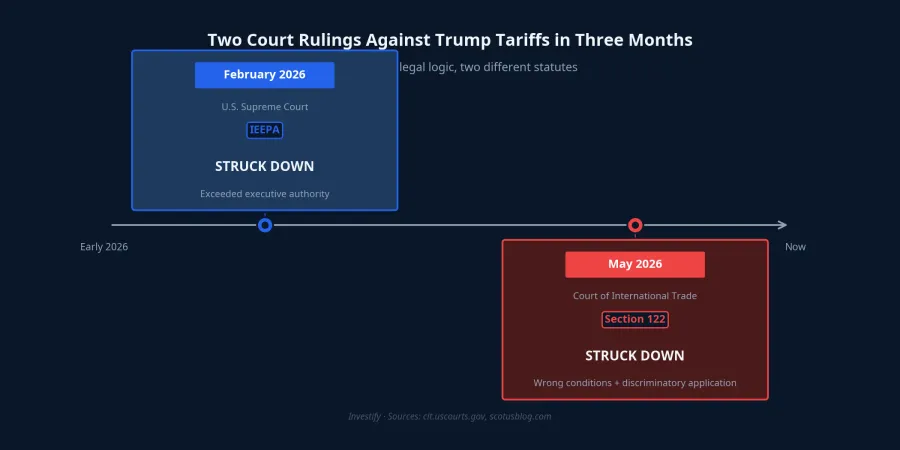

On the night of May 7, 2026, the U.S. Court of International Trade (CIT) ruled 2-1 that President Donald Trump's global 10% tariff, imposed under Section 122 of the Trade Act of 1974, was unlawful and exceeded presidential authority. The S&P 500 closed down just 0.4% that session. Vietnam's VN-Index hit a fresh all-time high of 1,909.01 points while the ruling was being handed down in Washington.

Wall Street's silence wasn't ignorance. It was an accurate read: the ruling was narrow, the tariff remained in force. But reading one ruling correctly and reading the trend across two consecutive rulings are two very different things. The bigger picture reveals what a single trading session cannot.

Why the Court Struck It Down

Section 122 of the Trade Act of 1974 grants the president authority to impose temporary tariffs of up to 15% for up to 150 days, but only under one narrow condition: a serious balance-of-payments crisis or the risk of a rapid dollar depreciation. The CIT's three-judge panel argued that the administration conflated a routine trade deficit with a balance-of-payments deficit: two concepts that are fundamentally different in legal meaning. Tariffs designed to rebalance ordinary trade flows do not meet Section 122's trigger conditions.

The court also identified a procedural flaw: the 10% tariff exempted goods from Canada, Mexico, Costa Rica, and several Central American countries, while Section 122 requires uniform global application. The discriminatory structure contradicted the plain language of the statute.

Critically for the market reaction: the court only suspended the tariff for the two named plaintiffs, a toy company and a spice importer, both in Washington State. Only they had demonstrated direct harm and legal standing to sue. There was no nationwide injunction. U.S. customs continues to collect the 10% tariff on virtually all imports, including Vietnamese goods.

Wall Street Read the Technical Correctly

The S&P 500 fell 0.4% on May 7 primarily because of profit-taking after the index had touched 7,365 points the previous session. The legal news played a secondary role. The DXY dollar index held steady near 97.83. The VN-Index's record close at 1,909.01 confirmed that Vietnamese markets read the ruling the same way as Wall Street.

That was the correct response to a technically narrow, limited-scope ruling. Wall Street didn't panic because there was nothing to panic about in the immediate term. But that's also precisely where the bigger picture begins to matter.

Two Rulings, One Legal Trend

In February 2026, the Supreme Court struck down tariffs imposed under IEEPA, ruling that the president had exceeded executive authority. In May 2026, the CIT struck down tariffs under Section 122 with the same core reasoning: Congress has not granted the executive branch the power to unilaterally define extraordinary economic conditions to impose sweeping universal tariffs in this manner. Two rulings, two different statutes, one consistent legal direction.

That core logic has now held across two different courts on two different statutory bases. Each time the White House switches its legal foundation, courts apply the same limit. This is a structural signal, not an isolated event.

The Justice Department is expected to appeal to the U.S. Court of Appeals for the Federal Circuit, an institution that has repeatedly struck down executive tariff policies in past administrations. Beyond the Federal Circuit, the matter could escalate to the Supreme Court if constitutional questions arise. This is a sustained legal erosion process, not a one-session conflict.

