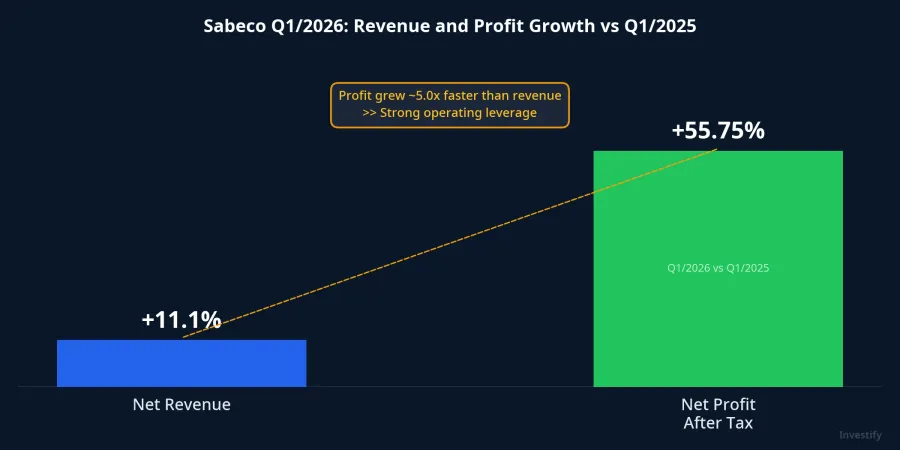

Sabeco's Q1/2026 net revenue came in at VND 6,457 billion, up 11.1% year-over-year. Net profit after tax reached VND 1,245 billion, up 55.75%.CafeF Looking at these two figures, the natural question is: how does revenue growing 11% translate into profit growing 56%? The gap cannot be explained simply by selling more beer.

The answer lies in two mechanisms running simultaneously within one financial report. Understanding each one separately gives a clearer picture of Sabeco's outlook than reading the headline number alone.

Mechanism 1: Cost of Goods Nearly Stood Still

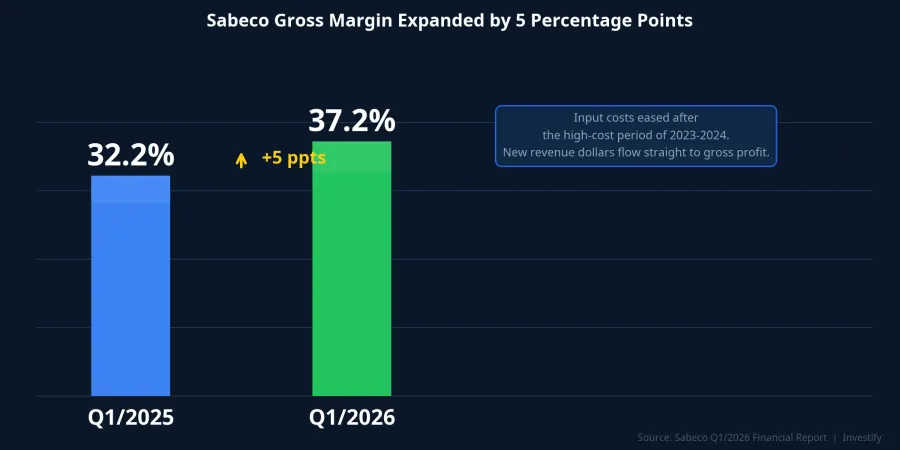

Cost of goods sold in Q1 rose just 2.88%, from VND 3,938 billion to VND 4,052 billion. Revenue, meanwhile, grew 11.1%. This divergence means most of the incremental revenue was not absorbed by production costs and flowed directly into gross profit. Gross profit reached VND 2,405 billion, up 28.47%, while the gross margin expanded from approximately 32.2% to 37.2%.

A five-percentage-point gross margin expansion in a single quarter is a meaningful improvement for a mature consumer goods company. It reflects two realities converging at once: input costs such as barley, aluminum cans, and sugar have cooled from the elevated levels of 2023–2024, and Sabeco has room to push through price increases or shift its product mix toward higher-margin segments. This is the "real beer recovery" component that investors should parse separately from everything else.

