Circular 26/2022/TT-SBV has been running exactly on schedule since it was issued in 2022. The rule: starting January 1, 2026, no portion of State Treasury deposits may count toward the LDR denominator at commercial banks. By the end of the week of May 10, the State Bank of Vietnam (SBV) confirmed the outcome: BIDV, VietinBank, Vietcombank, and Agribank are all operating with their LDR ratios pressing against the 85% regulatory ceiling.

This is not a signal of a credit surge or a sudden shortfall in deposit mobilization. Loan balances at the Big4 have not seen any sharp movement in recent months. What changed is the denominator: over VND 490,000 billion in Treasury deposits vanished from the formula at the same moment, pushing all four banks past the threshold even as the numerator barely moved. The week of May 11-15 is when the SBV is expected to shape its policy response. Whichever branch it chooses, savings deposit rates will follow.

The Technical Mechanism: Why VND 490,000B Creates a Warning

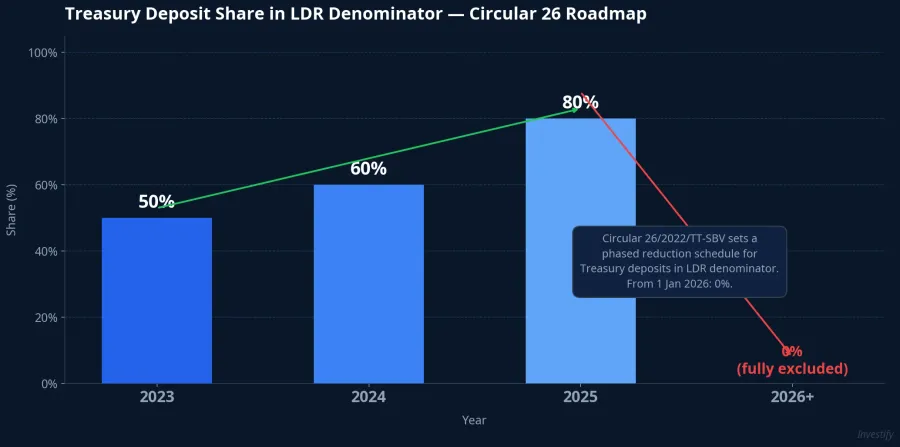

The LDR (Loan-to-Deposit Ratio) divides total outstanding loans by total mobilized funds. When it exceeds 85%, a bank is constrained from extending further credit until it either raises more deposits or receives a regulatory adjustment. Circular 26/2022/TT-SBV set a phased reduction schedule for the share of State Treasury deposits counted in the denominator: 50% in 2023, 60% in 2024, 80% in 2025, and 0% from January 1, 2026 onwards.VietnamBiz

The drop from 80% to 0% is the single largest step in the entire four-year roadmap, equivalent to removing all remaining Treasury balances from the formula in one move. In terms of actual deposit volumes: Vietcombank, BIDV, and VietinBank each hold approximately VND 134,000–136,000 billion in Treasury deposits; Agribank holds approximately VND 86,500 billion.DNSE Taken together, more than VND 490,000 billion was stripped from the LDR denominators of all four banks at the same time.

The credit growth backdrop makes the pressure more acute. System-wide credit grew 4.42% in the first four months of 2026, while VND deposit mobilization expanded at a notably slower pace.CafeF The Big4 simultaneously carry much of the country's national credit growth target, meaning the numerator keeps rising even as the denominator shrinks on a pre-set regulatory schedule.

Three Options on the SBV's Table Since April 9

On April 9, 2026, the SBV met with commercial banks and laid out three approaches to ease the LDR pressure.Báo Đầu Tư

The first option is to allow a partial recalculation of Treasury deposits back into the denominator, with a proposed level of approximately 20%, effectively extending a small portion of the 2025 treatment rather than cutting to zero abruptly. The second option is to broaden the components counted in the denominator to include long-term certificates of deposit (CDs) and long-term borrowings from international financial institutions. The third option is to raise the LDR ceiling from 85% to 87-90% for banks that maintain a sufficiently strong capital adequacy ratio (CAR).

The three options are not mutually exclusive, and the SBV may choose a combination. The critical point is that each option, whether applied alone or blended, leads to a different outcome for deposit rates, opportunities for savers, and credit supply to businesses.

