The numbers tell the story. On May 7, 2026, STB closed at the daily upper limit of VND 73,700 per share, up 6.97% in a single session on over 18.8 million matched units. Sacombank's market capitalization surpassed VND 138,900 billion, the highest level since the stock was listed, with nearly 1.3 million shares queued on the buy side at the ceiling price and no sellers in sight.DNSE

That same week, Sacombank reported Q1/2026 pre-tax profit of VND 2,106 billion, down 43% year-on-year, the weakest result among large-cap banks in the quarter. These two data points are not actually contradictory. They only appear to be when read in isolation, stripped of the decade-long journey that connects them.

Where It All Began: The SouthernBank Shadow

To understand May 7, you have to go back to late 2015. Sacombank completed its merger with SouthernBank, a bank controlled by a group of shareholders associated with Mr. Tram Be, who at that point held the title of former Vice Chairman of the Board of Directors at Sacombank. The transaction absorbed a debt load whose full depth would take years to uncover.

By 2016, the on-balance-sheet NPL ratio had surged to 6.9% of total outstanding loans, and the volume of bad debt sold to VAMC exceeded VND 23,000 billion.VietnamBiz Full-year profit collapsed to VND 89 billion, roughly 90% below pre-merger levels. The bank entered what analysts described as a "three no" state: no dividends, no bonuses, no growth.

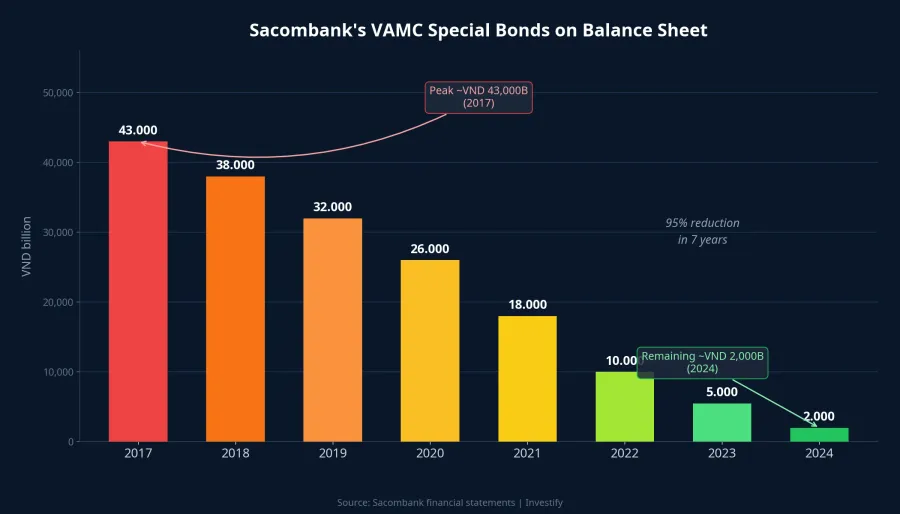

In June 2017, the State Bank of Vietnam approved the formal Restructuring Plan. Mr. Duong Cong Minh took the helm as Chairman of the Board of Directors of Sacombank with a very public pledge: if the restructuring was not complete within five years, he would step down. By end-2017, the VAMC special bond balance on the balance sheet peaked at over VND 43,000 billion.VietnamBiz The associated special provisions would chip away at annual profit every year thereafter.

Seven Years of Incremental Progress (2017–2024)

Between 2017 and 2024, Sacombank recovered VND 25,612 billion from legacy clients: VND 23,363 billion in principal and VND 2,249 billion in interest and fees. VAMC special bonds fell from a peak of over VND 43,000 billion in 2017 to approximately VND 2,000 billion by end-2024, according to analyst estimates, a reduction of roughly 95% over seven years.

The operating picture improved in parallel. Net interest income grew nearly five-fold, from above VND 5,000 billion in 2017 to VND 24,532 billion in 2024. On-balance-sheet NPL ratio declined to 2.4%. Total assets reached VND 748,000 billion at end-2024, nearly double the figure from seven years prior. By end-2024, the bank had achieved 13 of the 14 targets set in the Restructuring Plan. The one remaining target was not within management's own power to resolve.

The Final Knot: 32.5% of Shares Stuck at VAMC

Sacombank has 32.5% of its charter capital sitting under VAMC ownership, tracing back to Mr. Tram Be's former shareholder group. The shares have been frozen for years due to legal complications. Sacombank submitted a proposal to the SBV requesting authorization to organize an auction and recover the debt independently, but the approval process has stretched over multiple years.