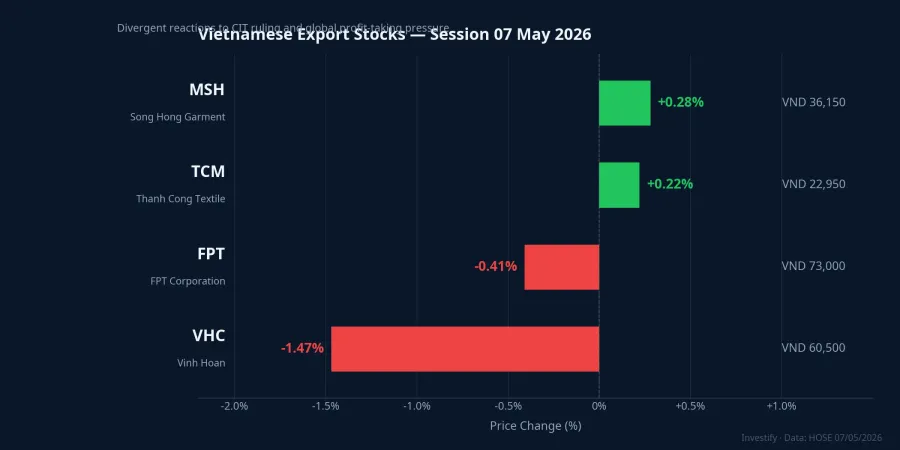

Four Stocks, Four Stories

Capital flows are shifting in proportion to each stock's sensitivity to this legal signal. Four major export names tell four distinct stories.

VHC (Vinh Hoan, seafood) closed at VND 60,500, down 1.47%. Vietnamese seafood exports to the U.S. declined during Q1 2026 as companies redirected shipments to China and other markets. Tariff risk has been priced in gradually over multiple quarters. The CIT ruling did not introduce a new shock for VHC.

MSH (Song Hong Garment) edged up 0.28% to VND 36,150. MSH's revenue is heavily dependent on U.S. orders, yet the session showed no unusual pressure. MSH is the clearest beneficiary if tariff exemptions are broadened through subsequent appeals.

TCM (Thanh Cong Textile) was nearly flat at VND 22,950, up 0.22%. Its vertically integrated spinning-weaving-sewing supply chain gives TCM better cost flexibility than pure contract manufacturers. This is a structural advantage when the legal environment remains unsettled.

FPT closed at VND 73,000, down 0.41%, with net foreign selling of approximately VND 372 billion, the largest on HOSE that session. FPT does not export physical goods to the U.S. and is not directly subject to the 10% tariff, but foreign capital flows are responding to broad global macro risk aversion rather than company-specific risk.

Two Layers of Signal

The accurate picture is neither "tariffs are locked in, just adapt" nor "tariffs are about to be reversed." The tariff's legal foundation has been struck down twice, and the executive branch's legal room to maneuver is narrowing. But the pace is slow and each ruling remains narrow in scope. Tariffs are still being collected every day, while the probability of broader suspension over the next 12-18 months rises with each new ruling.

For positions in U.S.-exposed Vietnamese export stocks, two distinct signal layers need to be read in parallel.

Short-term signal (1-3 months): the 10% tariff is fully in effect. Q2 2026 earnings from exporters will reflect that reality. Companies that redirected orders — like VHC's pivot toward China — or those with integrated supply chains like TCM face less pressure than direct U.S.-dependent manufacturers.

Medium-term signal (6-18 months): each appellate round may widen the scope of exemptions. The Federal Circuit's hearing schedule is the most important event to monitor. If exemptions are broadened, U.S.-dependent garment makers like MSH stand to benefit most clearly. If the appeal succeeds in preserving the tariff, the current risk structure persists.

Reading Correctly vs. Reading Completely

Wall Street's silence on May 7 wasn't about being uninformed. It was about correctly reading the technical scope of a narrow ruling. That was an accurate call. What Wall Street did not need to react to was the cumulative legal trend across two consecutive rulings. That is a 6-18 month risk horizon, not a single-session event.

For Vietnamese investors holding U.S.-exposed export stocks over that timeframe, the next step is not a judgment today. The next step is tracking the Justice Department's Federal Circuit appeal timeline. When the appellate court rules, the short-term and medium-term questions will have much clearer answers.