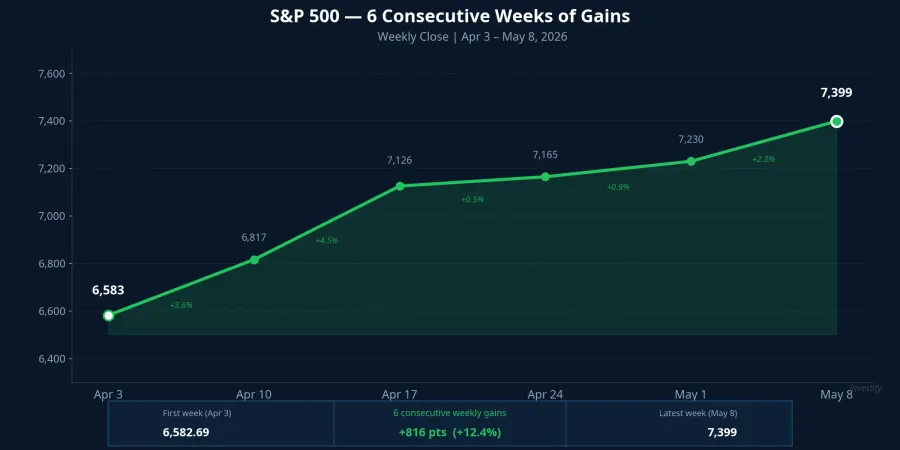

The S&P 500 closed the week of May 8, 2026 at 7,398.87 points, completing six consecutive weeks of gains from the 6,583 level.Business Insider The VN-Index stood at 1,915.37 points at the same time, a record high. Against that backdrop, the conventional wisdom writes itself: equities are running, gold is already expensive, no need for more defense.

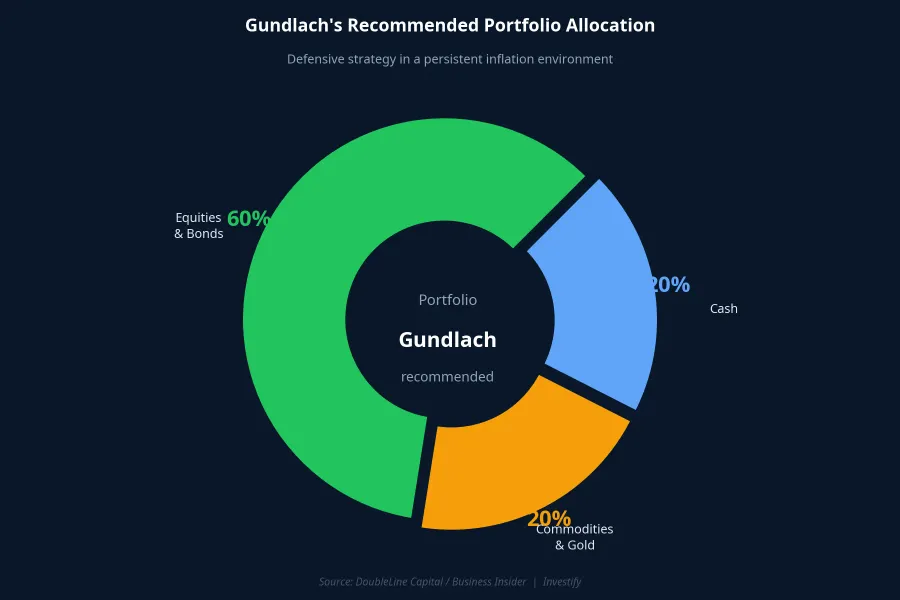

That same week, Jeffrey Gundlach, Founder and Chief Investment Officer of DoubleLine Capital, disclosed a portfolio that reads as the exact opposite: 20% cash, 20% hard commodities and gold.Business Insider A total of 40% sitting outside equities, precisely while U.S. markets are at record highs. DoubleLine manages approximately $93 billion in fixed income, placing Gundlach among the largest bond managers in the United States.Wikipedia

This is not a fringe view. Gundlach earned the title "new bond king" with his accurate call on the 2008 housing crisis. When someone in that position is aggressively raising defensive allocations while the market euphoria is building, the argument deserves serious attention.

Three Reasons Behind the 40% Defensive Allocation

Reason one: The Fed will not cut rates in 2026. This is a position Gundlach has restated repeatedly since early in the year, when market expectations were still floating around two to three cuts.CNBC The effective federal funds rate currently stands at 3.64%, well above the Fed's 2% inflation target. Core CPI for March 2026 came in at 2.6% year-over-year according to the Bureau of Labor Statistics, still above target. The disinflation process is stalling, leaving virtually no room for rate cuts.

Reason two: The real risk may lie in the opposite direction. If price indicators re-accelerate, the Fed not only won't cut but may be forced to tighten again.Pensions & Investments This is a scenario that equity markets have not priced in, and it is precisely why Gundlach is running an unusually high cash position. A 20% cash allocation functions both as a volatility buffer and as dry powder to deploy when genuine opportunities appear.

