In November 2016, the Vietnamese National Assembly passed Resolution 31/2016/QH14 with 92% of votes in favour, formally halting both Ninh Thuan nuclear power projects.VnExpress What made the decision distinctive was its stated rationale: the government's report explicitly noted that Russian and Japanese reactor technologies were among the world's most advanced, with high safety standards. The projects were suspended for macroeconomic reasons: capital had to be redirected to the North-South expressway, Long Thanh International Airport, and high-speed rail. A decade later, those same macroeconomic conditions have changed enough to reverse the policy entirely.

Why 2016 Conditions No Longer Apply

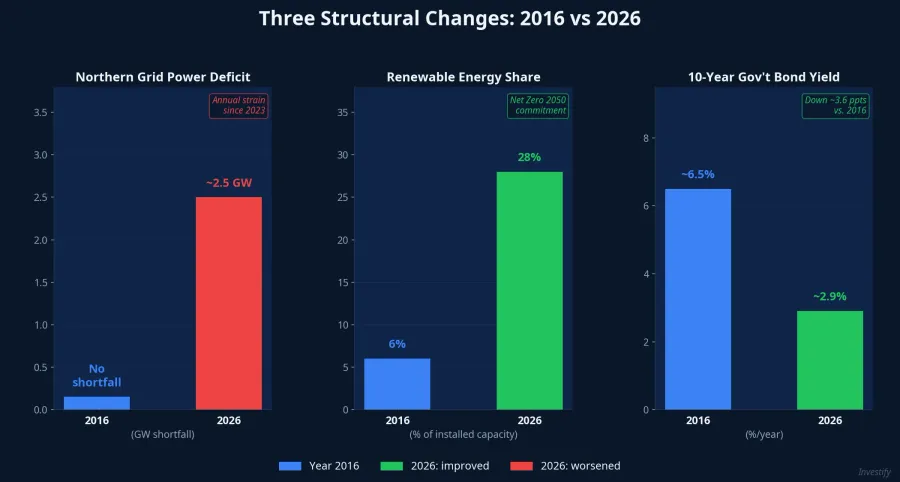

The reversal was not driven by a short-term political impulse but by three structural shifts that accumulated between 2021 and 2026.

First: a real power deficit has emerged. In 2016, Vietnam had surplus generation capacity; coal and hydro plants were sufficient to meet demand. By 2023, peak-season power strain in northern Vietnam became an annual event. Renewable capacity has expanded rapidly, but intermittent generation cannot substitute for baseload supply running 24/7. Nuclear power — with capacity factors above 90% — offers the one answer to a baseload gap that neither wind nor solar can close.

Second: the net-zero commitment has effectively closed the door on coal. After COP26 in 2021, international lenders and FDI investors largely withdrew financing from new coal projects. Gas-fired LNG generation is expensive and exposed to volatile international fuel prices. Nuclear power, with lifecycle emissions comparable to onshore wind, emerged as one of the few baseload options compatible with Vietnam's net-zero 2050 pathway.

Third: long-term capital costs have fallen substantially. Vietnam's 10-year government bond yield stood at approximately 6.5% in 2016. By 2026, the rate has come down to around 2.9%. For a capital-intensive, 60-year-lifetime project like a nuclear power plant, a nearly 4-percentage-point reduction in the cost of capital can fundamentally transform project economics. A project that looked marginal at 6.5% can look attractive at 2.9%.

The Legal Path to Restart

The policy reversal unfolded through a sequence of decisions over roughly 16 months. On 25 November 2024, the Party's 13th Central Committee plenum reached consensus on resuming the nuclear programme.Government Portal In late November 2024, the 15th National Assembly's 8th session approved resuming investment. On 19 February 2025, Resolution 189/2025/QH15 established a special implementation framework: direct procurement, exemptions from certain regulatory reviews, and the right to advance up to 50% of land compensation payments before the National Assembly approves final unit costs.Bao Phap Luat

EVN (Vietnam Electricity) was assigned as investor and developer for Ninh Thuan 1; PetroVietnam for Ninh Thuan 2.