Three Rate Branches for May 11-15

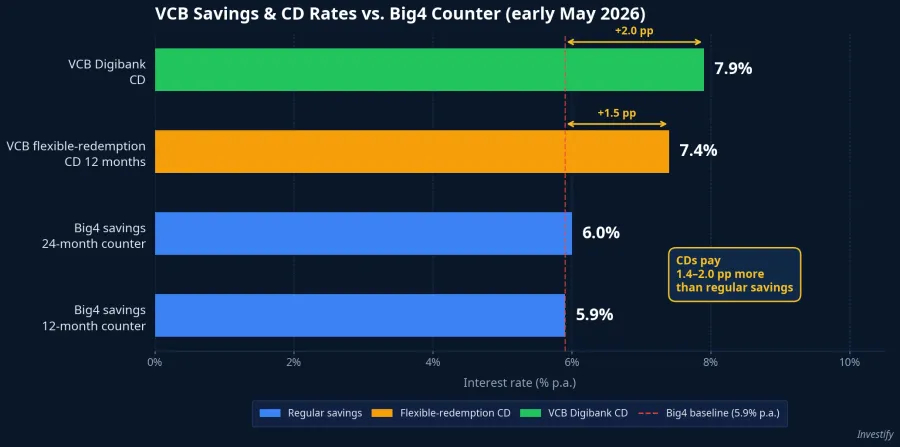

Branch A: SBV relaxes rules early in the week. If the SBV announces that 20% of Treasury deposits may count again, or raises the LDR ceiling to 87-90%, pressure is relieved almost immediately. The Big4 gain additional lending headroom without needing to push up funding costs. For savers, counter deposit rates would remain stable at current levels. The Big4 currently quote 5.9% p.a. for 12-month savings and 6.0% p.a. for 24-month savings at the counter.CafeF These levels are likely to serve as a near-term ceiling if Branch A materializes. Key signal: an official SBV announcement or a draft amendment to Circular 26 opened for public comment.

Branch B: Big4 self-fund, pushing up CD rates. If no official adjustment comes from the SBV, the Big4 will need to expand their denominators by issuing additional long-term CDs and bonds, precisely the direction of Option 2 from the April 9 meeting. Vietcombank already offers CDs via VCB Digibank at up to 7.9% p.a., and a flexible-redemption 12-month deposit product at 7.4% p.a.VietnamNet BIDV is also running a suite of fixed CDs with terms of 1 to 24 months. The spread between special CDs and regular counter savings currently sits at 1.4-2.0 percentage points; if Branch B persists, that gap is likely to widen further. Key signal: any Big4 bank registering a new CD issuance or raising rates on 24-36 month products during the week.

Branch C: Big4 slow credit, await policy clarity. If the SBV delays and the Big4 are unwilling to push up funding costs too quickly, the remaining option is to pause or decelerate new credit disbursement in selected segments while waiting for policy certainty. The consequence: credit growth slows in May, and small and medium-sized enterprises that rely on the Big4 face greater difficulty accessing short-term working capital. Key signal: unusually low credit figures in the first week of May, or reports from Big4 branches of tightened lending limits.

Reference Framework for Depositors

The three branches are not mutually exclusive. The most probable real-world outcome is a blended approach: the SBV allows a small portion of Treasury deposits to count again while simultaneously encouraging the Big4 to expand CD issuance. Such a combination leans toward Branch B in practice, because special CDs will continue to carry rates above regular counter savings.

This policy environment creates different choices depending on depositor needs and time horizons. For those with idle funds looking to place money this week: consider splitting the deposit between a short 3-6 month tranche to await clearer signals and a longer portion held for the CD opportunity if Branch B emerges. For those with savings maturing this week: avoid rolling over automatically at the same term. Wait for SBV and Big4 signals before deciding on the next tenor.

Three Signals to Watch: May 11-15

Whichever branch materializes first this week, savings rates will follow it. Three signals are worth tracking:

First, an official SBV announcement on adjusting Circular 26 or raising the LDR ceiling. This is the most decisive signal: it immediately determines whether Branch A is in play.

Second, any new CD issuance registered by a Big4 bank. If any one of the four announces a new issuance at a rate above current levels, that is clear evidence of Branch B.

Third, weekly credit data for early May. If credit growth comes in unusually weak relative to seasonal expectations, it is a sign that the Big4 are already executing Branch C while waiting for policy.

Circular 26 made January 1, 2026 an irreversible point of no return: the SBV and the banks have known this since 2022. The real question this week is not whether the pressure exists, but which path the SBV chooses to relieve it, and on what timeline.