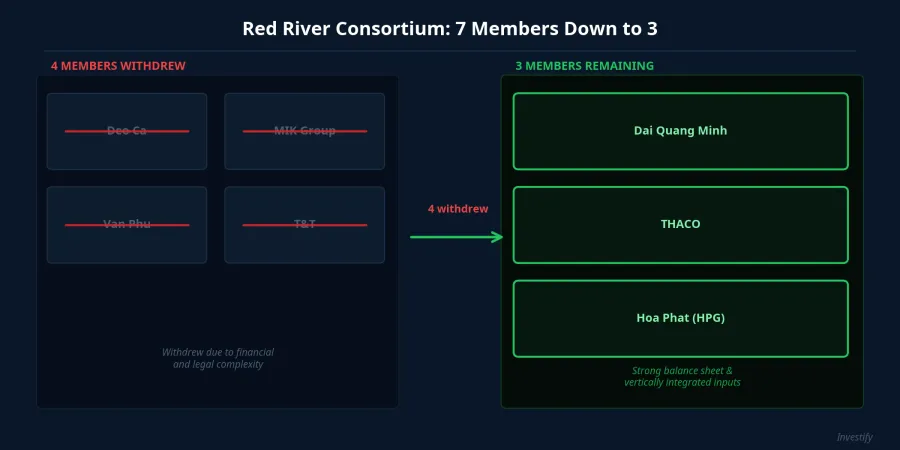

The consortium started with seven members. Deo Ca, MIK Group, Van Phu, and T&T withdrew across successive dossier revisions. The final filing submitted to the Hanoi People's Committee lists only three: Dai Quang Minh (a THACO subsidiary), THACO, and Hoa Phat.Dan Viet

Press reports attribute the withdrawals primarily to financial constraints and the legal complexity of committing to a large-scale, long-horizon project. What is notable about the three remaining members is a shared characteristic: all have the financial depth to sustain long-term capital commitments and the vertical integration to supply key project inputs independently. THACO handles construction machinery; Hoa Phat supplies construction steel; Dai Quang Minh brings urban development experience from the Sala project in Ho Chi Minh City.

The shrinkage from seven to three is not necessarily a negative signal about the project itself. It does, however, reflect that most initial participants assessed the project's complexity as exceeding their capacity for long-term commitment. Even with a clear land-for-infrastructure repayment path laid out on paper, the majority chose to exit early.

HPG's Financial Health and the Capital Equation

At the AGM on April 21, 2026, Mr. Tran Dinh Long, Chairman of Hoa Phat Group (HPG), called this a "100-year project" and stated: "If we don't do it now, there will be no second chance." He also disclosed Q1/2026 results: revenue of VND 53,500 billion (up 40% year-on-year) and after-tax profit of VND 9,056 billion (up 170% year-on-year).CafeF

HPG's current financial foundation is solid. As of the May 8 close, HPG shares traded at VND 27,850 per share, with market capitalization of approximately VND 213,800 billion. But the capital equation becomes more demanding when this new commitment is layered on top of existing plans.

The VND 107,138 billion equity commitment belongs to the full three-member consortium, with no official breakdown by member published yet. If split evenly, Hoa Phat's share would be in the range of VND 35,000–40,000 billion, representing roughly 16–19% of the current market capitalization, or approximately 1.6–1.8 times the company's full-year 2026 after-tax profit target of VND 22,000 billion. At the same time, Hoa Phat is running the Dung Quat 2 integrated steelworks, itself one of Southeast Asia's largest greenfield capital projects, in parallel.

The financial arithmetic therefore requires Hoa Phat to draw on additional funding channels: bond issuance, bank loans, equity offerings, or operational cash flow spread over multiple reporting periods. Dilution risk and leverage risk are two factors that belong in any long-term HPG valuation framework. For now, the equity split remains a consortium-level estimate; there is no official confirmation from Hoa Phat of each member's actual contribution.

What Exactly Does Today's Vote Decide?

This is the most important point to get right, and also the most common misread. The HĐND session this morning is reviewing the investment policy proposal, not issuing final project approval.

If the HĐND passes the policy, the PPP-BT process still has a long sequence of steps ahead: preparing a full feasibility study, independent appraisal, BT contract negotiation, formal investor selection under applicable regulations, contract signing, land clearance, and finally ground-breaking. For a project of this scale, each step can take months to years.

In plain terms: a favorable outcome today is a necessary condition for the consortium to continue. It is not a sufficient condition for the project to translate into actual cash flows for HPG within the next several quarters. This distinction matters especially for newer investors.

Reading the Session: Procedural Signals vs. Substantive Signals

A practical framework for today's session is to separate two types of signals:

Procedural signals: Does the HĐND resolution approve the investment policy, and if so, does it attach specific conditions around the land compensation parcels, construction timeline, or capital structure?

Substantive signals: HPG's price and volume during the session. If the stock rallies meaningfully but trading volume does not surge above the recent 5-session average (approximately 26 million shares per session), the move most likely reflects short-term sentiment rather than a fundamental re-rating. Institutional participation of a more durable kind tends to come with a clear volume breakout alongside a price move through key resistance.

Post-session confirmation signals: official disclosure from Hoa Phat of the actual equity contribution split, capital-raising plans, and specific land compensation terms. All figures currently available are consortium-level estimates without per-member allocation.

A Story Longer Than One Trading Session

Today's HPG story extends beyond a single trading session's range. Hoa Phat is simultaneously building out Southeast Asia's largest steel capacity at Dung Quat and now committing to urban infrastructure on a generational scale. If successful, the long-term investment thesis changes substantially. If the capital plan is not managed carefully, dilution and leverage could weigh on EPS growth for years.

Today's HĐND outcome opens or closes a legal gateway. The more important signal to watch next is not HPG's price over the coming sessions but the actual equity split between consortium members and the capital-raising plan that Hoa Phat's management discloses once the investment policy is formally approved.