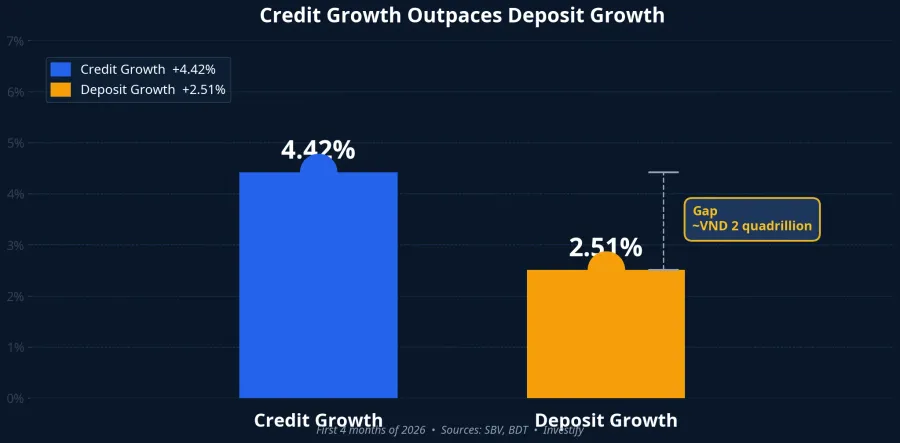

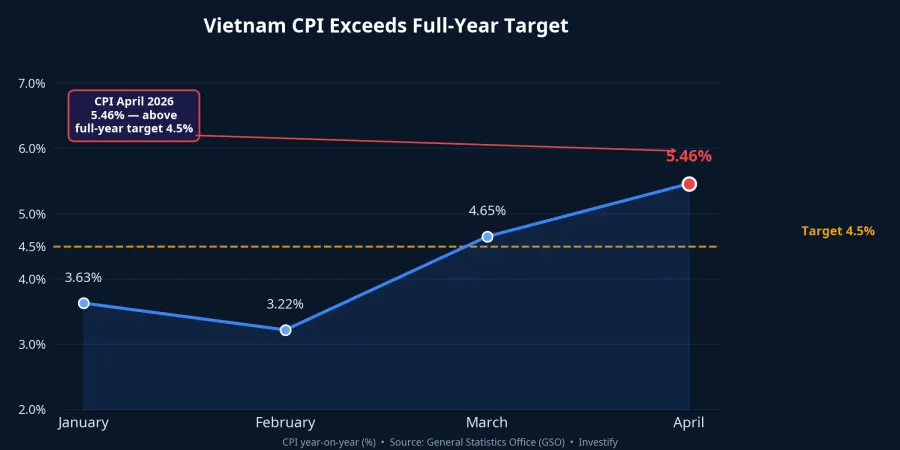

Three data points arrived together in the April 2026 report. Total outstanding credit in the economy exceeded VND 19.4 quadrillion, up 4.42% from end-2025 and 18.26% year-on-year.Fili VND deposit balances fell short of credit by roughly VND 2 quadrillion, meaning deposit growth has been consistently outrun by credit expansion.Báo Đầu tư And April CPI climbed to 5.46% year-on-year, above March's 4.65% and beyond the 4.5% full-year ceiling set by the National Assembly.24hmoney

These three figures do not stand in isolation. When credit races ahead of funding inflows, banks must scramble for liquidity. When actual inflation overshoots the SBV's 4.5% policy rate, room for further monetary easing narrows sharply. These are the starting conditions for three scenarios now shaping Vietnam's interest rate landscape over the next four to six weeks.

What the VND 2 Quadrillion Gap Is Telling Us

The VND 2 quadrillion "shortfall" does not mean the banking system is technically cash-strapped, since banks have other funding channels including interbank borrowing, bond issuance, and foreign currency deposits. The real message, however, is this: household and corporate deposits — the most stable and cheapest funding source in the system — are not keeping pace with loan demand.

Money is migrating to other channels. Margin debt across the stock market surpassed VND 400,000 billion, hitting an all-time high.CafeF The number of brokerage accounts reached 12.66 million at the end of Q1 2026, adding roughly 800,000 accounts in just three months.Nhân Dân With actual inflation now exceeding the Big 4 banks' 12-month deposit rates of 5.8–6.5% per annum, depositors have reason to consider reallocating a portion of savings to gold or bonds.

Inflation Is Closing the Door on Easing

The April CPI reading of 5.46% year-on-year is a significant signal for monetary policy. In March, CPI stood at 4.65%, already close to the target ceiling. One month later, the figure punched through 5% and set a new pressure zone. This means the SBV cannot simultaneously hold the policy rate at 4.5% as planned — UOB forecasts it will stay there for all of 2026 — let the credit-deposit gap widen further, and watch inflation push higher. One of the three variables has to move.

The VN-Index closed on 8 May 2026 at 1,915.37 points, a new all-time high. That figure reflects a reality: part of the money that would ordinarily flow into bank savings is sitting in equities instead. A market at record highs also raises questions about whether loan demand can maintain its current pace if investor sentiment turns.

Three Scenarios Now Taking Shape

Scenario 1: Deposit Rates Nudge Higher to Attract Funds Back

This is the most straightforward market reflex when funding inflows fail to keep up with lending demand. Individual banks will raise their deposit rates to compete for retail savings rather than wait for the SBV to adjust the policy rate. Early signals have already appeared in certificate-of-deposit segments and bank bond issuance in early May.