Rosatom and the VVER-1200 Technology

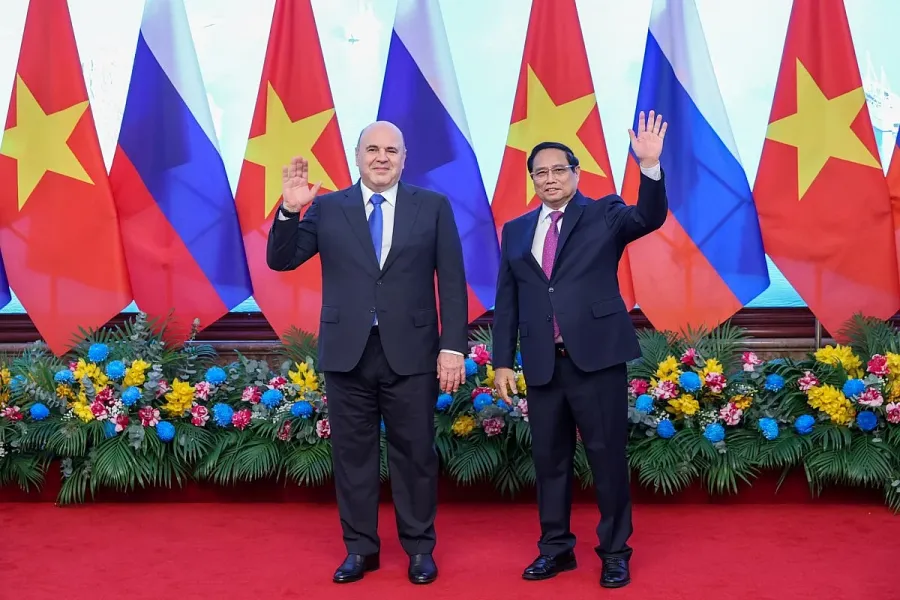

The original 2009 partnership structure paired Rosatom for Ninh Thuan 1 and a Japanese consortium for Ninh Thuan 2. After a decade, only half of that arrangement survived. On 23 March 2026 in Hanoi, Prime Minister Pham Minh Chinh and Russian Prime Minister Mikhail Mishustin jointly witnessed the signing of an intergovernmental agreement for the construction of Ninh Thuan 1 Nuclear Power Plant.Tuoi Tre The chosen technology is Rosatom's VVER-1200, comprising two reactor units with a combined capacity of approximately 2,400 MW.

The Japanese partnership for Ninh Thuan 2 was formally terminated in January 2026. Khanh Hoa province continues to proceed with land clearance at both plant sites in parallel. A new partner selection process for Ninh Thuan 2 is expected in a subsequent phase.

The June 30 Land Clearance Sprint

The Ninh Thuan 1 plant site covers approximately 449 hectares and affects 835 households and parcels. The approved budget for land acquisition and resettlement stands at VND 6,699 billion, comprising VND 5,280 billion in compensation and approximately VND 1,082 billion for resettlement construction.Nha Dau Tu

As of early May 2026, local authorities had confirmed land origin for 100% of affected cases. Compensation plans have been formally approved for 154 cases covering 122.1 hectares, totalling VND 168.2 billion. Of those, actual disbursements have been made to 18 households amounting to approximately VND 82 billion.Thanh Nien The 30 June 2026 handover deadline places significant pressure on the remaining 681 cases still awaiting approved compensation plans.

Special support measures include monthly housing subsidies of VND 5 million for displaced households until they receive replacement land or housing, with an additional six months if resettlement is on allocated land. If land handover is completed on schedule by Q2 2026, construction work could begin within the year.

