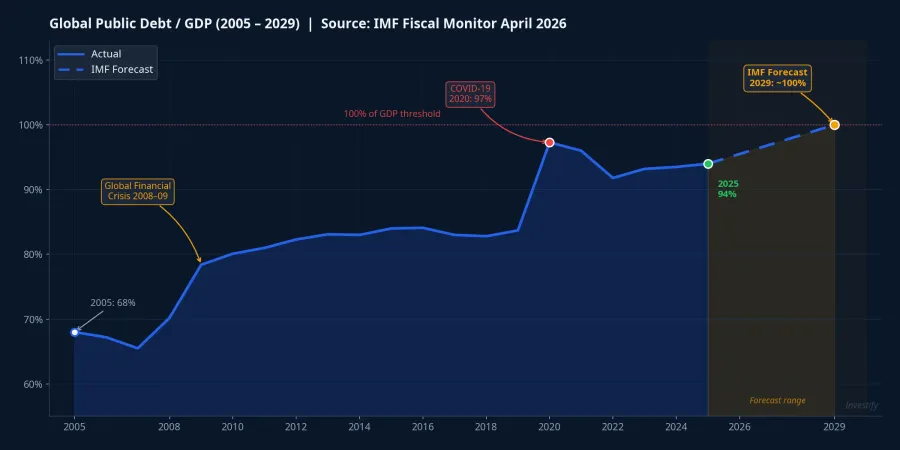

The IMF Fiscal Monitor for April 2026 confirmed that global public debt is closing in on 94% of GDP in 2025 and is projected to breach 100% by 2029, a year sooner than the Fund's previous estimate.IMF That would put the global debt burden at its highest level since 1948. Against that backdrop, Vietnam stands out as a notable exception: public debt at approximately 35–36% of GDP at end-2025, comfortably below the National Assembly's 60% ceiling.VnEconomy

The more useful question for individual investors, however, is not whether Vietnam's public finances are safe. It is whether that advantage shields their portfolios from rising borrowing costs. The short answer is: not entirely. For an emerging market, the cost of capital is set not by domestic debt dynamics but by the rate on the world's reserve currency. The transmission runs through the US dollar, not through the domestic bond market.

Five Economies, Very Different Positions

Placing five major economies on the same scale makes the divergence stark. Japan sits at roughly 230–240% of GDP,IMF DataMapper a position Tokyo has managed for decades through a high domestic ownership structure. The United States stands at approximately 124% of GDP in 2025, with the IMF projecting a rise past 142% by 2031 absent fiscal reform.IMF China is approaching the 100% threshold at around 99% of GDP in 2025, while the euro area averages roughly 87%.

Vietnam, at around 36% of GDP, is not just below the 60% ceiling but also well within the warning band for debt-service obligations relative to budget revenues (around 20–21%, below the 25% alert level). With an average debt maturity of 9.1 years and an average interest rate of approximately 3.1% per annum, Vietnam's government retains genuine fiscal room.VnEconomy

Why Low Domestic Debt Does Not Block High Capital Costs

The structural point worth understanding is this: the cost of capital in any emerging market tracks the global risk-free rate, which is anchored to US Treasury yields. When US public debt is large, the Treasury must sell ever-larger volumes of bonds and must offer yields attractive enough to find buyers. The 10-year Treasury yield has held above 4.0% per annum for more than twelve consecutive months, a sustained level not seen in over 15 years.

From that elevated USD yield floor, three transmission channels reach into Vietnamese investors' portfolios regardless of the domestic debt ratio:

Channel one: corporate cost of capital. When USD yields are high, Vietnamese corporates raising international capital through bond issuance must pay a larger risk premium than during the low-rate era. Domestic government bond yields at the 5–10 year tenor also moved higher through Q1 and early Q2 2026, consistent with a strong-dollar, high-Fed-rate environment. As domestic government yields rise, the discount rate applied to all listed companies rises with them, including companies with zero foreign-currency borrowing.