This scenario becomes more pronounced if interbank liquidity remains tight or May CPI fails to cool from 5.46%. In that case, the Big 4's 12-month deposit rate floor could nudge from the 5.0–5.5% range toward 6.0%, while smaller private banks continue anchoring at 7.0–8.0% to retain their funding base. For savers with 3- to 6-month deposits, locking in rates before this adjustment would mean missing the upside. For equities, a 50–100 basis point rate nudge typically creates short-term pressure on high-valuation and leveraged names, but is unlikely to reverse the trend outright.

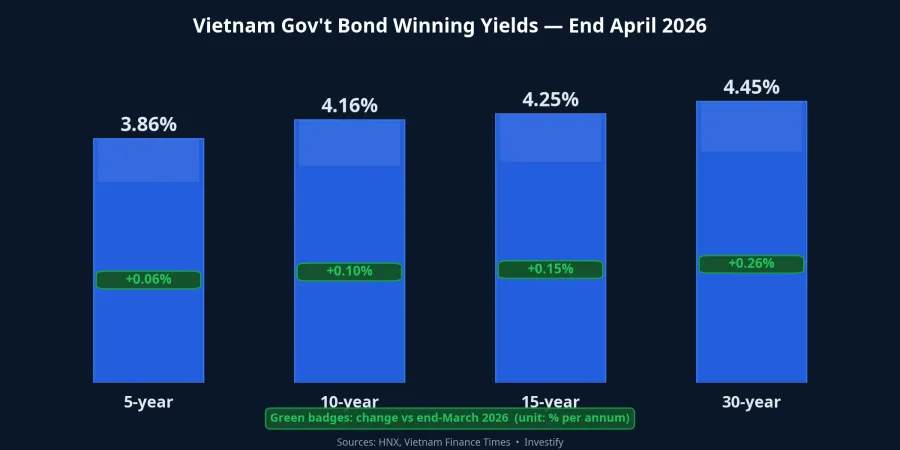

Scenario 2: Government Bonds Absorb Institutional Capital and Long-End Yields Drift Up

This channel is already being activated most visibly. In April, government bond auction yields for the 5-, 10-, 15-, and 30-year maturities rose 5–26 basis points versus end-March, landing at 3.86%, 4.16%, 4.25%, and 4.45% per annum respectively.Thời báo TCVN April's winning volume reached VND 45,455 billion, 2.32 times March's level. Over the first four months of the year, the State Treasury has raised approximately VND 125,556 billion.Saigon Times

The State Treasury is both borrowing more and accepting higher rates to get the job done. With roughly 75% of the full-year supply still unissued after four months, the pressure is real. If long-end yields continue drifting toward the Big 4's 12-month deposit rate floor, institutional money from insurers, bond funds, and bank proprietary desks will gradually shift into this channel. For retail investors, direct government bonds remain difficult to access due to lot sizes and low secondary-market liquidity, but open-ended bond funds will reflect this dynamic through their NAV.Saigon Times In a rising government bond yield environment, NAV faces short-term pressure but the forward yield-to-maturity improves: this is a better entry point for new buyers than for those already holding.

Scenario 3: Credit Growth Slows Naturally as Borrowing Demand Softens

This scenario receives less attention but has a higher probability than many expect. A 4.42% four-month credit growth rate is only the warm-up lap toward the SBV's 15% full-year target. In the second half of the year, once public investment disbursement demand has been largely met and real estate demand has yet to stage a clear recovery, credit growth could decelerate on its own.

Triggers worth watching: manufacturing PMI falling below 50, retail sales stalling, and a slowdown in new credit signings for real estate and consumer goods in May and June. If that happens, funding pressure on banks would ease, deposit rates would not need to climb, and the SBV could maintain its pro-growth stance. This is the favorable scenario for equities but not for savers hoping for higher deposit returns.

The Three Scenarios Are Not Mutually Exclusive

Reality is rarely a binary choice. The picture could be a blend: deposit rates nudge up modestly at some private banks (Scenario 1), government bonds continue absorbing institutional capital while long-end yields edge higher (Scenario 2), and aggregate credit growth begins decelerating from June onwards (Scenario 3). Whichever signal arrives first will shape how the broader picture is read.

It is also worth acknowledging an alternative explanation: the VND 2 quadrillion gap could be filled gradually by faster-moving funding sources — bank bond issuance, interbank borrowing, or offshore loans — without necessarily pushing retail deposit rates higher.Báo Mới The evidence is that Big 4 bank bond issuance activity in early May has been brisk. That said, bank bonds carry their own cost and ultimately compress net interest margins (NIM). The question of funding cost is shifted rather than solved.

Allocation Framework and Signals to Watch

In a multi-scenario environment like this, the commonly cited approach is to segment capital by time horizon rather than concentrate it in one channel. For capital needed within six months: prioritize liquidity with Big 4 savings accounts or short-tenor certificates of deposit. For capital with a 6- to 24-month horizon: consider fixed-rate products (yields of approximately 8–11% per annum depending on the issuer) or open-ended bond funds. This is the tranche that benefits most if Scenarios 1 and 2 materialize. For capital with a 3-year-plus horizon: equities and fund certificates, accepting near-term volatility in exchange for a long-run return expectation above inflation. Note that this is a broadly cited reference framework, not personalized investment advice.

The big picture shows the SBV facing genuine dual pressure: credit must flow adequately to support growth, but inflation is narrowing the margin to do so cheaply. Among the three scenarios, Scenarios 1 and 2 currently have more supporting evidence than Scenario 3 in the near term. Three specific numbers are worth tracking over the next few weeks: the 10-year government bond auction yield in the third week of May (versus 4.16% at end-April); May CPI from the General Statistics Office; and the 12-month deposit rates posted by Vietcombank, BIDV, VietinBank, and Agribank. Those three readings will reveal which scenario is actually entering the real economy, and at what speed.