SSI Research expects the SBV to approve the proposal in the second half of 2026, with an assumed recovery of approximately VND 12,000 billion.VietnamBiz An earlier report from the Vietnam Banks Association estimated that Sacombank could recover up to approximately VND 19,000 billion depending on the auction structure.VNBA

What makes this step meaningful goes beyond the one-time cash recovery. Once the 32.5% stake is resolved, the special provisions tied to legacy SouthernBank assets will stop eroding annual profit. Simultaneously, the massive block of shares currently parked at VAMC will transfer to new owners, removing the dilution risk that has hung over the balance sheet for years. This is the structure of a dual-impact event: improving reported earnings and cleaning up the ownership structure at the same time.

Why Q1 Looked Weak, and Why the Market Did Not Care

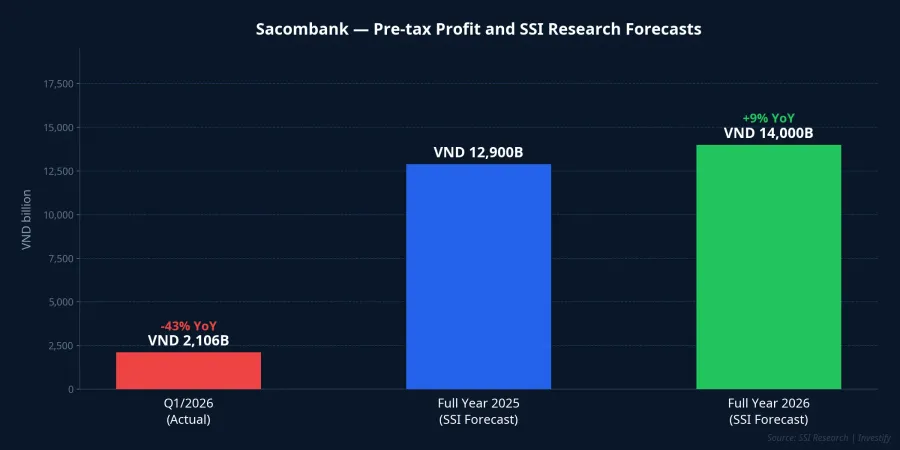

Q1/2026 pre-tax profit came in at VND 2,106 billion, down 43% year-on-year. The primary driver was a sharp rise in provisioning costs, partly because the bank proactively accelerated legacy debt resolution ahead of closing out the Plan. On-balance-sheet NPLs stood at VND 41,498 billion, representing a 6.62% ratio, among the highest in the system.DNSE

SSI Research takes a different view of the same data. Their full-year 2026 forecast calls for pre-tax profit of VND 14,000 billion, up 9% from 2025, even with annual provisioning costs projected to reach VND 6,100 billion, up 47.6% from the prior year.VietnamBiz Under this framework, the elevated provisioning in 2026 is the final investment to clean up the balance sheet before closing the Plan, with core operating income improving enough to offset that pressure.

The market is clearly not pricing Q1/2026 numbers on paper. The May 7 session was a bet on the second half of 2026: a bet that the SBV will approve the proposal, and that the bank will close out the Plan exactly 10 years after Mr. Duong Cong Minh took over with a five-year pledge that ran four years past schedule. If both things happen, the cash recovered from the auction combined with the gradual reduction in special provisions from 2027 onward would deliver a double tailwind to underlying earnings, the portion that high provisioning costs have been masking for several quarters.

Risks on the Table

The thesis plays out only if two variables hold. First, the SBV actually approves the proposal within SSI's assumed timeframe. The approval process has already spanned multiple years; one additional quarter of delay would be enough to disappoint a market that has already moved significantly ahead of actual progress. Second, the auction achieves a result near the VND 12,000 to 19,000 billion range, a figure that depends on market conditions at the time of the actual sale.

Independent of these two, the 6.62% on-balance-sheet NPL ratio is a risk that belongs to current credit quality, not legacy restructuring. It has nothing to do with the Tram Be group or the SouthernBank inheritance. Even if the Restructuring Plan is fully closed out, this is an issue the bank will need to address on its own terms in the years ahead.

What May 7 Was Actually Measuring

The most notable thing about the May 7 session is not the price itself, but the logic behind it. The market did not pay VND 73,700 for the weakest Q1 earnings report among large caps. It paid that price for a scenario: Sacombank closes the Plan, frees its balance sheet from the last legacy burden, and enters 2027 with underlying earnings no longer obscured by special provisions from a merger completed a decade ago.

Whether that scenario materializes will become clear within a few quarters, when the SBV either issues an approval or pushes the timeline back again. Two signals worth monitoring closely: the pace of regulatory progress on the 32.5% share disposal, and how NPL trends move through the remaining quarterly results of 2026.