Channel two: USD/VND exchange rate. A widening interest rate differential in favor of USD makes holding the dollar more attractive, applying gradual downward pressure on the dong. The USD/VND rate moved from around VND 26,300 at end-2025 to approximately VND 26,355 at end-April 2026, even with the State Bank of Vietnam intervening actively. A weaker dong does not only affect importers and exporters. For individual investors, it compresses the real yield on VND-denominated portfolios when inflation erosion is factored in.

Channel three: foreign portfolio flows. When US yields are high and the dollar is strong, international portfolio capital tends to reallocate toward safe-haven assets. In 2025, foreign investors were net sellers of nearly VND 139,000 billion across Vietnamese equity markets, with over VND 129,000 billion of that concentrated on HOSE alone, a 43% increase from 2024's figure and the largest annual net selling on record.VietnamBiz This was not a judgment on Vietnamese corporate fundamentals. It was a global capital allocation decision driven by the USD yield environment.

How Each Asset Class Is Affected

The three most widely held asset classes among Vietnamese retail investors show very different profiles in this environment:

Bank deposits offer the clearest defensive positioning right now. The 12-month rate at the Big 4 state banks sits around 5.0–5.5% per annum; smaller banks and online platforms reach 7.0–8.0%. Domestic rates must track global ones to some degree to prevent capital outflows. For money with a priority on liquidity and safety over a horizon of less than one year, a fixed-term bank deposit continues to offer a stronger net yield than an open-ended bond fund once management fees are netted out.

Government bonds and bond funds present a more complicated picture. Longer-duration domestic government bond yields have moved up through the first half of 2026, but realized returns from open-ended bond funds in Q1 remained around 4.0% per annum, still trailing the Big 4 deposit rate. This is the direct arithmetic of a high global rate environment feeding through to domestic yield curves.

Equities face a double headwind: higher discount rates compressing valuations and sustained foreign net selling. Yet the VN-Index has held around the 1,915-point level as domestic retail flows have absorbed most of the foreign selling pressure. That resilience is real, but it is also finite if USD headwinds persist through the remainder of the year.

The Road to 2029 and Its Uncertainties

If global public debt reaches 100% of GDP by 2029 as the IMF projects, US Treasury yields are unlikely to fall quickly even through a Fed easing cycle. The logic is straightforward: the supply of US Treasuries will remain large, and term premiums will need to stay elevated to clear that supply. Three downstream implications follow for Vietnamese portfolios over that horizon: the cost of capital for Vietnamese companies is unlikely to return to the lows of 2020–2021 for several years; the USD/VND rate may continue its gradual, managed depreciation trend; and foreign investors could remain cautious sellers until the USD-VND yield differential narrows materially.

That said, the 100% global debt trajectory is not a certainty. If major economies implement meaningful fiscal consolidation earlier than expected, or if geopolitical pressures ease and defense spending plateaus, the path could flatten. Conversely, sustained defense spending increases and failure to reform entitlements in advanced economies could accelerate the timeline past 2029.

The Key Takeaway

The big picture is clear: Vietnam's 36% debt-to-GDP ratio is a genuine fiscal asset, providing the government with room to stimulate and reducing the risk of a domestic debt crisis. But that advantage does not translate into protection from global cost-of-capital pressures, because the transmission mechanism runs through the US dollar, not through domestic borrowing. This is the structural insight that investors often miss when they read reassuring headlines about Vietnam's safe public finances.

Capital flows are moving to the rhythm of USD interest rates, and that rhythm will only change when three signals shift simultaneously: a sustained decline in the 10-year US Treasury yield, stabilization or reversal in the USD/VND rate, and a shift in foreign investor behavior from net selling to net buying on HOSE. Until those three conditions are met together, the transmission channels described here remain fully operational, regardless of how sound Vietnam's own fiscal position may be.