Reason three: Long-term USD weakness supports gold and hard commodities. Gold has risen from around $2,700 per ounce to above $4,721 per ounce over the past 12 months, a gain of approximately 75%. Gundlach raised his hard commodities allocation from roughly 10-15% previously to 20%,Business Insider a deliberate repositioning rather than a reactive trade. On gold specifically, he has said an allocation of up to 25% of the portfolio is "not unreasonable" in the current macro environment, and that he would be "buying with both hands" on any pullback toward $3,500 per ounce.

Defensive Is Not the Same as Bearish

The big picture reveals something important that requires careful reading: Gundlach is not forecasting an S&P 500 collapse, nor is he recommending a full exit from equities. The message is something different. Current macro risk structures are being underpriced by the market. A portfolio with 40% in capital-preservation assets will withstand a persistent inflation scenario far better than one fully concentrated in equities.

The distinction between defensive and bearish comes down to this. A defensive posture accepts giving up some upside if markets keep rising, in exchange for preserving capital if the bad scenario materializes. A bearish posture actively bets on the bad scenario. Gundlach is doing the first. Confusing the two leads to the wrong response to accurate information.

What Vietnamese Investors Can Take Away

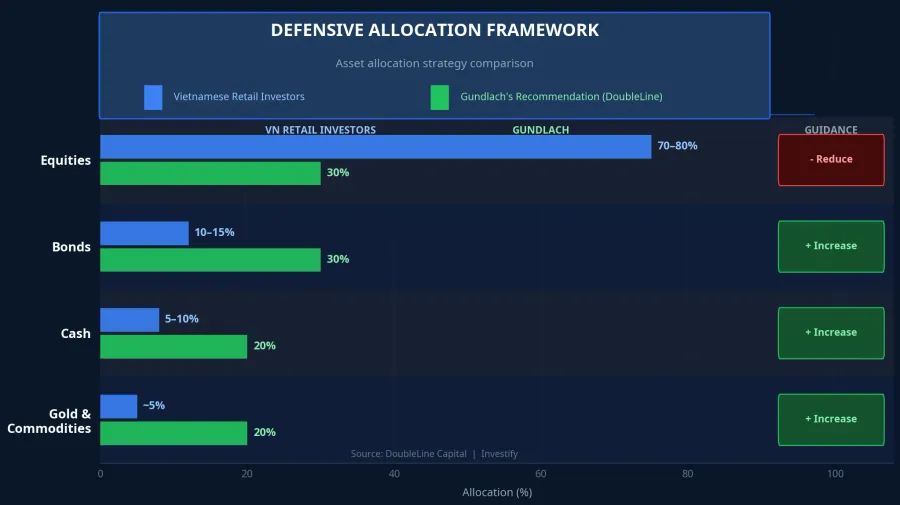

DoubleLine's framework cannot be imported directly into the Vietnamese market, given the differences in interest rate environment, product availability, and macro dynamics. But the three principles behind the decision are broadly applicable, with practical local adjustments.

On cash: Most Vietnamese retail investors currently hold very high equity concentrations, with cash typically at 5-10% of the portfolio. As the index approaches historical resistance levels, raising cash to 15-25% is a standard defensive posture for portfolios sitting on meaningful gains. This does not mean exiting entirely; it means creating flexibility to act when better entry points emerge.

On gold: Gold plays a distinct role in Vietnam. The gap between SJC pricing and the international spot price remains significant, though Decree 232/2025 has broken the SJC monopoly and a national gold exchange is being implemented. Access to physical gold at reasonable premiums is gradually improving. A 10-15% gold allocation in long-term portfolios is the range commonly referenced by personal finance advisory firms in Vietnam. Gundlach's 20% represents the upper end, appropriate for portfolios with a more defensive orientation.

On hard commodities: This is the asset class least used by Vietnamese retail investors, despite the legal framework being in place. Direct access is available through the Mercantile Exchange of Vietnam (MXV) via contracts in coffee, crude oil, and metals, or through fund certificates with commodity components. Even without direct exposure, holdings in commodity-extracting and commodity-exporting equities such as oil and gas, steel, and fertilizers provide indirect exposure to the global commodity cycle.

Key Signals to Watch

Gundlach's thesis rests on two data pillars: the pace of U.S. disinflation and Fed signaling. Both will either validate or invalidate the framework over the coming months.

If U.S. core CPI continues to hover above 2.5% in upcoming releases, the probability of a Fed hold (or even a rate hike) rises. In that environment, Gundlach's defensive framework has stronger grounding, and real assets such as gold and commodities continue to benefit. Conversely, if core CPI declines sustainably below 2.3% for two consecutive readings, rate-cut expectations will return, the USD may strengthen, and pressure on gold increases. In that case, a 40% defensive allocation becomes a significant opportunity cost against an equity-heavy portfolio.

This is a genuinely balanced call between two directions: not optimism or pessimism, but identifying the right decision point to monitor.

The big picture remains unchanged: in a cycle of persistent inflation with rates above target, a defensive asset allocation is a form of disciplined risk management. The real question is what level of defense fits a given portfolio, not whether to have any defense at all. The April 2026 core CPI release (expected May 12) and the June 2026 FOMC meeting are the two most important data points to reassess the framework.