In 2026, Vietnamese securities firms have registered to add approximately VND 100,000 billion in charter capital, the single largest annual capital raise in the industry's history.BaoMoi The number itself is striking, but the more important question is why. This is not a growth wave driven by a sudden market boom or shareholder pressure. Three structural constraints have converged at once: margin lending balances approaching the legal ceiling, a new circular that compresses available capital ratios, and a decree that, for the first time, opens securities firms to 100% foreign ownership.

Who Is Leading the Wave?

SSI plans to raise approximately VND 9,262 billion, pushing its charter capital above VND 30,000 billion and making it the first Vietnamese broker to cross that threshold.CafeF VIX is issuing rights to existing shareholders at a 10:6 ratio, priced at VND 12,000 per share, targeting proceeds of over VND 11,000 billion to lift its charter capital above VND 24,500 billion. VCK is targeting an increase of approximately VND 9,131 billion, primarily from retained equity.

Together, these three firms account for roughly VND 28,000 billion of the total wave, with the remainder distributed among HCM, MBS, TCBS, and smaller brokers. Notably, all three have capital plans within VND 131 billion of each other — a gap of less than 1.5% — suggesting they are responding to the same set of binding constraints rather than competing for market share.

On the market, SSI shares closed the latest trading week at VND 28,300, implying a market cap of VND 70,500 billion. That price still lags SSI's earlier-year peak even as VN-Index set a new all-time high of 1,915.37 points on May 9, 2026. The gap reflects the market's caution about dilution risk accompanying the large-scale issuances.

Pressure One: The 200% Equity Ceiling

Decree 155/2020/ND-CP caps each securities firm's margin lending balance at no more than 200% of its equity. The mechanics are straightforward: a firm with VND 10,000 billion in equity cannot extend more than VND 20,000 billion in margin loans. Once that ceiling is hit, the only way to grow the lending book is to grow equity first.

At end of Q1/2026, total market-wide lending reached an estimated VND 415,000 billion, with margin lending specifically at approximately VND 405,000 billion, the highest level on record.Stockbiz Five firms surpassed the USD 1 billion threshold: TCBS, SSI, VPBankS, VPS, and HSC. TCBS leads with approximately VND 45,000 billion; VPBankS exceeded VND 36,000 billion following its sixth consecutive quarter of balance growth.Vietstock

For the firms in this group, capital raising is no longer a strategic choice but a prerequisite for maintaining their core brokerage business.

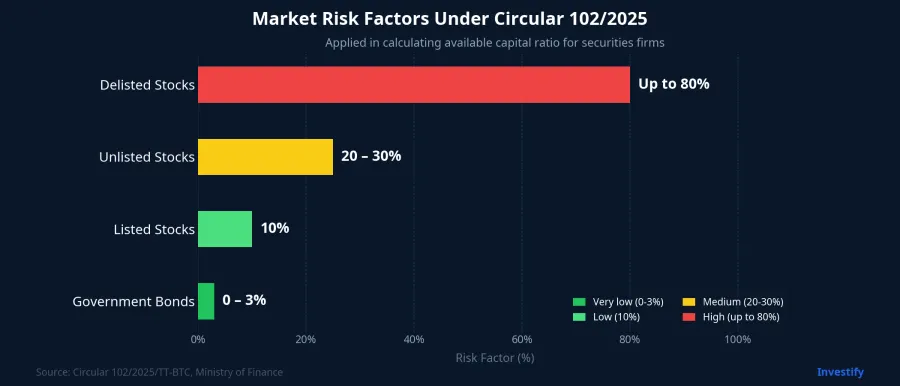

Pressure Two: Circular 102/2025 Compresses Available Capital

The Ministry of Finance issued Circular 102/2025/TT-BTC on October 29, 2025, with effect from December 15, 2025, subject to a six-month transition period.CafeF The circular revises the market risk factors applied in computing the available capital ratio for securities firms, with clearly differentiated weightings by asset class.

The mechanism works as follows. Available capital equals equity minus deductions and risk provisions, where provisions are computed as asset values multiplied by their respective risk factors. When risk factors increase, provisions increase, which pulls the available capital ratio down. To keep that ratio above the regulatory floor, a firm must either trim its risky positions or inject more equity. For firms carrying large books of unlisted stocks, proprietary trading portfolios, or margin loans against unlisted securities, the faster solution is a capital raise.

This explains why issuance plans clustered around the AGM season of April to May 2026. The six-month transition starting December 15, 2025 places a soft deadline in mid-year, and firms needed their issuances approved before that window closed.

Pressure Three: Decree 245/2025 Opens 100% Foreign Ownership

Decree 245/2025/ND-CP, signed September 11, 2025, amends Decree 155/2020 by removing the provision that allowed listed companies to self-impose a foreign ownership cap lower than the statutory maximum.Government For securities firms, this opens a real path for international institutional investors to participate in private placements at up to 100% ownership, the first time in the industry's history.

Previously, a broker wanting to raise thousands of billions of dong in a single year was largely limited to three channels: rights issues for existing shareholders, bonus shares, and ESOP allocations. All three depend entirely on domestic shareholder absorption capacity. With foreign room now fully open, the private placement channel becomes a genuine alternative. TCBS is the first firm to receive approval under this new framework.

The first two pressures (margin near the ceiling, higher risk factors) establish the necessity to raise capital. Decree 245 supplies the mechanism to do it more efficiently, reducing internal dilution pressure and creating pathways to long-term strategic partners from abroad.

Two Perspectives for Investors

For individual investors who use margin, this capital wave materially expands lending headroom. With SSI alone raising equity to approximately VND 30,000 billion, the 200% ceiling translates to VND 60,000 billion in additional lending capacity. Aggregated across the industry once all issuances close, the sector's total margin capacity could increase substantially, sufficient to absorb the larger flows expected when Vietnam's FTSE EM upgrade takes effect in September 2026.

For shareholders of listed brokers, the picture is more nuanced. When charter capital grows faster than earnings, EPS is diluted, and valuations face pressure if firms cannot deploy the new capital productively. The market is likely to bifurcate. Firms with stable brokerage market share, healthy margin utilization rates, and growing investment banking revenue will absorb the dilution. Firms that raised capital primarily to satisfy regulatory ratios without expanding underlying business activity will likely trade at a discount relative to their pre-issuance levels.

There is also a near-term market risk worth noting. When multiple brokers issue rights in the same few-month window, the supply of new shares creates additional short-term price volatility. For tickers where issuance size represents 40 to 50% of the pre-raise capital base, the wave of new shares hitting accounts simultaneously with bonus shares and ESOP allocations can weigh on prices in the weeks immediately following the ex-rights date.

Signals Worth Watching

The Q2/2026 earnings report will be the first real test of how efficiently new capital is being deployed. Three ratios are worth tracking to distinguish the winners from the laggards in this cycle.

The first is the capital absorption rate into actual margin lending, measured as margin balance divided by post-issuance equity. Firms that return this ratio close to 200% within one to two quarters will have a clear net interest margin advantage. The second is the proportion of new capital raised through private placements to foreign strategic investors relative to total capital added. This channel dilutes existing shareholders less than broad rights issues and brings in long-term committed partners. The third is post-dilution EPS compared year-on-year, particularly relative to broker research consensus forecasts. If EPS falls materially below expectations, the market will reprice the entire sector group.

While waiting for Q2 data, investors holding broker stocks should track rights exercise ratios at each open issuance. This is an early indicator of how much confidence existing shareholders have in each firm's ability to deploy capital effectively. A high exercise rate signals market acceptance of the plan; a low rate is a signal to revisit the investment thesis.