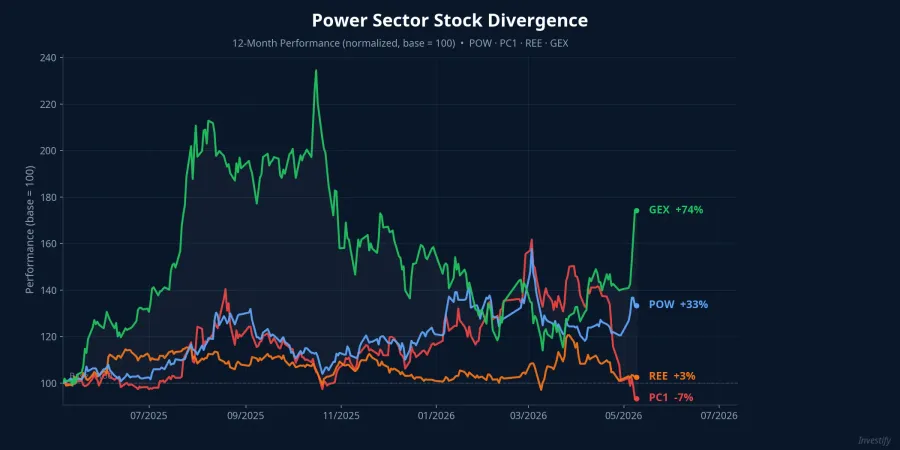

Four Tickers, Four Different Stories

The past 12 months of trading reveal that the market is pricing each stock on its own logic, rather than applying a uniform "nuclear beneficiary" premium across the sector.

POW closed at VND 14,000 on 9 May, up 33.4% over 12 months. Trading volume surged in March 2026, just ahead of the intergovernmental agreement signing. Market expectation is that EVN — the designated developer of Ninh Thuan 1 — may involve POW in project operations or enter into a long-term power purchase agreement (PPA) once the plant is operational. The 33% gain reflects that expectation; it does not guarantee the timeline will hold.

PC1 closed at VND 18,100, down 6.7% over 12 months and down sharply 32.2% in the past month. Near-term pressure stems from multiple share issuances in 2026, creating dilution. The paradox is that PC1 is the ticker most directly sensitive to EPC contract announcements once construction genuinely begins. Current backlog stands at approximately VND 7,000 billion, with profit margins on some segments reaching 18–23% in Q4 2025. Dilution weighs on the near-term price, but EPC contract awards could shift that equation.

REE closed at VND 61,000, essentially flat over 12 months (+2.6%). REE benefits indirectly through M&E systems and auxiliary grid infrastructure around the plant, not from the nuclear project directly, but as a practical execution partner when the South-Central transmission network is built out.

GEX closed at VND 33,500, up 74.1% over 12 months. The bulk of that gain, however, traces back to an internal restructuring cycle and the electrical equipment businesses (Cadivi, Thibidi), which benefit from the broader grid investment wave. Nuclear is a supportive backdrop, but not the direct driver of GEX's 74% appreciation.

The Roadmap and Key Milestones to Watch

The standard construction timeline for a nuclear power plant runs 7–10 years from land handover to first commercial operation. If the Ninh Thuan 1 site is fully cleared by Q2 2026 and EPC contracts are signed, the first reactor unit is expected to reach commercial operation somewhere in the 2032–2035 window.

That timeline is fundamentally different from the typical short-term investment cycle. Over the next three to five years, stock market performance in this sector will track specific milestones: the outcome of the 30 June land handover, feasibility study approvals, detailed EPC tender announcements, capital allocation for the 500 kV transmission network across the South-Central region, and the selection of a new partner for Ninh Thuan 2. Each of these serves as a reality check for expectations currently priced into the market.

The greatest risk is not another policy reversal. The three structural shifts that drove the restart remain firmly in place. The real risk lies in execution speed and cost: 681 cases pending compensation approval, foreign currency exposure embedded in international EPC contracts, and multi-stage regulatory approvals for each technical phase of construction. Equity dilution to fund capital expenditure is a persistent risk for EPC-linked stocks, as PC1 is currently demonstrating.

Investors in power sector equities should distinguish clearly between two groups: those where long-term expectations are already reflected in the share price (POW, GEX), and those where actual contract awards and construction milestones remain uncertain (PC1). The risk-return profile across these two groups differs considerably depending on where the project stands in its development cycle.