On the morning of May 11, the VN-Index stood at 1,921.29 points, edging past the previous week's closing peak of 1,915.37. The backdrop behind that number runs deeper than short-term trading sentiment. FTSE Russell has officially confirmed that Vietnam will be reclassified from Frontier to Secondary Emerging Market status, effective at market open on Monday, September 21, 2026, with approximately 28 Vietnamese stocks joining the index.LSEGVietnamNews

For investors already holding Vietnamese ETFs or stocks tracked by FTSE Vietnam indices, the practical question is not "should I buy?" but whether the market's technical infrastructure will be ready in time. One piece still being assembled is a controlled short-selling mechanism. Vietnam's Ministry of Finance has tasked the State Securities Commission (SSC) to work with the Vietnam Securities Depository (VSD) and the exchanges to research and pilot securities lending and controlled short selling during the 2026–2028 period.VnExpress

Why Markets Need to Move in Both Directions

Think of it this way: when a market only allows buying, prices only reflect optimism. The investors who believe a stock is overvalued have no tool to express that view with real money. The result is that prices stay disconnected from fair value for longer than they would in a two-sided market.

For ETFs, the mechanics get more concrete. Market makers stand between buyers and sellers, creating new ETF units by purchasing the underlying basket and redeeming them by selling it back. Their job is to keep the ETF price trading close to its NAV. Without the ability to borrow and short shares as a temporary hedge, market makers must carry overnight risk every time a price gap opens up. They do not absorb that risk for free: they demand wider bid-ask spreads, and the ETF trades at a persistent premium or discount to NAV. Late buyers pay the price.

This is why FTSE Russell includes short-selling infrastructure in its emerging market criteria: the stock lending pool must be large and stable, the infrastructure must be transparent with a central counterparty clearing mechanism, and foreign investors must have access to data on lending balances, borrowing fees, and liquidity.

What "Controlled" Actually Means in Vietnam's Model

Vietnam's approach is the opposite of the open model used in the US or UK, where qualified investors can short most listed securities with restrictions mainly around the uptick rule and large-position reporting. Vietnam's framework defaults to prohibition and opens only what is explicitly permitted, with three main layers of constraint.

The first layer is the eligible stock list. Only large-cap, high-liquidity stocks with a sufficiently wide free-float will qualify, making the eligibility list closely resemble what FTSE Vietnam already tracks rather than the whole market.

The second layer is initial margin and margin-call mechanics. Initial margin requirements will likely be set above the stock's typical daily volatility range, with top-up calls triggered when prices move unfavorably, similar to how margin lending already works.

The third layer is position limits. Caps will apply per investor and for the aggregate market, preventing short positions from concentrating in a single stock or a single session. VSD sits at the center as the central counterparty: lenders (open-ended funds, ETFs, custodian banks, large institutional holders seeking to optimize return on their portfolios) and borrowers (securities firms and qualifying investors) transact through VSD's centralized system rather than on a bilateral basis.

Lessons from the Gulf

Saudi Arabia and Kuwait both completed this journey before their FTSE and MSCI upgrades. Both markets had to build out a functioning securities lending and short-selling framework as a prerequisite for reclassification. Once live, ETFs tracking those indices saw higher trading volumes and tighter premiums or discounts to NAV, as market makers gained the hedging tools they needed and passed that benefit through to end investors via narrower spreads.

The key lesson from both cases: controlled short selling did not crush prices, as many feared. The volume of passive capital flowing in at reclassification dwarfed the amount that could realistically be shorted in the early stages, when eligible stock lists were still narrow. The practical takeaway is that controlled short selling does not create immediate downward pressure, but it makes markets price more accurately over time.

The Scale of Capital Waiting for September 21

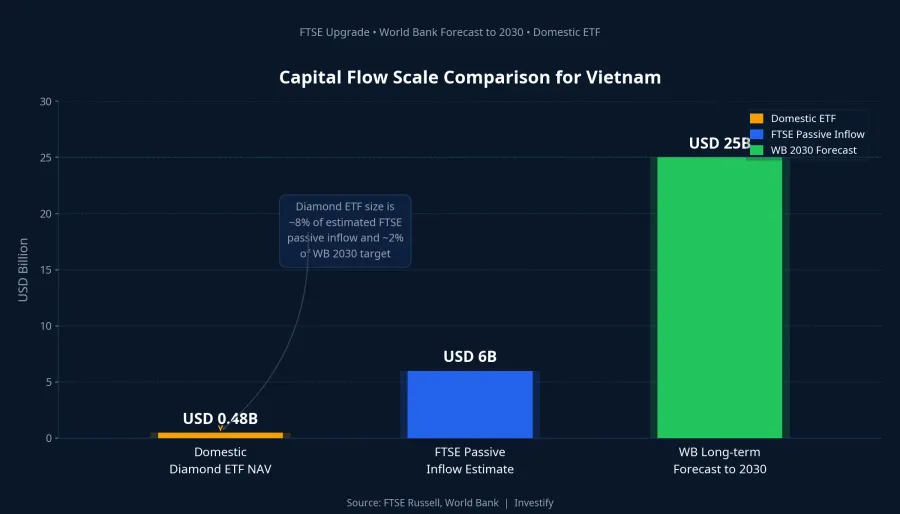

FTSE Russell estimates that approximately USD 6 billion from passive funds tracking the FTSE Emerging Index will flow in automatically once Vietnamese stocks are added to the basket.Vietnam Briefing The World Bank projects short-term inflows from passive and active investors of around USD 5 billion around the reclassification event, with total long-term capital potentially reaching USD 25 billion by 2030.Vietnam Briefing

For context: the DCVFM VN Diamond ETF (ticker FUEVFVND) currently has net assets of approximately VND 12,140 billion, equivalent to roughly USD 480 million.Vietstock The FTSE passive inflow estimate of USD 6 billion alone is more than twelve times the size of one of Vietnam's largest domestic ETFs. That scale gap illustrates why market infrastructure must meet the standards that foreign funds require before the capital actually arrives.

What ETF Holders Need to Know Between Now and September

To put it plainly: controlled short selling will not directly move your portfolio up or down in the near term. It is a plumbing condition, one that must be in place for two more critical things to work smoothly: foreign capital flowing in on FTSE terms, and ETF units trading close to NAV rather than swinging wide in volatile sessions.

For investors already holding ETFs benchmarked to FTSE- or VN30-related indices, the upgrade story has already been partially priced in. The period when passive funds actually rebalance their portfolios tends to fall in the week before and after September 21, not now. For investors who do not yet have a position, dollar-cost averaging between now and the start of Q3 is a widely used approach to avoid the risk of entering at a short-term peak.

Rather than watching the VN-Index every session, there are three signals worth tracking more closely between now and September. The first is when the SSC publishes a draft short-selling regulation and eligible stock list: that publication will indicate whether the legal framework is solid enough. The second is the securities lending fee that VSD sets when the pilot goes live: that figure directly affects market makers' hedging costs and, in turn, the ETF price spread. The third is the premium or discount of Vietnamese ETF units to NAV during high-volatility sessions: the most real-time indicator of whether the mechanism is actually running smoothly.

September 21 is the date, but the quality of what happens after depends on whether technical building blocks like VSD and controlled short selling are in place on schedule. That is the real story worth watching in the months ahead.