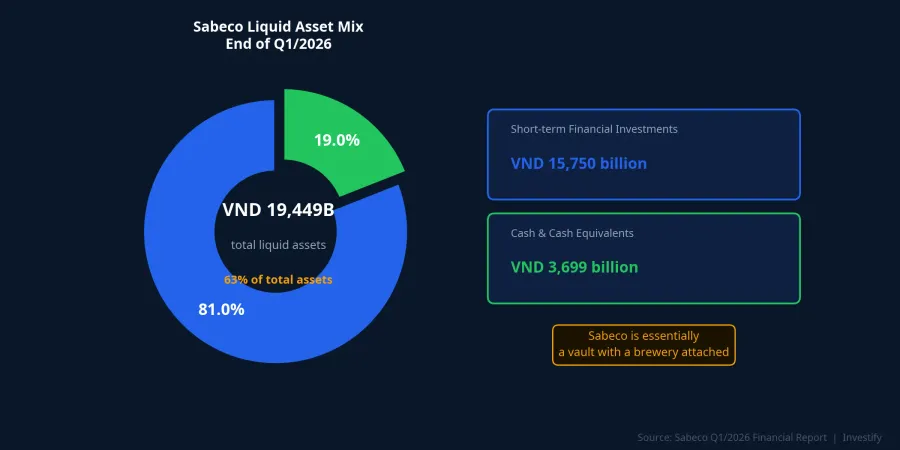

Mechanism 2: VND 16,000 Billion in Deposits Generating Returns

At the end of Q1/2026, Sabeco held approximately VND 15,750 billion in short-term financial investments, primarily fixed-term bank deposits, along with VND 3,699 billion in cash and cash equivalents. Total liquid assets reached nearly VND 19,449 billion, equivalent to approximately 63% of total assets. By structure, Sabeco operates more like a large cash vault with a brewery attached than the reverse.

That deposit base generated approximately VND 260 billion in financial income during Q1.Bao Phap Luat Against total net profit of VND 1,245 billion, deposit interest contributed roughly 17% after corporate income tax. It is not the primary profit driver, but it is a substantial buffer that has nothing to do with selling beer.

Combining Both: Decoding the Revenue-Profit Gap

Placing the numbers side by side gives a fuller picture. The year-over-year profit increase was VND 446 billion, rising from VND 800 billion to VND 1,245 billion. Of this, gross margin expansion contributed approximately VND 280–300 billion; net financial income contributed the rest. The core beer business remains the primary driver, but deposit interest pushed the total up by a meaningful increment.

This is also why the operating leverage appears so dramatic at the headline level: revenue up 11% pulling profit up 56%. Disaggregated, the operating leverage from the beer business is closer to 35%, with the remaining roughly 20 percentage points coming from the non-beer component. These two growth sources operate through different mechanisms and carry different risk profiles.

Progress Against the 2026 Plan

Sabeco set its 2026 targets at VND 28,959 billion in revenue and VND 4,937 billion in net profit after tax, representing 8% growth over the prior year.Tin Nhanh Chung Khoan After Q1, the company had completed 22.3% of its revenue target and 25.2% of its profit target. This pace is consistent with Vietnam's beer consumption cycle, where Q4 is typically the peak quarter thanks to Tet and the year-end holiday season.

Worth noting is that the full-year plan assumes both segments maintain their current form. If deposit rates continue declining in subsequent quarters, the VND 260 billion quarterly contribution from deposits will be the first to compress. The core beer business is more structurally resilient, but hitting the overall annual target will depend increasingly on sustaining gross margins at or near the 37% level.

The 30% Dividend: Cash Already Sitting in the Safe

Following a 20% interim dividend in February 2026, Sabeco approved the remaining 30% cash dividend for fiscal year 2025 at VND 3,000 per share, with a record date of July 28 and a payment date of August 28, 2026.CafeF Total payout is approximately VND 3,800 billion across more than 1.28 billion shares outstanding.

This dividend does not depend on Q2 or Q3 results. With nearly VND 19,449 billion in liquid assets, Sabeco can fund the entire VND 3,800 billion distribution without borrowing or selling any assets. That said, after the August 28 payment, the company's deposit balance will fall by roughly 24%, and the quarterly financial income contribution will compress proportionally.

Valuation and Market Context

SAB closed the May 8, 2026 session at VND 46,250 per share, with a market capitalization of approximately VND 59,300 billion. At this price, trailing four-quarter P/E is approximately 13x. That is not expensive for a market-leading consumer franchise, but it is not cheap measured against the company's own 8% growth guidance.

The full-year 2025 cash dividend yield at current prices is approximately 10.8%, above the 12-month deposit rate offered by major Vietnamese banks to retail customers. This yield differential is one reason SAB maintains a stable institutional shareholder base, even though the stock is not a high-volatility trading name.

Three Things to Watch in Coming Quarters

Looking ahead to Q2 and beyond, three questions will shape the investment thesis.

First, can the 37.2% gross margin hold once input costs stabilize? This is the most durable component of Sabeco's earnings story and the foundation for assessing real operating leverage going forward.

Second, how will the deposit balance evolve after August 28 and as corporate deposit rates continue trending lower? The non-beer financial contribution is the most vulnerable to compression in a declining rate environment.

Third, what will Sabeco do with remaining free cash flow after dividends: continue holding cash, invest in capacity expansion, or sustain elevated distributions? That capital allocation decision will directly influence how the market values Sabeco's "cash vault" premium over the next few years.

The core beer business is recovering visibly through the gross margin data. The deposit income is providing meaningful support alongside it. These are two distinct stories that operate independently, and they deserve to be read separately before drawing conclusions from the headline profit figure.